Forum Replies Created

-

AuthorPosts

-

ScottMcNab

ParticipantHi Kate.. I just found this message which is strange…my apologies…the backtest images were from 1995 so the system found this year tought…like the dynamic stretch too…I think i was a tad naive designing this one…have decided to add an exit if stock tanks since previous low

ParticipantI’m still unsure about it tbh. One the one hand when I designed the MRV RUA it was as part of a suite of MOC and 3-4 day MRV systems and so it has no index filter or stock selection criteria that will exclude trades in a downturn. This is fine when the return of the portfolio is concerned and as such the system has not done anything unusual or unexpected in the market that we have experienced.

On the other hand, as Nick has highlighted, this has been an unusual year….but this system did so much worse than it has in years with similar down days. I will (most likely) turn off a system if DD hits 2x previous max historical DD and this system was heading towards that level. I am not considering any major changes but am thinking more along the lines of “just because it has never happened in the past it doesn’t mean it cant in the future”. I am not really keen on going too far down this rabbit hole. I am thinking it may be prudent to simply add a line of code that gradually reduces position size in this particular strategy (even if it results in a slight drop in CAGR) to ensure I do not have a crisis of confidence in the system in the future (no doubt I would turn it off just before it bounced).

I will think on it more. I am keenly aware of the risk that I am potentially making (another) rookie mistake here but am weighing it up against the desire to retain confidence in the system going forward.

Participant

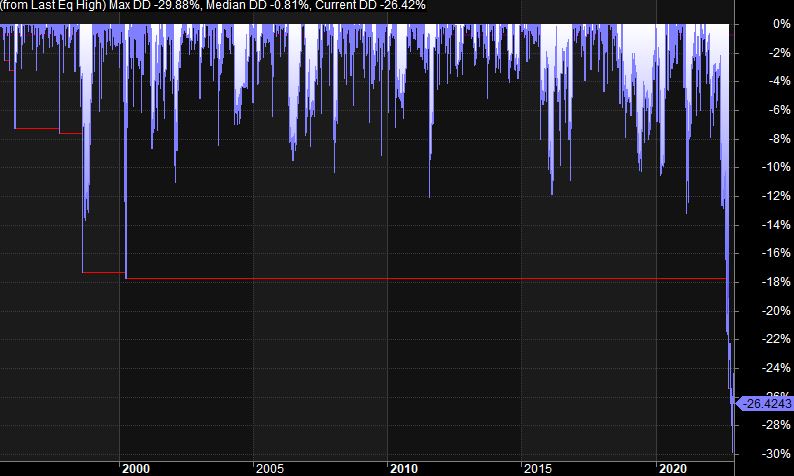

MRV RUA….wtf….

Participant

Participant

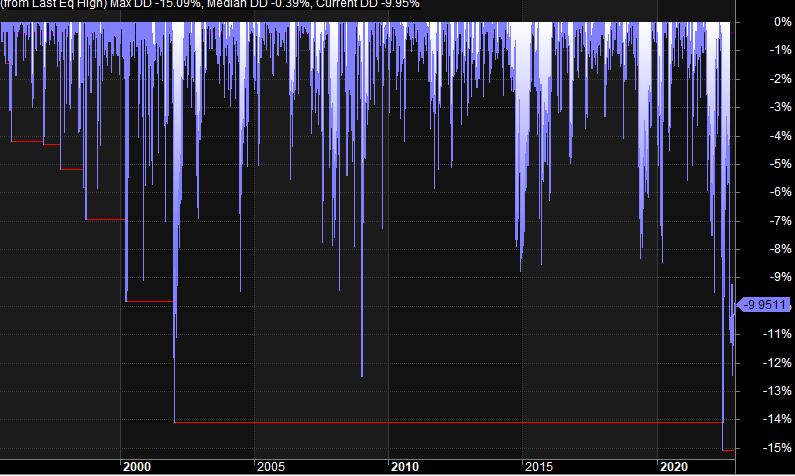

MRV RUI…so far so good

Participant

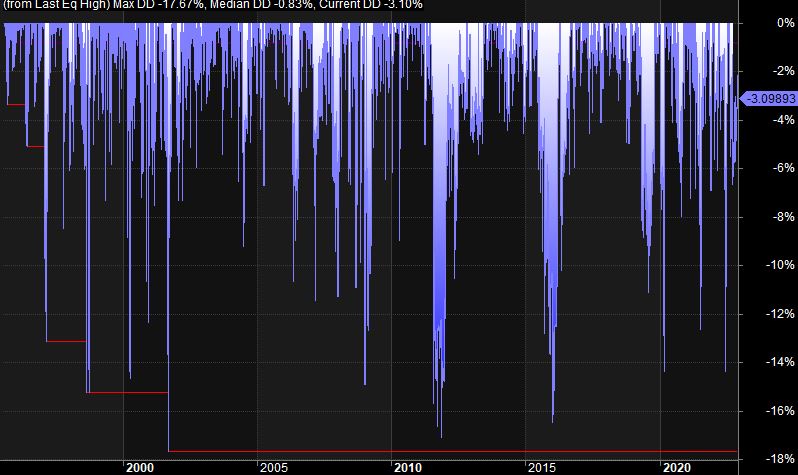

MRV AK

ParticipantSpent most of the year sitting in cash on the sideline so ran back test to see how systems would have gone…most ok but was genuinely shocked at how badly my MRV system on RUA would have gone….trick now is to find out what happened without venturing into the curve fitting trap (first 2 systems ok…the third is the RUA shambles)

ParticipantPun unintended ?

ParticipantI may be remembering this incorrectly but I seem to recall from a few years ago that there was quite a few posts regarding experiments members had performed and possible benefit (in terms of getting live results to match backtests) to be gained for ASX short term systems by testing with the buylimit needing to be a tick lower to trigger a fill in the backtest….apologies for being too lazy to search for it but some (most) here will have a better memory

ParticipantDid you do the system design/testing for the Futures Trend system in Ami or RT Len ?

ParticipantSep 2022

MRV RUI -3.0%

MRV RUA -2.4%

MRV AK -1.3%

MRV SM -2.8%Made a bit of cash back by not being fully hedged USD exposure so account down 0.5% for month…. wasn’t deliberate to start with but then let it run….don’t think will do that again…. what could possibly go wrong pursuing a discretionary system with aud/usd futures…

ParticipantHindsight it wonderful of course but Canadian systems seem to be having a great year….anyone else still subscribing ? Be interested if find similarly

ParticipantAug 2022

MRV RUI -0.7%

MRV RUA -11.1%

MRV USA AK -2.3%

MRV USA SM -7.3% Participant

ParticipantJuly2022

MRV RUI 6.3%

MRV RUA 0.7%

MRV AK 9.8%

MRV SM -4.2%ParticipantI think, from memory, the changes didn’t seem large enough or consistent enough to feel significant….the improvement or worsening for each strategy was pretty random across markets…ie may have been better for USA but worse for AUS and no change for Canada and then also varied across time frames sampled….the size of stretch seemed more critical for MRV systems (ie in the formula var1*atr(x) for calculation of buylimP then “var1” seemed much more important than “x”)

ParticipantJulian Cohen post=13209 userid=5314 wrote:

I have tried to keep parameters as broad as possible. For example if I have ATR as a parameter I use the same ATR(20) anywhere I am going to use that parameter, irrespective of the strategy. I did this to keep things as robust as possible. I’m sure I can make the backtest much much better by tweaking the parameters, but by deciding that this setting is the one only one I am going to use across the board, this stops the temptation to individualise each strategy. Once a portfolio is built I might then see if ATR(10) is better, but it will be ATR(10) everywhere ATR is used, not just on one or two strategies.Interesting…fwiw i went the opposite path (chasing diversity)..if one system uses atr(10) then the next will use atr(5) or atr(20) in the next system….just halved or doubled to avoid curve fitting.

-

AuthorPosts