Forum Replies Created

-

AuthorPosts

-

TrentRothall

ParticipantThink i found my answer to above.

Just need to use Isempty() function.

ie sectormom > x or Isempty(sectormom);

May 21, 2020 at 7:18 am in reply to: Incorporating an Index Volatility Based Trailing Stop with the WTT #111485ParticipantDo you mind posting your looping code ben, the issue might be there. It looks to me that the backtester didn’t know you were already ‘in that position’ if that makes sense.

May 21, 2020 at 5:12 am in reply to: Incorporating an Index Volatility Based Trailing Stop with the WTT #111482ParticipantCheers Glen, that makes sense

May 21, 2020 at 2:42 am in reply to: Incorporating an Index Volatility Based Trailing Stop with the WTT #111480ParticipantAnother question for you Glen, have you had any trouble with low-volume stocks? I see that your turnover filters are set to $500,000. Which over a week is only $100,000 a day have you had any trouble with fills or slippage?

May 21, 2020 at 2:27 am in reply to: Incorporating an Index Volatility Based Trailing Stop with the WTT #111470ParticipantFor guys trading weekly/daily trend systems do you have a entry condition that open must be within x% of the signal bar close to get a fill? I imagine on the ASX guys are placing a LMT entry 3-5% higher than last close to get the opening price. So if price has a big gap you might not get filled.

ParticipantAfter seeing your post on Wayne’s thread

Have you had any experience with A.I. or it probably can be without it tbh (i’m no expert). Would be great to be able to go over a backtest or potential setups and see what precedes the good or bad trades, bar, volume patterns etc. I guess i kind of looked a bit deeper into my system with the cbt to compare setups but there must be a better way.

ParticipantYeah ok, thanks Nick. I’ll keep that in mind. Cheers

ParticipantI’ve been trying to test using the sector ranking as both position score and a entry condition. eg sectormom > x

The first issue i hit was not showing and trades pre 2019 in a backtest. This was because the sector $XRE.au seems to be added in late 2017. There is a work around here: https://norgatedata.com/amibroker-faq.php#limitedresults

But now if a stock is in the sector $XRE.au currently, it doesn’t show a buy until 2019 even if it meets the previous criteria.

I’ve tried to add:

Code:sectorUp = sectormom > x or sectormom == null;Anyone ave any ideas? or is that makes no sense ill try and explain it again.

ParticipantNot sure if i liked after life or was semi depressing lol

ParticipantNice Scott, that’s a good idea. my systems been lazy as well i think 2 or three trades this month.

ParticipantHoly shit!

ParticipantCheers seth looks good.

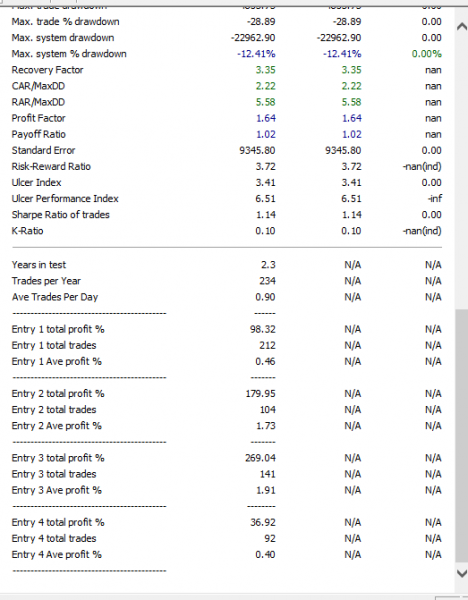

I spent the arvo adding custom metrics to my backtest report, it will be good for reviewing my entries instead of manually doing it in excel

Participant

ParticipantInteresting docco

ParticipantHi Seth,

Do you get stopped out a lot on btc? there’s some wild volatility there! Are you trading it via cfds or another way?

Sounds confusing haha.On my MR system it isn’t a MOC just regular MR. I was trading on the All ords but now on the entire ASX will be monitoring slippage though.

ParticipantNo worries Howard. Hopefully you find it useful.

-

AuthorPosts