Forum Replies Created

-

AuthorPosts

-

ScottMcNab

ParticipantSounds logical to me Rob but then that may be cause for concern.I think the article caught me eye as it was something I had seen in my MRV MOC system.

I have a very similar atr filter in the system I use Said.

ParticipantSPX MOC

trades per year

2000-2007: 619

2008-2016: 544

2011-2016: 534av profit/loss (PS =random/ PS=worst poss)

2000-2007: 0.58% / 0.49%

2008-2016: 0.53% / 0.42%

2011-2016: 0.40% / 0.31%Not as severe as in the post but in line with general theme

ParticipantNot sure if this has been posted/linked but interesting read…something I have noticed with MOC over last few years in backtest too

Broken Strategy or Market Change: Investigating Underperformance

ParticipantAlong that line of though re TF systems, I took some data I had for LSE and ran rotational system over current consituents of FTSE 100…problem with survivorship bias as not Norgate but its school holidays so any excuse to hide in the office for a bit….data from 2005 to 2017…only change to code was UKX as index….results were around the often quoted TF returns… 15% cagr/25% max dd….not going to win any competitions but would take that over the next 20 years

ParticipantNick Radge wrote:You’d need very deep pockets to trade that on futures contracts…Unholy Grails, page 55, had a New Yearly High strategy, albeit long only and without vola position sizing.

Interestingly I actually pulled out my copy and read that section after I read Clenow’s post.

ParticipantJulian Cohen wrote:Scott I believe the idea behind posts like these from Andreas is to demonstrate that a simple system can have great results….BUT it is not as simple as that. As we know from our tests of selection bias, a system with results of 35% CAGR and 10% MDD can look great initially but actually be impossible to replicate in real life. If you posted one of your systems that you had tested with 60% selection bias then it would read the same. Buy when the close is over the 100 day moving average and when the market has had 2 lower lows. Sell on next highest close. That will give you a great CAGR and low MDD but we all know that the selection bias will kill the system.I think Andreas is trying to show you that it is easy to build a system that gives you great results but he always says that to trade it would require more work. This is due to the selection of the markets, and correlation coefficient rules that you might or might not choose. As you have found if you juggle the ETFs in just the right way you can get great results. Add/subtract one more and it all goes pear shaped? Then you know that’s not a system you want to trade.

Andreas goes into the market selection process in his first book on futures trading and how to choose the markets to trade and the various ways you can split them up to control the correlation. It’s a good read.

Thanks Julian. I assumed he would have the equivalent of positionscore in rightedge if he wasn’t using a buystop or buylimit order. The results struck me as too good to be true (how many CTA’s are reporting those metrics long term !!) but I hadn’t considered it may be selection bias….futures are a market I know very little about but I thought I would pop his quote up here as a talking point.

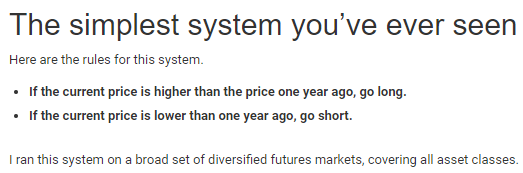

CheersParticipantWas browsing through followingthetrend.com after reading Maurice’s info re Amibroker and right edge…found this

Seems great results for something so simple…and would be great to have some markets not correlated with stocks as has been mentioned in futures and ETF posts previously…

but do the results depend heavily on the

actual futures selected ? I have found I can get results that look great with ETFs if I just try enough variations in the basket of ETF’s in the backtestHas anyone who has backtested with futures tried this rule of Clenows ?

Is another issue the large range of markets needed for diversification making it impractical for the average investor?

Thanks in advance

ParticipantNick Radge wrote:Trend following and strategic positions.Boom …where do I sign up for the Strategic Positions Mentor Course ?

") Participant

ParticipantI had a similar experience back in late March that I mentioned in my progress journal Trent. Hasn’t happened since…still no idea how it happened…in the end I assumed it was human error on my part somehow

ParticipantDid IB suggest placing buy limit order (placed above previous close…maybe 2-3% above) instead of mkt ?

September 6, 2017 at 1:02 am in reply to: Selection bias – how much is too much and general MOC discussion #107616ParticipantMy ASX system has very little SB and was around 18% for worst possible 5 year period…SPX was about 16% …while likely wont get the worst possible result every time, by the time also miss a few trades the results may turn out to be not too far off…time will tell

September 5, 2017 at 7:33 pm in reply to: Selection bias – how much is too much and general MOC discussion #107614ParticipantI would trade a system that produced those results….sounds positive to me Len..if 18% cagr the very worst it could possibly be ..

September 5, 2017 at 12:26 pm in reply to: Selection bias – how much is too much and general MOC discussion #107612ParticipantLen Zir wrote:Julian,

The number of time I have more than 4 buystops is pretty infrequent( selection bias is 98% on my MOC) but it must have an impact since my CAR drops dramatically when I use the worst case scenario codes.Mine drops sig too Len…over 20%…but cagr stays above 15% for worst 5 year period and averages in the mid twenties over 10+ years….so if that is the very worst than can happen I’m ok with it….the drop was much more severe before I added the selection bias filter admittedly

September 5, 2017 at 11:23 am in reply to: Selection bias – how much is too much and general MOC discussion #107609Participantdidn’t copy/past correctly

September 5, 2017 at 9:07 am in reply to: Selection bias – how much is too much and general MOC discussion #107606ParticipantLen Zir wrote:Said,Scott,

September 5, 2017 at 9:07 am in reply to: Selection bias – how much is too much and general MOC discussion #107606ParticipantLen Zir wrote:Said,Scott,

I have been running your worst case scenario codes and have a question.

In my MOC I would like to code so when I backtest I can exclude days when I have more buysetups than number of positions allowed. Currently I can take 40 positions max. I would like to know results of my backtest when I exclude days with more than 40 buysetups.

The goal is maximize my returns on days when I have less buysetups than positions allowed. I believe Nick mentioned this approach on the last mentor call.

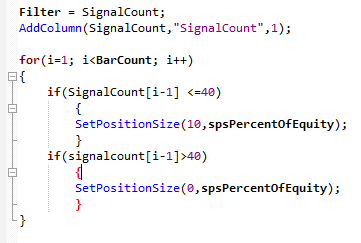

ThanksAddToComposite(BuySetUp == 1,”~SignalsLive”,”X”,atcFlagDeleteValues|atcFlagEnableInBacktest|atcFlagEnableInExplore);

SignalCount = Foreign(“~SignalsLive”,”X”);Filter = SignalCount;

AddColumn(SignalCount,”SignalCount”,1);for(i=1; i

if(SignalCount <=40)

{

SetPositionSize(10,spsPercentOfEquity);

}

if(signalcount>40)

{

SetPositionSize(0,spsPercentOfEquity);

}

}This sort of thing Len ? Julian and Brent posted some stuff in Amibroker afl section…think this code ok but not sure…run scan first and then backtest

-

AuthorPosts