Forum Replies Created

-

AuthorPosts

-

ScottMcNab

ParticipantAnyone got a good tip for keeping track of cash available in a cash account to avoid violating free-riding rule ? Or is this calculation made clear in the accounts section (available for trading subheading) by IB ?

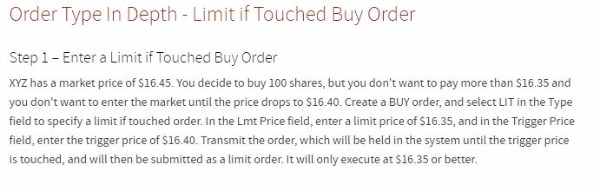

ParticipantSo far so good…should be much cheaper to modify existing api…just need to change order type from LMT to LIT and need extra column for trigger price to be included…rest can stay the same…will ask Levente for a quote

Participant Participant

ParticipantJust tried on ASX and worked ok..I have tried to contact IB to see if can be used in cash account as well as regT but message center temporarily down for maintenance …will post once have reply

if it cant be used with cash acct then maybe could open regT account for smsf and just not trade on margin I guess if regT was needed to use LIT order

Participant Participant

ParticipantIsn’t that the “market if touched” Nick ? From what I can see “limit if touched” triggers a buy limit order or have I mixed it up ?

ParticipantYou make a good point Said but at this stage I am like a newbie golfer…I can hit a 7 iron and that’s it….if I try and switch between a driver or a lob wedge etc it all goes to poo. So for the moment I have to work with the tools I have….which means using the moc system in a cash account for superannuation if possible.

So far, 2000-current MOC with 20 positions at 5% (with settlement delay +3) system returns approx 15% (only 11% from 2011 to current)….I would be very happy with that if I can get it up and running.

ParticipantMiguel Teixeira wrote:Thanks Julian, what I have done is run it through an exploration instead of, as you suggested changing the backtest run, either way it will give the same answer. I am just questioning the logic of dividing the number of trades taken by the total number that could have been taken as the backtest will take that into account as in the simple example I have given.

After writing that though I can think of a few more permutations that will make that logic incorrect, the same goes for how many of the days there have been more buys than positions available.Example:

Day 1 – 10 potential buys – 10 taken

Day 2 – 5 potential buys – 5 taken

Day 3 – 10 potential buys – only 5 taken (max 20 positions) but now I have a selection bias on 5How many of the days have the potential buys been higher than available. Answer = 0%, if using a simple formula of counting the number of potential buys on a day and comparing that to the max position allowed. An additional formula will need to be taken into account to get a cumulative balance and take exits into account.

Anyone out there trading MRV or swing systems have a “work around” they use for the issue of holding trades for multiple days/weeks and how this affects calculation of selection bias?

Systems using positionscore have some obvious advantages

ParticipantThanks Nick. In the US I use SMART and the fills have been good on the open but I have had a bit of a brain freeze and have confused myself why the buy limit order is filled at the ask in those cases when the buy limit is way above the asking price

ParticipantIf we designed a system that allowed buy to occur Mon-thurs and positions were sold on fri each week, would this not avoid problems with the free-riding rule (as proceeds from the sales on fri may be used to buy new positions on monday but then these new positions would not be sold till following friday) ?

If so, then settlement delay could be left out of code too as can use proceeds to enter new positions as we have ensured second security is held until settlement (+3) of initial sale by selling on the friday ?

Think ASX going to +2 I think incidentally

ParticipantRandom question…when we place a buy limit order before the open and then the open is below this prices, what is to stop some party filling this order above the ask but below the limit price ? I thought I read somewhere on IB website that SMART has a requirement that the price is at the displayed bid/ask or better but cant find it now

Thanks in advance

ParticipantResults dont quite agree with US market quite either..

if do backtest on “S&P500” the results agree exactly with the live results for all 17 trades overnight

if i do backtest on “S&P 500 Current and Past” then one of the live trades that the system actually took is left off but the other 16 agree exactly…more work to do hereon a positive note the new system that I started last week made 1.2% more for the night than the previous MOC would have…makes up for last week…swings and roundabouts

ParticipantHmm…qin.au showing up in backtest on ASX on 23 and 24 march but was not an actual trade…when I checked my saved excel files for the batchtrader explorations it was not even on the list as a possible buy on those days…hmmm…can see it underwent a name change recently

anyone found similar ? Can’t see what I have done wrong here

ParticipantIs this a more sophisticated version of what some are currently doing running several versions of Batchtrader through the single instance of TWS ?

ParticipantMy favorite is Aristotle; “Never trust citations on the internet”

-

AuthorPosts