Forum Replies Created

-

AuthorPosts

-

ScottMcNab

ParticipantI am not sure if it matters tbh. My concern (which could be entirely incorrect) was the risk that I was taking a portfolio with 5 to 10 thousand trades over multiple markets and then optimizing it based on two individual equity curves (each of which is theoretically only one of many possible outcomes)….I would be worried if this was even further “complicated” if the correlations were only computed monthly as I would have reduced my sample size of many thousands of trades and could now be making changes to systems on the basis of only 50 or 60 data points. Usually I am down the wrong rabbit hole but that was my initial concern. Perhaps this has been eliminated by the correlations being performed using the (averaged) results of the MC (rather than just the 2 individual equity curves) and are done on a daily basis ? It seemed a potential threat to the robustness of the system(s) with the additional layer of complexity (especially if determined by a small number of data points)

ParticipantHmm..I’ve never really looked at the correlation matrix as I have always had the systems stand alone rather than share an equity pool. I need to read up on how these are matrices are calculated…whether it the monthly correlation averaged over the test time range ?

ParticipantInteresting call Terry

Combining 2 systems from 2010 until now…first on RUI and second on RUA (both systems have 50 k allocated)

when I have maxsamesym: 2 (assuming this means both have normal/uninhibited choice of stocks ?)

system A grows 50k to 533k for cagr of 18.4 (same result as code in the stand alone system…so prob not mucked anything up..yet)

system B grows 50k to 1.8m for cagr of 29.2 (same result as for stand alone code)

total earnings (A+B ) from initial 100k start is 2.35m for cagr of 25.3 (sits between A and B which seems in correct ballpark)when I have maxsamesym: 1 (no other code changes)

system A grows 50k to 517k for cagr of 18.2 (not sure why slight drop as I thought first system always got the pick with RT by default)

system B grows 50k to 1.25m for cagr of 25.8

total earnings (A+B ) from the initial 100k is 1.76m for cagr of 22.8 (between A and B which again seems in correct ballpark)DD almost same for both scenarios

ParticipantThanks Julian…generous as always.. I think I have it for done it correctly for the testing so far

ParticipantHi Nick…on RT now

ParticipantI have thought about it and promptly put it back in the basket labelled “beyond my limited intelligence”….I am waiting for one of the “lodgers” to become proficient at coding and then I will slide it across her desk in exchange for keys to the car or some other bribe

Do you know off the top of your head please how it would output the buy/sell orders ? Would it be as a single csv that I then need to divide into three separate csv files to upload into Chartist API for each system ? Or does it have the ability to generate individual buy/sell CSV files for each of the 3 systems ? Either would work I guess so no big deal either way.. Hmm…I need to have a crack and see what (garbage) I produce.

Good prompt regarding my laziness…appreciated

ParticipantSeems it was my sixth sense…all 3 systems bought NYCB

Participant

Participant3 systems running now at very low acct size

I’m finding it strange and interesting in a slightly twisted way the push back I am getting psychologically …I don’t really seem to want to get back into it…systems have years out of sample and have not degraded in US, XAO or TSX markets… but still

Perhaps it was covid ? I found that time quite stressful…up until then I don’t recall it bothering me too much

I feel like trading at full size is like waking up every morning waiting to see if the stranger at the door is going to punch me in the face or hand me a wad of cash…I could reduce size but it seems to defeat the purpose.

I guess the only answer is to stop whining, suck it up and get back in the ring…but I find it intriguing nonethelessParticipantAnother fun friday night on call as unpaid uber driver for the girls….so played around with back test results

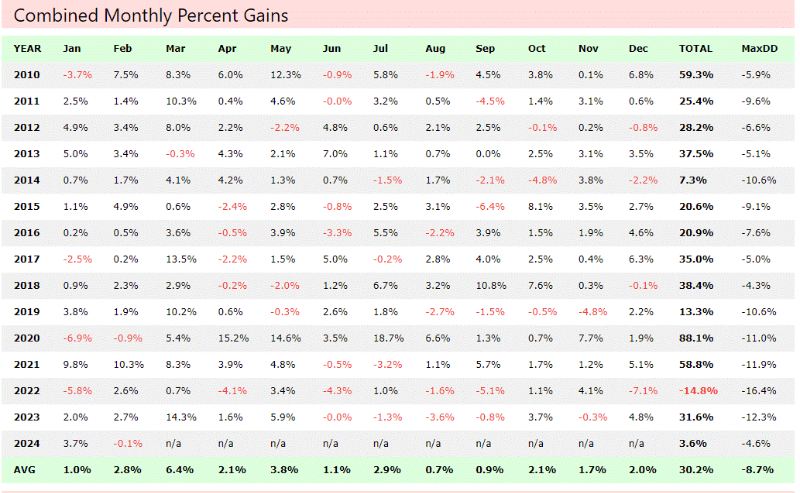

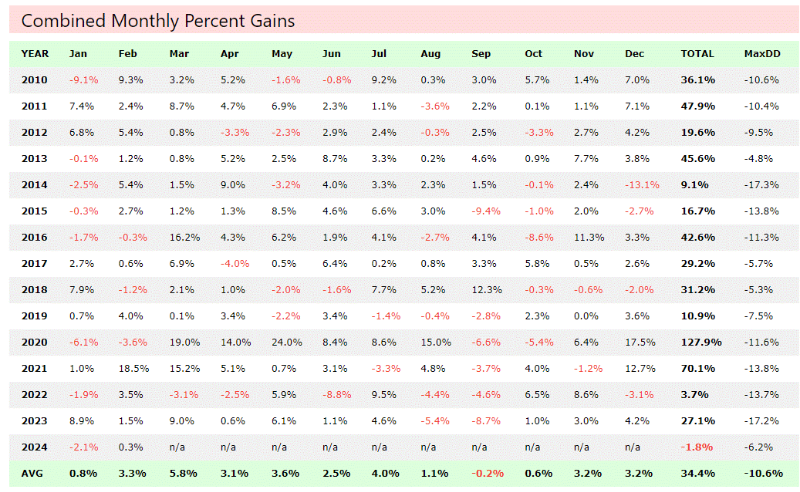

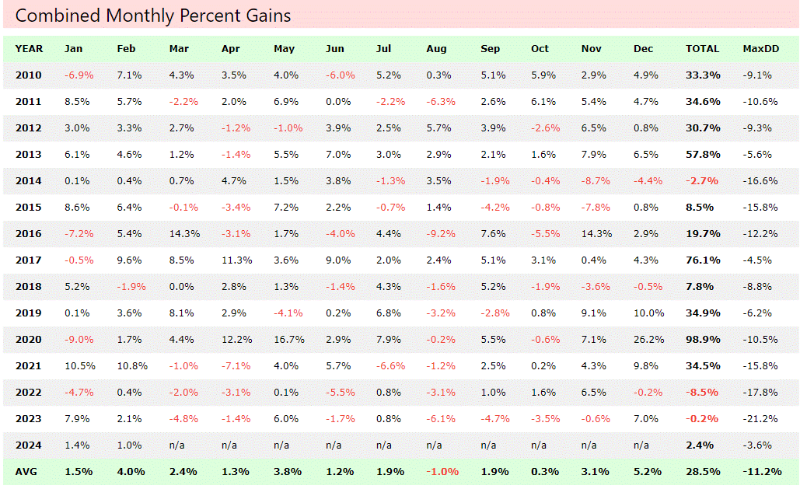

I only have 3 distinct mrv type systems..in practice they are used either moc, mono or mrv (3-6) days with or without leverage and spread between RUI, RUA and USA (much as the same as many here do) but I was unsure how to test the systems against each other per se…. in the end just used all USA as universe and tested as a MRV system without leverage (10×10)…in reality some systems did not achieve these returns as results of the same system on RUI not as good as on USA…anyway…lets see if I can post pics in a readable format

sys1 was designed end of 2016 and traded live since 2017 in different forms (moc, mrv, mono)…I tried to add in the old code (to copy the amibroker delay if missed entry) but didn’t seem to work unless added legacymode:true….which then mucked up something else and I lost interest…so apologies that the results are without that original feature

Participant

ParticipantI think basic pattern was lost money in 2022 and recovered in 2023 but will look further….seeing all the OOS talk a while back on the RT forum I was tempted to post the results of a couple but there are a few individuals on that forum that can be a bit arrogant/abrasive ….my first ever system constructed at the completion of the Mentor Course was designed in 2016 and started trading in early 2017. It has had two changes in that time after I switched from Ami to RT. The first was to add an exit if stock tanked (doesn’t actually improve back test but seemed prudent after covid) and the second was allowing entry following day (v Ami default of waiting until exit signal to be eligible again)…i might back those changes out and compare them

ParticipantNot really happy with return of my etf systems so it back on hold

started live trading MRV system with small account after long layoff…TWS was so far out of date it refused to update and needed re-installation…updates on Chartist API smooth

will continue to monitor results v back-test to make sure I have not missed anything crucial regarding changes in RT code since I was last live….so just the one system at the moment and will endeavour to resurrect the other 5 I used to trade over the next month or two….or three..orParticipantVery impressive to have that conviction/fortitude

ParticipantI have not traded a long term system for many years Paul. Not purely for any philosophical reason…just the ones I came up with were not great and I couldn’t bring myself to stick with them. I have hedged my short term MRV systems with futures at times. I am paper trading a longish term ETF system but I selected aus domociled etf’s so I wouldn’t have to deal with the hedging issue (and the CHESS makes me feel better….which may or may not be true ?). I imagine if I was trading a long term US ETF system I would hedge it using futures with a basic filter similar to what Nick has discussed in the forum (assuming you have access to futures trading acct)

ParticipantVery interesting.. thank you. Great to get new ideas about where to go fishing

Participantboom…what did u decide re currency hedge Paul ?

-

AuthorPosts