Forum Replies Created

-

AuthorPosts

-

October 6, 2017 at 7:26 am in reply to: Selection bias – how much is too much and general MOC discussion #107817

ScottMcNab

ParticipantNick Radge wrote:Quote:.use API to place buy limits for multiple stocks before the markets open and wait and see if any drop sufficiently to trigger a buy.Scott,

Well, if its a ‘buy on open’ then you are 100% certain to get a fill aren’t you? There is no waiting.Unless the terminology you’re using is incorrect and you mean ‘fill or kill’.

It appears I have used incorrect terminology.. I want to buy the stock on the open if it is below the limit price…using a limit order..limit on open (hence the LOO)

LE = Ref(buysetup,-1) AND (open<=Ref(buylimit,-1) AND NOT OnLastTwoBarsOfDelistedSecurity) ;

LEPrice = open;October 5, 2017 at 8:26 pm in reply to: Selection bias – how much is too much and general MOC discussion #107814ParticipantI will go away and think about this more. I can’t see at the moment how I would know which stocks would gap lower than the buy limit at the open such that I could apply a ranking …thought it would be same approach as current MOC …use API to place buy limits for multiple stocks before the markets open and wait and see if any drop sufficiently to trigger a buy.

October 5, 2017 at 11:13 am in reply to: Selection bias – how much is too much and general MOC discussion #107812ParticipantIn other words, could relax entry requirements significantly…wouldn’t matter (in extreme case) if had more buy orders than available positions every day in a limit on open MOC system (LOO FART for J)

October 5, 2017 at 11:11 am in reply to: Selection bias – how much is too much and general MOC discussion #107030ParticipantNick Radge wrote:Yes, this would be a Fill or Kill order.In essence the system is a little different in my opinion, i.e. the buy limit price is not really the buy limit – its a hurdle where the actual but price must be below…semantics is all.

Essentially the system is buying on an opening gap below that hurdle price. If no buy activated, all orders are immediately cancelled.

I like the idea. Would stop indiscriminate fills on a large trend day to the downside.

As stated in the call I used to trade an opening gap system across all Asian futures markets. My research showed that Asian futures tended to ‘over react’ to a down session in the US and therefore tended to rally off that open.

Is it wrong to think that selection bias not a major issue with a system that buys on open only…if there were 40 buys for 20 positions all at the open then the selection should truly be random ? This would mean a system with limit on open order could increase it’s exposure significantly higher than in systems that had buy limit any time through the day

ParticipantBump…no experience with this…anyone tried ?

ParticipantIf wanted to minimize risk I guess you would use the smallest size possible in the 4x leverage account to meet your goals and allocate all the rest to non-leveraged systems.

If instead were focusing on profits then would try and use largest amount of leverage account that think could apply and survive in worst case scenario based on backtests and pain tolerance

That may be a starting point ?

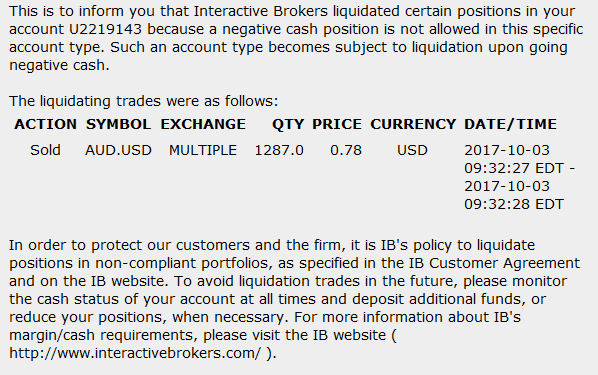

Everyone would be slightly different in their allocation if aiming to maximize profits due to different risk tolerances. If, however, wanted to minimize risk then once determined goal (eg cagr/maxDD) then it becomes more of a mathematical calculationParticipantIB does the currency transaction

and also issues bulletin below

ParticipantJulian Cohen wrote:So my questions are:

ParticipantJulian Cohen wrote:So my questions are:Should I reduce the trend following allocation back to around 60%? My feeling is yes I should.

Is 60% each for the MR and the MOC too much?

Should the MR be half the MOC because of the difference in leverage? I’m really undecided about this and this really is the main crux of the matter. If we are running systems at full leverage what percentage of overall account should we be allocating, bearing in mind the exposure of each system, and the potential exposure for each system. Of course the potential exposure could be 100% but I think we have to work in the bounds of the backtesting model as risk is always there, it is just how we account for it and manage it that is the main thing.Hopefully this will give us all a good point of discussion

I am not sure how to objectively make the decision….. if the same equity is shared between several systems then there will naturally be times when the equity is trying to be in multiple places at once…in other words, the backtests are no longer an accurate representation (maybe out by just a little..maybe a lot eg if TF systems miss a few winners at the start of a trend….who knows?)

How do you decide how much to allocate..normal metrics such as maxDD or the timing of maxDD for each system etc would have changed (by an unknown amount)

Is the 60% based on exposure rather than walk forward or correlation of timing of maxDD between systems ?..cant quite work out where the 60 comes from but exposure seems to be common in the post

As a starting point, if (when) another 20% loss like 1987 occurs, at 4x leverage I think I would like my MOC system to be max of 1/3 of portfolio …but 1/4 sounds even better now I write it down…12 months ago it was 100% (but was only 2X leverage back then)….who knows what I will think in another 12 months

Participant Participant

ParticipantI have been looking at portfolio balance too but from a slightly different way… I feel that the 400% leverage is risky so want to reduce it as much as possible…my goal is 20% cagr for portfolio

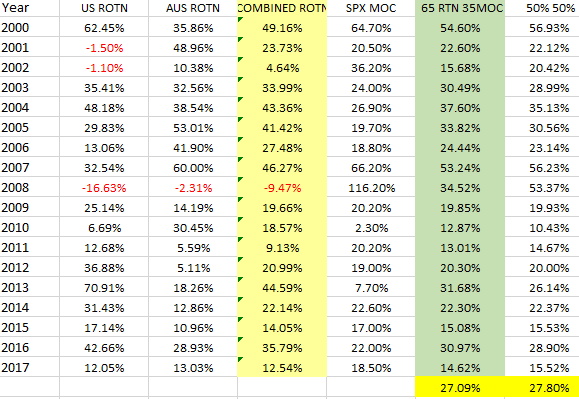

so start with non-leveraged AUS momo and US momo in cash account (can see from table of annual returns not 100% correlated)…once combine AUS and US momo things looking ok (column D)….add MOC (column E)(only SPX in this table but should add in XKO MOC if weren’t being lazy) and looks better (column F and G)..so the balance issue becomes how much can I reduce the highly leveraged MOC and still have it hedge the years when momo go poorly…seems ok 65% momo and 35% moc…(col F)….may even go 75/25

Specifics are not issue…just throwing forward another approach to look at topic

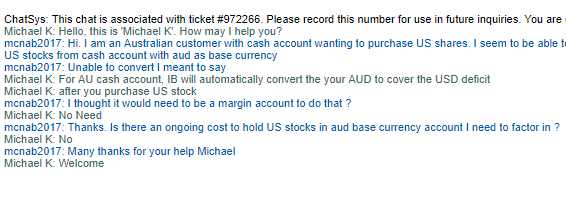

ParticipantFor au cash accounts, ignore IB video/instructions on their website about converting currency to USD before buy stock it seems… will try tonight and see how it goes

Participant

ParticipantHostwinds VPS shut down last night for me…hasn’t done that in over a year

ParticipantNo go….hmmm

Participant

ParticipantOk..I imagine IB will be pretty close in estimating amount to convert

ParticipantThanks Said..much appreciated…I have sent a ticket to IB to confirm but I wont spend any more time searching acct mgt…still makes me wonder at a solution….maybe just submit as mkt order and just ignore all the warning pop ups about trading without market data

-

AuthorPosts