Forum Replies Created

-

AuthorPosts

-

smurfki0808

ParticipantAnother month, more chop. This month, I had to do some digging as confidence took some hits.

The relentless chop on my WTT has taken a toll. The last few months has seen the most consecutive losing trades in my entire backtest period: vis. 22 in a row! But, in live trade, I’ve had 16 losing in a row, followed by a single small win, and then the next 6 losing trades…certainly trying times. The downward reversals in the markets seem to be quite in sync with my WTT recently taking up new positions, haha.

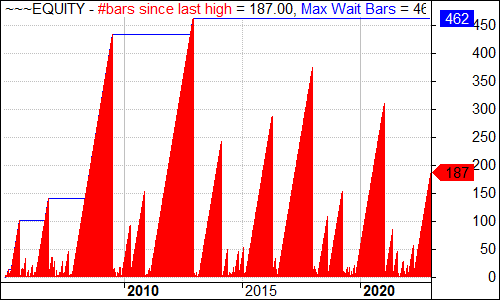

My ASX MR system successfully picked 4 positions that went into trading halts, and suspensions for capital raise, and upon resumption got smashed. Not much I can do about those, but it did prompt some further research. To preserve mental capital, I investigated the effects of both a regime filter and a stale exit on the performance of the system. Yes, overall potential reduced, but the bottom line was a stark increase in the CAGR/MaxDD ratio and the Recovery Factor. So, for peace of mind and willingness to continue, I’ve decided to implement these modifications.

So now, all my systems are well into portfolio protect, with most of the cash on the sidelines, doing as they should.

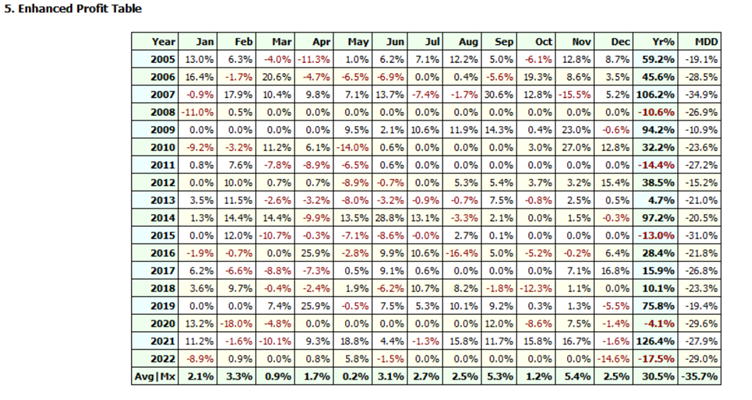

ASX WTT: -4.43%

ASX MOMO: 0.0%

ASX EMO: -5.08%

ASX MR#1: -13.35%

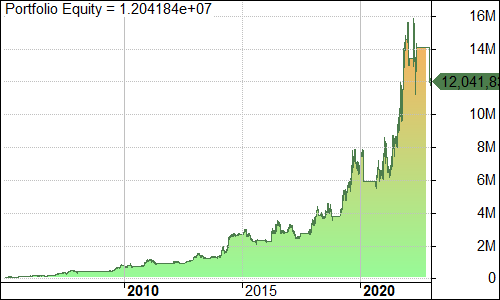

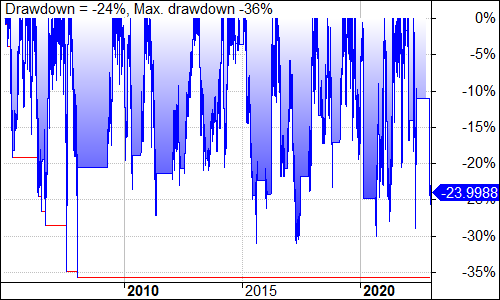

Managed Growth Fund: -0.4%Total for month -1.7% taking total drawdown to -25.8% and to a new max.

ParticipantAt what point does being stubborn transfer from being a strength to a threat? In future, I hope to look back on these times, and reflect fondly on the value of sticking with the process.

I continue to become more comfortable trading my ASX MR#1 strategy, even though several trades were whacked after being caught in suspensions. My processes for running the strategy are smoothing out, and the more trades I execute (50 completed now), the more value I can see in having this type of strategy in my stable. After all, the strategy nearly made a profit for the month!

Otherwise, I’ve continued building and testing a range of strategies to complement my existing ones to develop different equity pathways (XAO Monthly/Weekly rotation, XTO Monthly rotation, ASX weekly volatility breakout, ASX MR#2 RSI). As yet, I’ve not deployed any of these new strategies, but given market dynamics, I’m hesitant…. Is there ever a better or worse time to deploy?

I’ve followed the All Weather Portfolio discussions, and tinkered with concepts to understand the rationale and think about how such an approach might fit in my portfolio longer term, replacing my Managed Growth Fund.

ASX WTT: -1.7%

ASX MOMO: -9.2%

ASX EMO: -10.5%

ASX MR#1: -0.6%

Managed Growth Fund: -0.8%Total for month -3.5% taking total drawdown to -24.9% and to a new max DD, exceeding -24.1% at Dec 2022.

ParticipantMarsten Parker having a chat with Michael Covel. Good to hear his thoughts on systematic trading.

ParticipantNick Radge post=14288 userid=549 wrote:The other pertinent comment that stood out to me was the time between fat tails that he’s chasing can be extended.

Hence, the need to stay in business until the fat tails come along.

Participant“This business is a marathon, not a sprint”,…

“Patiently waiting for the major trends to emerge”,…

“Trust your research”,…

“Big draw downs would come, …but I stuck with it, as they were within the bounds of my research”,…Always good to hear.

ParticipantGlen Peake post=14259 userid=314 wrote:What do others do? I’ll let you know if/when $AVZ.au comes out of its suspension…… lolCan’t really avoid it….. you can minimise the damage by diversification of multi systems….which you’re doing, so the percentage ‘hit’ isn’t going to wipe you out etc…. and the loss only represents a small % of total account etc….

Unlucky mate…..

Yes, I too have AVZ.au taking capital out of the game. Maybe there should be a rule for ‘region of operations’ saying stay clear of African complexities, haha.

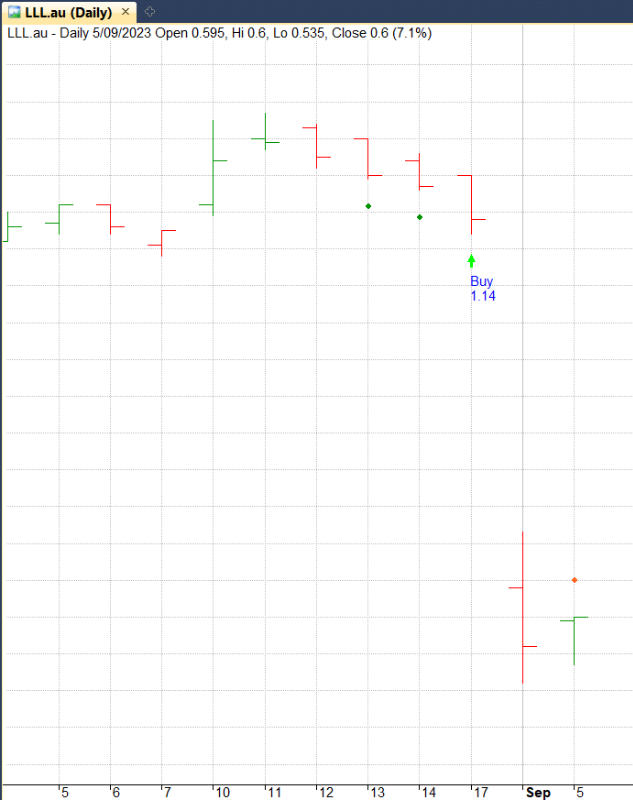

Yes, I hear your wisdom, it is what it is in volatile times. Out of LLL.au now, and waiting for the big bounce by end of week to exit the same in WTT.

Thanks Glen,

ParticipantTrading halts on the ASX when in short term mean reversion positions, are getting a little tiring. Now LLL.au, I entered MR trade on the day that they went into Halt and then Suspension. Upon resumption, whacked.

Is this another little lesson for me why same day MOC systems might be preferred? What do other people use as a tactic in this situation? Do you sell on the resumption and simply get out? Thanks.

ParticipantQuote:“…do you allow the same stocks to be traded over the different systems at the same time or do you exclude duplicates?”No. One symbol only across all systems – the beauty of RealTest

ParticipantQuote:“…do you allow the same stocks to be traded over the different systems at the same time or do you exclude duplicates?”No. One symbol only across all systems – the beauty of RealTestOne symbol only across all systems to offer greatest opportunity to find that next outlier? Is that the intent?

Thanks for your insights Terry and Nick.

ParticipantGlen Peake post=14232 userid=314 wrote:Thanks for the update Sean…. A nice catch with $EML.au….. Well Done!FWIW: I was also in $MSB.au prior to the news catalyst and the dump thereafter…. Swings and roundabouts I guess.

Well, that is reassuring to me Glen, glad to be sharing the swings, see you on the round about! Sharing the rides is a bonus of the forum, thank you.

ParticipantSeems like August 2023 was a challenging month for lots with their various strategies, me included. I can be thankful that our managed Growth Fund held its head up above water.

My ASX MR#1 system was progressing quite well, until signal luck hit with a big stick. A position in $MSB.au, was hit by a trading halt, followed by reporting and got summarily whacked, delivering the 2nd largest losing position in backtesting since 2005, for a 67% loss. Three good lessons came from this. Firstly, upon closer scrutiny of the backtests, I saw that it happened before and when the largest loser occurred, I could see that the portfolio recovered quite quickly, after about 8 trades, so that was encouraging. Secondly, I revisited the role of stale exits, rather than waiting for an upbar exit. Had I been using a stale 3-bar exit at this time, $MSB.au would have been in and out with a small profit instead of a whopping loss. While stale exits take a little bit off the performance, I can see they add to the psychological comfort. If there is no bounce after 3 days, then let it go and find the next one. And thirdly, I finally got one to bounce my way with a good trade on $EML.au, which I picked up on low of the day prior to reporting. After report it jumped, resulting in a 36% profit. So signal luck can go our way too, carry on.

The upside of my ASX WTT is that I can see positions starting to accumulate some useful profits, e.g. $DUR.au, $MRM.au, and $C79.au. These positions have managed to survive the chop and stay in the trade. No $AVS.au unfortunately, but that’s signal luck for you.

ASX EMO is doing its job of plodding along and picking up some useful returns from the likes of $BGL.au and $BOT.au.

ASX MOMO was having a great month, until reporting…

ASX WTT: -4.8%

ASX MOMO: -4.2%

ASX EMO: -3.2%

ASX MR#1: -7.5%

Managed Growth Fund: 0.6%Total for month -1.1% taking total drawdown back down to -22.9% and back to where I was in May and June of 2023 and October 2022. Sideways

ParticipantSignal luck,….AZS signalled in my WTT strategy back in May at $0.505, but I already a had a full allocation of positions at that time,…while WC8 signalled this week…ho hum.

ParticipantGlen Peake post=14208 userid=314 wrote:Hi Sean,This should rotate Fortnightly on a Monday and cater for Public Holidays on a Monday i.e. Rotate on the Tuesday

FYR:

Discussed in this series of posts: https://edu.thechartist.com.au/forum/progress-journal/12-nick-radge-daily-journal.html?start=288#9152////////////////////////////////////////////////////////////////////////////////////////////////////////////

Mon = FirstDayofWeek = DayOfWeek()

// rotate only on Monday, every 2nd one

EOM = Mon AND (countMon % 2 == 0 );score = Ref(Rank,-1);//score is the rotational criteria

Score = IIf(LE,score,0);

PositionScore = IIf(Year()>=1985 AND EOM,Score,scoreNoRotate);////////////////////////////////////////////////////////////////////////////////////////////////////////////

Thanks Glen, I see that there is nothing new under sun, you guys raked over these coals a few years back. It is interesting that the fortnightly rotation fares worse than the weekly rotation. Hence, the benefit of the weekly and monthly rotations running in tandem. Glad I could test these three differing rotations to quell the gnawing. Cheers

ParticipantNick Radge post=14207 userid=549 wrote:Weekly will be:DofW = dayofweek() < Ref(dayofweek(),-1);

LE = Ref(BuyTrigger,-1) AND NOT OnLastTwoBarsOfDelistedSecurity;Score = Ref(ROCFinal,-1);

Score = IIf(LE,score,0);

PositionScore = IIf(Year()>=1960 AND DofW,score,scoreNoRotate);

So Nick, your US TLT strategy operates on two rotations right, weekly and monthly. The analogy for me would be running half my capital as a weekly rotation as per your suggested code here, together with half my capital in a monthly rotation. The hypothesis being, when a position takes a nose dive, it will likely be replaced in the weekly version, but held in the monthly till end of month. And, if a new front runner turns up in the weekly rotation, it might push its way in on that time frame. As your notes say, it should be unlikely that a 10 different symbols would be held at any one time. Another reason to get into RT!

ParticipantA little project that has gnawed away at the back of my mind was to develop a monthly rotation strategy for the broader XAO minus the XTO section of the ASX. There are often some strong movers in there (up and down), so maybe it was worth my while.

Compared with my Monthly Rotation for the XTO, I quickly realised this section of the market is a little more challenging. The increased volatility appears to manifest in longer MaxWait times, and deeper MaxDD. I guess when the market decides “risk off”, this section gets hammered quicker than the XTO. To trade this part of the market, it looks like I would need to be comfortable with extended periods of drawdown, that turns around with a stampede. Hmmmm.

One potential solution may be to rotate twice a month, rather than once per month? Can anyone point me to AFL code that rotates every 10 days, rather than end of month, or end of week? Or any other tips for this style of strategy would be greatly appreciated.

Participant

ParticipantSolid, nice work Glen!

-

AuthorPosts