Forum Replies Created

-

AuthorPosts

-

ScottMcNab

ParticipantMy system exits on open next day…only holds overnight so every morning the system goes flat and tries to load up all over again

ParticipantNot sure if its a viable idea but I have noticed that on days when my MRV’s have a huge number of entries for a day (over 100 but up to 300 on RUI) using Darryl’s addtocomposite that the index often seems to close higher 5 days later…I have no chance of coding this and testing it properly but posting it in case someone interested enough to try it. I guess the huge spike in MRV entries (eg using Said’s lowest low in 5 days) would correspond to a market pullback but measures it differently from a traditional indicator.

ParticipantIt was my concern regarding selection bias. I was finding that the systems with the best metrics were not taking a significant number of trades.

ParticipantDarryl Vink wrote:Scott McNab wrote:30 positions at 6%made some changes to tighten entry criteria and reduce selection bias

its an interesting exercise trying to find the best combination of margin, position size and max positions. after many tries and fails at consistency i went back to 20 positions with 10 % equity with my system due to consistent results. im still not sure what is best…

I made the decision to use 30 positions based on the code/graph you were kind enough to post. It was a bit of an arbitrary decision but I wanted to limit the number of days where the system couldn’t take all the available trades to 3 or 4 a month. The systems’s metrics are better with a lower number of positions but the message I took away from the last group call was that we each had to decide whether to trade for CAR or comfort…so I went for 30 positions. It may be diluting CAR but so be it. The results I posted were for 2011-2016. I used this as this was the worst period for the system and I wanted to base any changes around this time frame in case this is a reflection of changes to market structure etc (ie changes that are likely to persist into the future) rather than just an anomaly . I too am constantly trying different combos. If I find one I like, i then try it on NDX (looking at win/loss ratio,payoff ratio and profit factor) The addtocomposite has kept me experimenting for hours by adding a new element to the mix.

ParticipantI am using a lower buy limit when market moving down (larger atr drop needed for entry) but haven’t been able to get an index filter to work yet…encouraging to hear its working for you. I think I will revisit it.

Thanks Trent

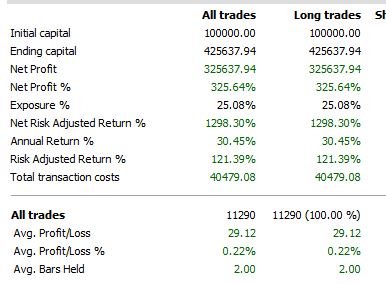

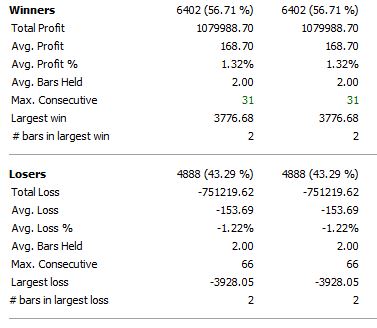

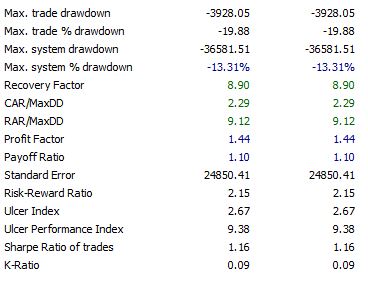

Participant30 positions at 6%

made some changes to tighten entry criteria and reduce selection bias

Participantother stats… single run 2011 to 2016

Participant

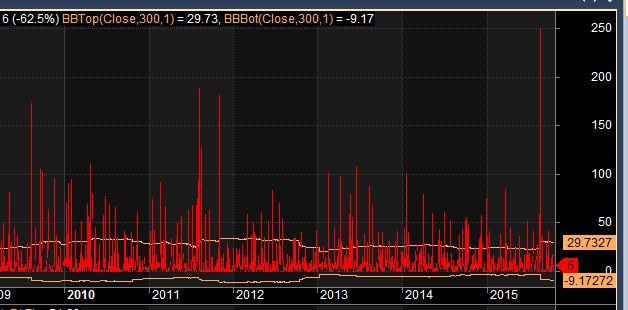

Participantmade some changes to position size and margin….now 30 positions using chart of Darryl’s based on the following (upper BB 1 SD from 300 MA)…any comments/feedback received with thanks

Participant

ParticipantThe other interesting aspect of this chart of Darryl’s is the marked difference in the number of signals generated and hence positions needed to reduce selection bias of a trading system based on 1996-2000 data verses one designed based on the entry signals in the last five years

ParticipantVery very helpful…just used it on my latest system (mark 24…or whatever) been paper trading…quite an eye opener. I thought I was ok as was only approx 40% exposure (on AVERAGE) and seemed ok with trade skip but I can see that I need to be able to have more positions. To do this without a sig drop in CAR I would need to leverage. The tests I have done over the last hour or so show this tends to keep CAR similar but at the expense on increasing maxDD…hmm

The next solution in backtesting for dummies is I guess I need a quantifiable measure of number of positions needed based on the number of trades system allows…maybe needs to cover 1 standard deviation above mean number of trades (for example 1SD above MA)…a rough rule of thumb on the fly as to whether need to tighten entry criteria or increase number of positions ?

ParticipantThanks Trent…that looks the goods too

ParticipantThanks Darryl…I read that post and thats probably what made me think of it….its simply changing it from looking at the LE/potential setups to the number of actual buy orders.

I will try it now.

Participantaim is to create a histogram of average number of days with (eg) 10/20/30/40 buy orders etc so can quickly see visually what number of positions system really needs to be using to try and minimize selection bias

Participantyep….just not sure how to get excel to count the number of buy entries for each day in the 10-20 year output

ParticipantTrents comment on potential selection bias has me thinking if there is there a way to automate/code the number of new positions entered per day for a system like this one over a (eg) 10 year period.?..maybe making an exploration with only a “buy” filter and then sorting the results according to date, copying into an excel file….and then I’m lost….is there some way excel can then look through the date column and somehow tally/count the number of entries for each date? Anyone out there with some excel knowledge point me in right direction please

Might be simple ….will go and ask google…some of you may be doing this already ?

-

AuthorPosts