Forum Replies Created

-

AuthorPosts

-

TrentRothall

ParticipantTrades for today were 1 exit , no new entries

1 Exit tomorrow – IPH had a nice bounce today to trigger an exit

2 open positions

3 Pending orders for tomorrowNot the ideal setup at the moment – currently waiting for IB to approve my margin account, so trading the system in my sim IB cash account. It doesn’t have API capability so if i get my full portfolio i will have to manually close trades. But it should still allow me to make sure the trades are executing properly and the explorer is not losing trades.

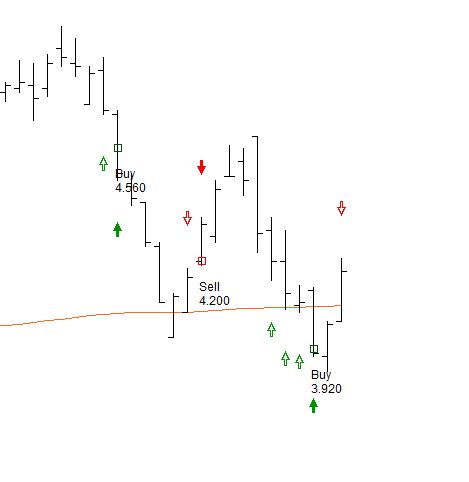

ParticipantHere are a couple of trades in MTR over the last few weeks – one exit tomorrow

Participant

ParticipantAll week has been spent running stress tests and MCS on my Mean Reversion system and i am happy with how things have turned out. It is amazing how adding a few small tweaks and adding you own ideas to a simple concept can turn an ordinary system into something that looks good and SHOULD be easier to trade.

A bonus of the system I think is that it doesn’t need to use an index filter to keep the drawdowns low in fact adding an index filter drastically hurts both the CAR and MDD. Another positive from the test results is that the past few years the system has had good returns, I think it helps me mentally knowing that the system does not rely strong bull market to make decent returns, it also has a fairly high when rate around the 68% mark so hopefully this should help the consistency.

Now that I’m happy with the system and that all the test results seem to be good I will start to paper trade the system in my Sim account. I’ll post a bit more regularly now and let you know how it’s going.

ParticipantOk thanks, cleared that up

ParticipantSince last week i have done a bit of a swift U-turn i have gone from a weekly system to a MR system, while the results from my weekly system were not bad Nick pointed out that it might be hard to trade at times with the consistency of returns. This got me thinking about what I actually set out to achieve and originally I was after a short term system with a more consistent profit potential.

I trawled through different Internet forums and blogs around the place to get some ideas, then I added a few things that I had seen and liked out of other mean reversion systems. i ended up with system that at the moment is looking pretty good, I didn’t want something that has a overly high trade frequency because I want to run it on the ASX and didn’t want commissions dragging me back to much.

Started doing some stress tests and Monte Carlo simulations, so I will let you know how I go.

ParticipantI personally haven’t done very much trading over earning releases but just some observations that I have picked up is that once a stock has upward momentum quite often if there are gaps over earnings they tend to go the way the stock is moving.

I would think to do if you are trading a small universe such as the NASDAQ 100 a lot of the stocks might be reporting in the same month so you might have to end up taking signals that aren’t as strong, and then earnings might not go your way.

I’m not sure if I can help you in the way of testing that though. Also this would not be the first time observations are incorrect… :ohmy:

ParticipantOk nice, that should work well

ParticipantHi Oliver, just wondering if you are working on a ASX or US system?

ParticipantThe last week has been spent basically running MCS and various stress tests on my system. Have been sending the code through to Craig and Nick a few times to ensure everything is on track and no mistakes hidden in there.

I think i need to make some sort of checklist to work through while testing systems, i seem to sway off track and certain tasks take longer than they should…Haven’t been doing much trading of late everything is a bit volatile at the moment.

ParticipantHi Oliver

have a look at Module 17/27, Lesson 1/5 it mentions about using the ROC for Positionscore.

Try –

PositionScore = 1000+ROC();

or something similar might help. If you want the ROC on the setup bar you will need to use ref(ROC(),-1) I made that mistake earlier

Trent

ParticipantQuote:Next thing is to go over the signals in the Explorer window to ensure that my back tests are picking up the signal ranking properly. Then I’ll stress test the parameters to work out if the system is robust enough.found an error in my backtest ranking code i was using PositionScore = 1000+RankROC; but it was using the ROC on the entry bar and not the setup bar. Changed it to PositionScore = 1000+Ref(RankROC,-1);

it diluted results again but haven’t done a MCS as yet to find out more info… It pays to check!

Participantearly on in the week I finished coding my momentum system which uses the ROC indicator as part of the entry. The results from this entry technique seemed to be the best that I have been testing so far.

After going through a lot of the charts and checking the code over, and observation that I picked up was that a lot of the daily chop was causing an exit in the position before it had a chance to move upward. I played around with the stoploss using different parameters, also coded up and ATR stop neither of which really helped with the results in fact all they did was increase the drawdown.

I then tested the system on a weekly timeframe to try and alleviate some of the exits caused by the daily chop, trends on a weekly timeframe seem to be smoother.

When first testing on the weekly timeframe I didn’t put enough thought into adjusting the volume and turnover filters and I thought that I had found the ultimate system although I was suspicious. After a quick post to the Forum I soon realised that I didn’t have the filter set right. Once I started testing system properly the results are still showing it is a good start.

Had a Skype call with Nick this morning to go over my backtest settings to make sure that my results were correct.

Next thing is to go over the signals in the Explorer window to ensure that my back tests are picking up the signal ranking properly. Then I’ll stress test the parameters to work out if the system is robust enough.

ParticipantNick Radge wrote:I came across another site that uses single market systems – I’ll try and find it for you. That guy made the argument that there is nothing wrong with data mining patterns. As I say in my notes, it’s my personal opinion rather than a law that must be followed. The one thing I would suggest, which is also what Howard Bandy suggests, is using a system stop loss of some type, like an equity curve trail stop or some such.Is the stop loss in case the system gets totally out of sync with that market? So you would stop trading it for example

ParticipantThanks Said – tested it and it doesn’t improve results. i guess the entry conditions are there because they produce profitable trades – miss the proper signals and you can miss out on profitable trades.

ParticipantI tried

BStrade = Ref(PriceAtBuy==0,-5);

Doesn’t logic say that should work? to enter a trade PriceAtBuy has to be false 5 bars ago so there is no trade on. That didn’t work either, it still entered a trade straight after an exit

-

AuthorPosts