Forum Replies Created

-

AuthorPosts

-

TrentRothall

ParticipantYeh similar to what you posted. That’s why i’m a bit wary, if you constantly getin the bottom 30% of the range it’s going to be a fair bit worse than backtest i would think

ParticipantFollowing from Julian and Seths post in Terry’s jornal.

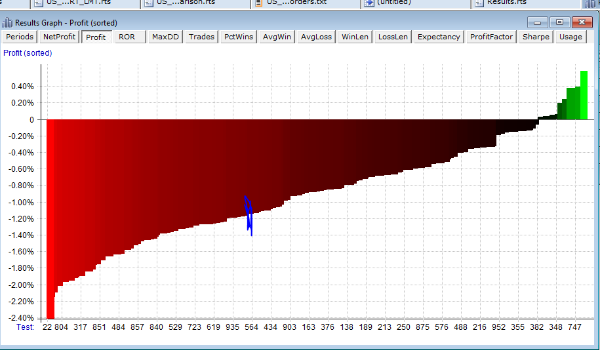

I have been trading a long/short MOC system for about a month now. I have coded in RT and I am running five positions long and five position short at 10% each. Each day I am placing 15 long and short positions with the API. (Running two Apis, one long one short). Because I am running a cash account and not leveraging I found it not worth while only placing the number of orders for my maximum positions as with the AB CBT code. The exposure was too low so returns weren’t great.Placing more orders than positions does introduce a element of selection bias but as Julian said in RT is easy to rank these orders. Because RT is so fast at back testing you can easily do 1000 MCS simulations to test the possible variance to get an idea of the possible results.

I’ve been keeping a spreadsheet of my daily returns versus the back test on days where there are > 5 entries from my 15 orders. I want to know if on average my returns are going to be worse than the back test when SB is occouring. Because I’m still sceptical if I can achieve the returns that the back test shows. So far it seems on days when there more possible entries than positions you will get the worse end of the distribution of returns.

Example. Last session 4/12

Live:

7 trades total – 2 long 5 short

Return: -1.15%BackTest:

7 trades – 2 long 5 shortTotal possible trades from 15 long order + 15 short orders

15 trades – 2 long 13 shortI do 1000 backtests over 1 bar to see all the possible outcomes from taking different trades.

MAX RETURN: +0.59%

AVG RETURN: -0.85%

MIN RETURN: -2.41%MY RETURN: -1.15%

Remember this is only over one bar, so the distribution of returns can be quite large. The blue line on the picture below is where my returns came in the day. This is 1000 runs over the last bar. I guess the theory is over the long term you will get a random outcome and it will average out. Whether or not this happens in live trading I guess time will tell and is why I am keeping the spreadsheet.

If it turns out that in live trading you get a worse end of the deal. Then you can easily incorporate that into the back tests in real test. To get a better/more accurate back test.

ParticipantSo with a cash account you can do this Glen? I thought i couldn’t i better check again! Thanks

ParticipantAnother thing with stocks under $20 in the US they are probably more likely to go up 1-200% in a day! Probably similar to a 3c mining company in Aus.

I’ve got some serious brain block trying to come up with a decent US MR system. Hopefully i can snap out of it soon!

Looking good mate!

ParticipantOuch!

Do you know why you missed them? Just no fill or not available?

Maybe change price filter to C > $20 ?

ParticipantNice one Seth! Not a bad month!

Good luck with the application!

ParticipantGetting a big month close to system release like that will really help with compounding that account too hey! Nice.

Participant#keeppushingbuttons

Nice one!

ParticipantBoom, nice Glen. You have been smashing it too! How’s the win % on MR1!! Nice

ParticipantNovember Results

ASX WTT = 17.47%

ASX MR = 0.5%

US long/Short MOC = 4.7%Acc = 6.33%

Small caps really took off this month after a rough start in October. Back in the green (for now). Some positions are looking extended but i said that basically every day for two weeks.

ASX MR i did some more testing and lowered number of positions to 5 @ 20%. i basically will be starting this month with a equal split between my 3 accounts. so even though position size has increased in % terms in $ terms it’s fine i think. although once recommencing i had a partial fill in the first 5 trades… Hopefully will phase it out once i can work out a decent US MR. I have been toying with a aggressive NDX rotation too in place of this. Nick has been talking about his long term bullish bias over next 10 years so that maybe wise.. thoughts? My system i coded in 2017 has been going nicely and fared quite well over Rona so i basically have one ready to go on the NDX

That would give me

Small cap ASX trend following

R1000 MOC

US NDX rotation.ParticipantI’ve been hitting the refresh button waiting for this update, thought it would be big but HELL! Great work Tim!

ParticipantYeh i’ve seen that.

There’s a bit more involved to only take the first signal, think i’m getting there though

ParticipantI traded it last night (19th) with no issues besides a small loss =]

ParticipantHow do you guys post your STT performance over x period?

ParticipantHow do you filter trades by dates on the STT dashboard? In older versions i thought there was a date range selection?

-

AuthorPosts