Forum Replies Created

-

AuthorPosts

-

TrentRothall

ParticipantSeth Lingafeldt wrote:Glen Peake wrote:Trent Rothall wrote:It would be interesting to know the % of daily volume that occurs in the opening/closing auctionsSee attached for the past month of 1minute intra-day data.

")

I have no interest in this, but Glen is such a swell guy. Good guy Glen!

spot on here!!

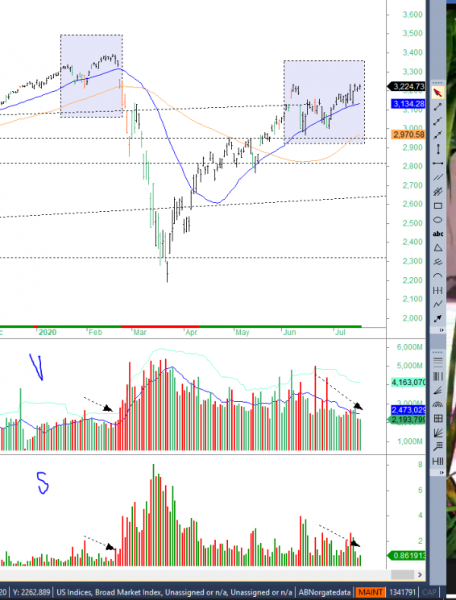

Participantexactly, the 3 bar turnover is over $3.8m too so there is no way that you wouldn’t include something like that in your backtests. It would be interesting to know the % of daily volume that occurs in the opening/closing auctions

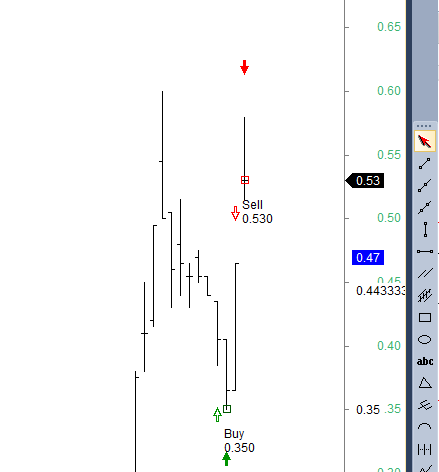

Participantonly about 10k shares traded at 0.35

ParticipantThis is the kind of heart break that come with short term trading the ASX.

Missed trade in AR9.au 51.23%. Killer

Participant

Participant😆 😆 😆

I’m all ears Seth

ParticipantGood recap! What sort of discretionary trading are you looking at Matthew?

ParticipantYes, short term memory – i’ve been reminding myself of the good times. Probably a bit the same as Mike with the emotion scarring from my first proper DD, plus it came at the worst possible time for myself but keep on pushing that buy button… Few good months and i’ll be back.

ParticipantASX MR = – 0.43%

Some serious fomo going on with everyone else killing it atm. Well done all!

ParticipantThat’s nice Glen, cheers.

ParticipantOr better ways of doing this

ParticipantDoes any one do any statistical analysis of basic chart patterns or bar patterns using a exploration to test the validity of a certain setup?

I want to look more into patterns of price/vol to find tradeable setups.

If anyone does this, any tips or metrics you like to look at?

I’m thinking something like the basic exploration below (with added metrics) to help find good setups

Code://Test to find patterns – basic consec inside days for exampleconsecInside = Inside() AND Ref(Inside(), -1);

MA1 = MA(C, Param(“Long MA”,50,20,300));

TrendUp = C > MA1;

cond1 = consecInside AND TrendUp;

Filter = cond1;

AddColumn(C, “Close”);

AddColumn(Ref(C,5),”Close in 5 bars”); // find the C after 5 bars

AddColumn(Ref(ROC(C,5),5),”Roc in 5 bars”); // find 5p ROC IN 5 barsParticipantYou always miss the good ones too ffs

SLC.au

Participant

Participantoh you might be right actually, it might be worth sticking to the mkt orders and reviewing the fills like you said

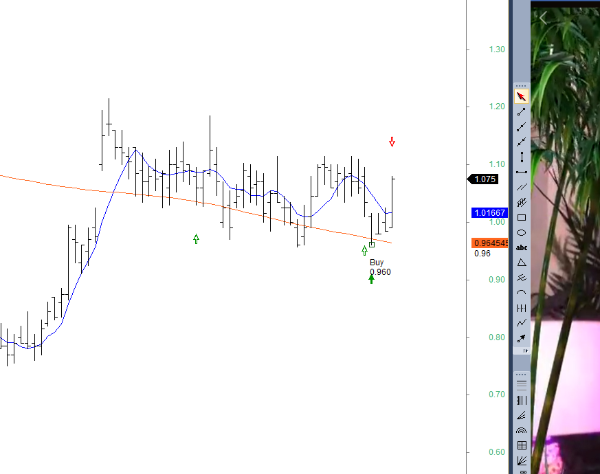

ParticipantIs it just me or the price action looking similar to pre crash? diminishing volume, smaller price spread while price is creeping higher.

Although think i’ve said this twice now…

Participant

ParticipantHi guys

I’ve been trading my MR on the ASX for ages the biggest issue i face is not getting fills on the low. As Glen or Scott said above i think this not only happens in thinly traded stocks but stocks that also have a reasonable daily turnover.

I also don’t run the CBT code on my mean version system because I want to send as many orders as possible to the exchange to try and get my exposure up. Because of the smaller universe I think running the CBT code you would have quite low exposure because of the minimal orders placed. (I could be wrong about that).

Matthew, you might need to send limit orders I think to get filled in the closing auction as you do with the opening auction. By sending a market order you might just be getting the market price at that time, which would probably be close to the closing price I guess but it might not be exact.

-

AuthorPosts