Forum Replies Created

-

AuthorPosts

-

ScottMcNab

ParticipantYes…normally saves me money as often if filled in last 20 min the price is on a slide into the close….not always …but swings and roundabouts

ParticipantAux price may be the trigger price…a few ticks above lmt price ?

ParticipantJulian Cohen wrote:Scott McNab wrote:better…added 1 line where if index went crazy (atr) it would add a multiplier to the adx filterus moc 2014 current same as before…now down to 5 days where selection bias and reduced on each of those days

That’s a clever idea!

Not sure if Julian taking the piss here but in case anyone is interested other things I tried were:

Index volatility on ROC (not as good as ATR so far)

Index switch filter (briefly mentioned to Nick but he sounded dubious so I have binned it)..idea was when things go crazy then drop back to a smaller (larger cap index)…eg SP500 back to SP100 or from SP1500 to SP500

cond1 = NorgateIndexConstituentTimeSeries(“$SPX”);

cond2 = NorgateIndexConstituentTimeSeries(“$OEX”);

IIf(IndexVola, Cond2,Cond1)use the Mult (see other post) on:

atr filter

adx filter

price filter

volume filter

all of these are trying to make it less likely for a stock to trigger a buy in cases where the all stocks across the board are fallingnext research is to look into market breadth indicators to see if that helps

ParticipantTo find this out Julian I suspect we would need to run two almost identical systems …one using a limit order placed before the open and then another exactly the same criteria but executed using a LIT order…probably over a year ?

ParticipantDoesn’t bother me …in a weird way, as long as I can hit 20% cagr, then the less time I am in the market the happier I am

ParticipantSetForeign(“$SPX”,True);

IndexVola = ATR(2)>2*ATR(50);

RestorePriceArrays();Mult = IIf(IndexVola,2,1);

ParticipantNick Radge wrote:Yep – all lows of the day.been thinking of possible options…may all be rubbish or not apply but am looking to do this myself for aussie MOC:

1. trade XJO rather than XAO…my xao system uses 20 positions at 10% but can get XJO to work if go to 20 positions at 20%..bit of extra volatility but liquidity may make it worth it

2. if trading odd lots (which IB tells me means I am not necessarily entitled to fill as on separate order book) then add rounding calculation to code to eliminate odd lots

3. raise buylimit price by a tick

Participantbetter…added 1 line where if index went crazy (atr) it would add a multiplier to the adx filter

us moc 2014 current same as before…now down to 5 days where selection bias and reduced on each of those days

ParticipantJulian Cohen wrote:Scott McNab wrote:Along the lines of trying to increase the stretch for the buylimit when volatility of index goes berserk perhaps

ParticipantJulian Cohen wrote:Scott McNab wrote:Along the lines of trying to increase the stretch for the buylimit when volatility of index goes berserk perhapsOne problem with that will be the lag. If it missed 9 of 800 days are they days just out of the blue? If so then you can’t predict when they will occur and can’t code for them as the indicators you use reference the day before.

Seems to be when entire index takes large nosedive for a few days in a row…suspect your right and will just have to live with it

ParticipantSaid Bitar wrote:OH i feel guilty all the time when i see others comparing the trades with the backtest and verifying the trades for me i update STT and move on .Damn…this makes me feel guilty…I often just download the file from TWS and tell myself I will get around to updating STT later

ParticipantAlong the lines of trying to increase the stretch for the buylimit when volatility of index goes berserk perhaps

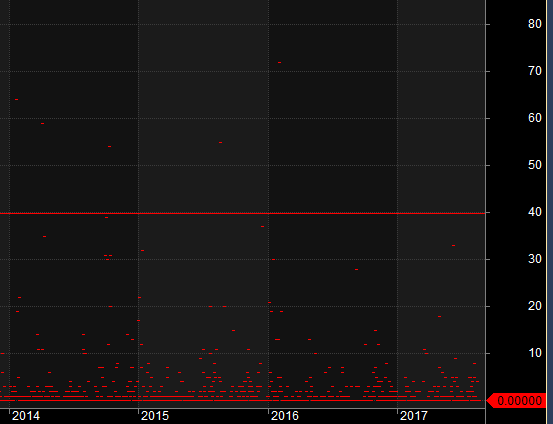

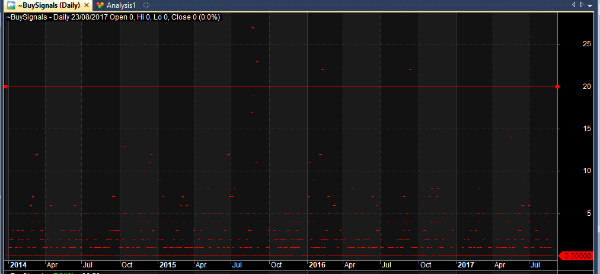

ParticipantI’m still a bit fazed by selection bias…the asx system is pretty good …of the 800 or so trading days in the 2014-current sample there were only 5 that it didn’t capture all the signals and even on those days it went pretty close

The SP500 seems ok on the number of days it captures all the signals (missed 9 of the 800) but on the days it misses it can REALLY miss a lot….wondering if it is worth trying to add some sort of index filter (as these days of huge buysignals occur when the entire index is dropping) ?

Participant

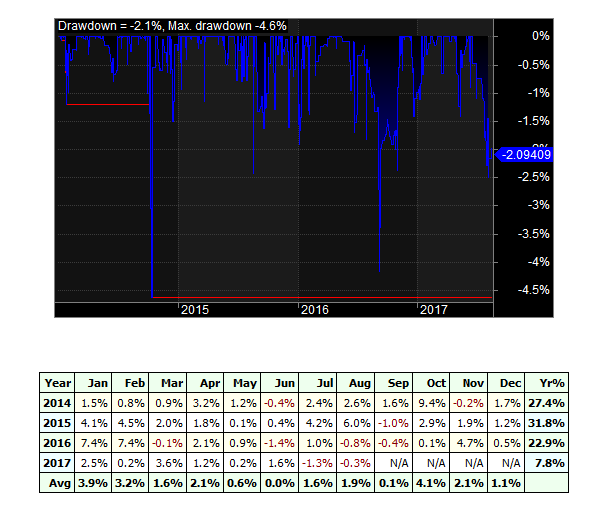

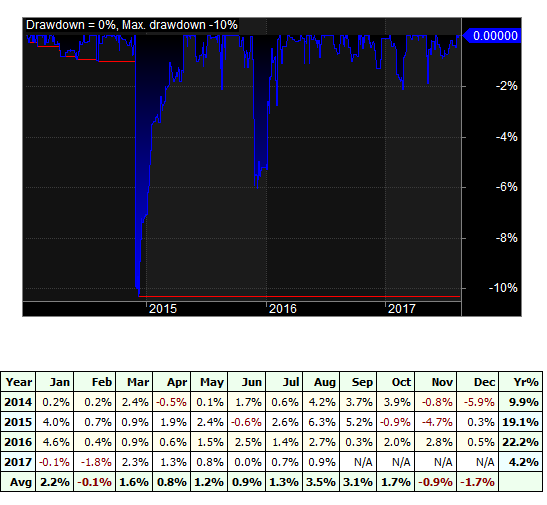

ParticipantSelection bias or not getting fills do you think Said ? Does (eg) 1-June result in live equate to May return for Ami ?

ParticipantDue to not getting filled at low of day ?

Participantonly have moc

SPX

XAO

-

AuthorPosts