Forum Replies Created

-

AuthorPosts

-

ScottMcNab

ParticipantDo you have different IB accounts for US and AUS markets Nick ? I am trying to get my head around the possibility of needing to account for currency conversion. It would seem a lot simpler for position sizing to keep an IB account for the US markets set to US currency and have a different IB account for AUS markets with currency set to aussie…or does Share Trade Tracker handle this ?

ThanksParticipantAre you using Share Trade Tracker to keep track of your paper trading as well as your live trading Trent ? Paper trading multiple systems from the same IB account would necessitate keeping track of the portfolio equity for each of the systems to enable accurate position sizing (based on unrealized P/L and commission costs) as look to open new positions ??

ParticipantI found this site quite useful…actually discussing MRV system of Nick’s but forms a good basis to experiment from

ParticipantI have a few hours spare today so I might try it using different exits for different conditions (rather than scaleout which I suspect is be beyond me)…interesting that it seems to work better for momentum verses MRV. Thanks for replies.

ParticipantI thought I had all Nick’s books but apparently not. Is this contained within the Chartist community Trent ?

ParticipantI’d like to hear how you go Oliver please if you get a chance to try it out….I’d also be interest if anyone has tried playing around with different exits based on changing market conditions too. I have wondered if a filter could be added such that the stop loss was tightened or loosened (eg depending if stock and/or index ADX or RSI rising/falling or the close in relation to HHV(H,20) etc) or the filter may trigger a different exit altogether (eg strongly strending market then exit1 = close>ref(c,-1) AND ref(c,-1)>ref(c,-2) …otherwise exit2 = close>ref(c,-1)….) or may scale out to take some profits earlier than would normally.

I hope to get around to trying this stuff out once have a system that passes paper trading… if happens I will post too.

Cheers

ParticipantYep….it would do that Trent…this system doesn’t allow an exit signal on the same day as entry though…day after entry has to be a higher close to trigger exit. I did try it allowing exit on same bar but results were sig worse…but for a slightly different system it may turn out differently.

ParticipantCongrats Trent…

") Participant

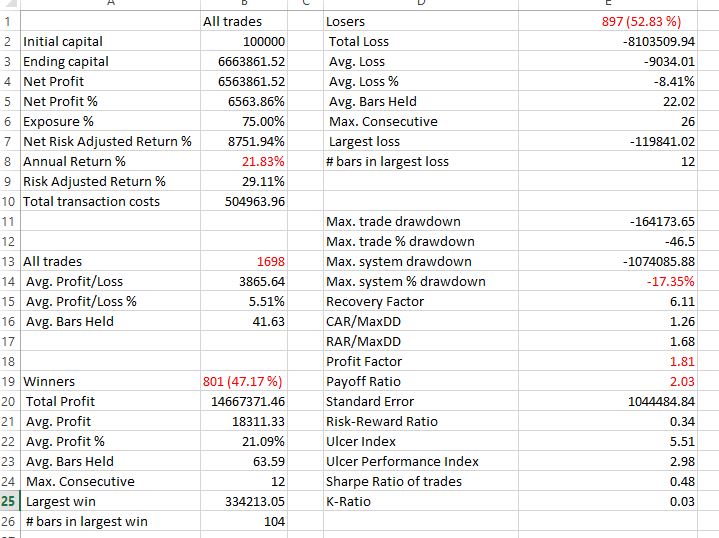

ParticipantFor reasons I am unsure of every system I have is pretty awful on ASX. I have a weekly system with decent stats but when it is compated with short term MRV or breakout systems the results are significantly lower. The only potential I can see for it relates to the low number of trades and possible application in super fund depending on ATO/super laws but thats for the accountants.

Trend following on SP1500 hist 1/1/95 until present:

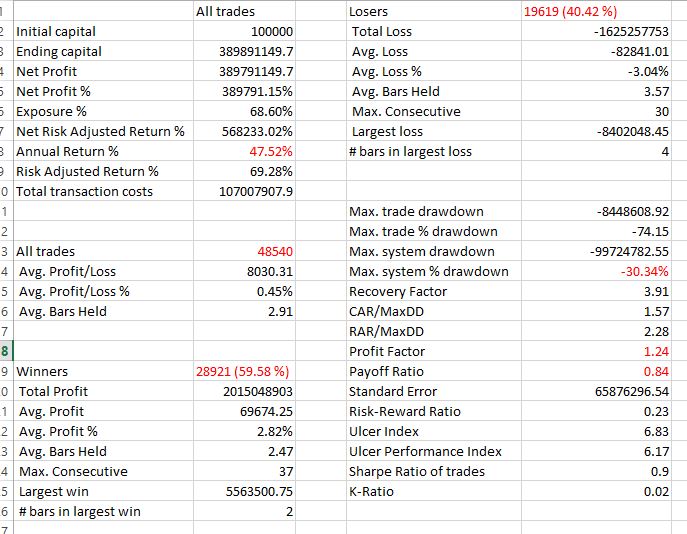

I am also working on a MRV as it seems to produce its drawdowns at different times to the TF and breakout systems…so if both systems have a maxDD of -25% but they happen at different times I should be able to keep maxDD of portfolio under 20. The current MRV system buys on open and suffers a bit as a result but is a work in progress.

MRV on Russell 3000 his 1/1/95 until present:

Thanks for the input Said

ParticipantSystem buys on the open to keep it simple (to try and avoid added complexity to order entry). I am confined by some pretty limited coding skills at the moment…if it wasn’t for Craig’s looping templates I’d be stuffed . So all of my systems do currently buy on open but a MRV system I have been playing with gives better results using the stretch concept associated with buy limit order. Coding is something I will work hard on after the Mentor Course is complete but for the moment I need to keep rolling to get the paper trading and then live trading happening.

At the start of the course I thought a weekly system would be better as I felt it would be more sustainable for me long term (only having to trade over the weekend) but as it turns out it was the only type of system I could get to work (until now)….I found the patterns I was testing were more definite (less noise ?) in the weekly time frame and the size of the move meant commissions had less impact…the downside was the reduced trade frequency.

I did try the two consecutive higher closes too…I am yet to try a profit target with this particular system so that is probably next….thanks again for your input Trent

ParticipantThanks Trent…Said has some great posts…exit in my HFT system is a higher close….this HFT system is actually a breakout system buying strength rather than a MRV system like Said’s so close above the MA wont work well in this particular case as this occurs on entry. I have found, not surprisingly I guess, that the profit factor improves if I move to a weekly system but I’m trying hard to get a daily one. I was looking over Said’s posts again in light of your suggestion and noticed for the first time that his MRV seems to operate with a profit factor not too far removed from 1.3 so I will keep tinkering with this one… thanks again for your suggestion.

ParticipantHuh….miracles do happen

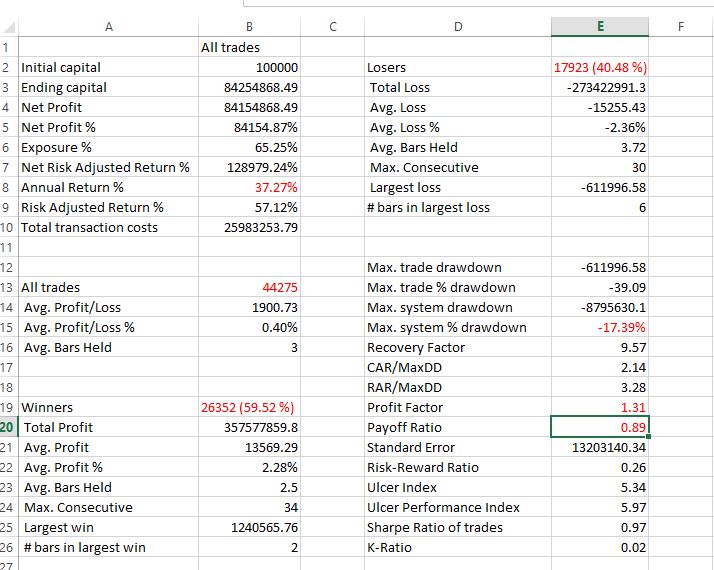

ParticipantBeen working on daily system to work alongside weekly system that am paper trading….have some results (thank you for help again Craig) ….I admit that it sails pretty close to the wind…results are based on commission for IB (0.005 per share)…rapidly becomes non-profitable with higher commissions…is a HFT daily system on Russell 1000 hist database….not tried inserting jpg before so my guess is will be issues…apologies in advance

Participant

ParticipantThanks again Said…I am only paper trading a weekly system…I have a daily system I have been backtesting that seems ok with IB commission structure but it only takes a small amount of slippage and the profits rapidly disappear due to the small profit factor…have you found any issues with this with your extensive testing of your MRV so far or has the paper trading P/L been close to the backtesting ?

CheersParticipantMany thanks for posting Said. Do you use the commission table (with IB settings) for your backtests ?

-

AuthorPosts