Forum Replies Created

-

AuthorPosts

-

ScottMcNab

ParticipantThe guy who wrote above article now also has a podcast called “Flirting with Models”…can only imagine the number of people who arrive at his podcast disappointed to find he is a quant

ParticipantHi Rob…I have taken my laptop with me over the last few years and plan to do so in the near future at least. I have not been going to exotic off the grid places however.

ParticipantHi Matt,

I have an accountant/firm I have been with for almost 30 years in Brisbane. If you are still looking, it may be worth having a chat with him to see if you speak the same language. If you send me an email, I will forward it to him for him to make contact.ParticipantIt’s Rob’s system Tim but I believe so. My understanding is that the decision to turn off a system is not 100% quantitative but is based largely on whether live performance deviates significantly enough from backtest metrics to raise suspicion that either something fundamental has changed such that the system no longer works or that the system was subject to curve fitting in it’s design (unlikely if steps in course were followed). So a system with a 20% drawdown may be perfectly within backtest parameters or may be right at the extremes. My reply to Rob’s post was to try and clarify whether the times he has been unable to place orders due to travel has contributed to the performance. If he has been travelling then he may not have had time to add the CBT code to the MOC system he launched in Aug2017 and that may also produce a positive change.

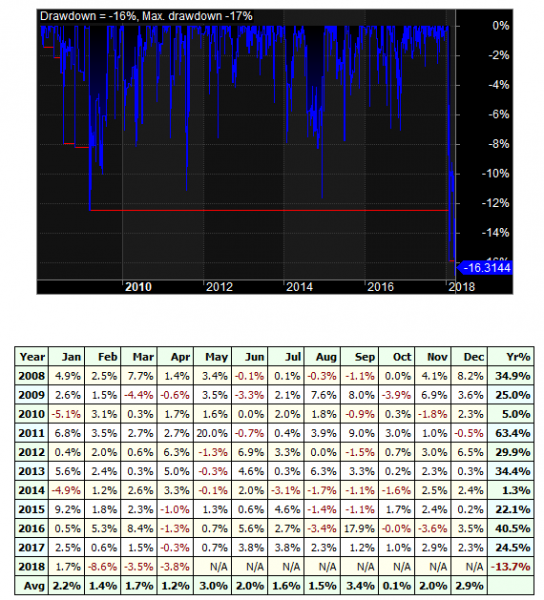

ParticipantRob Giles wrote:Late this month due to travel. Results are as @ 10/7/18:US MRMOC

– 21.76% since inception (16th Aug 17)

– 0.22%% for the period

Times I have questioned the time effort and cost of running this system as I often miss days where I cannot trade due to travel.Best system continues to be the one I haven’t coded (Growth).

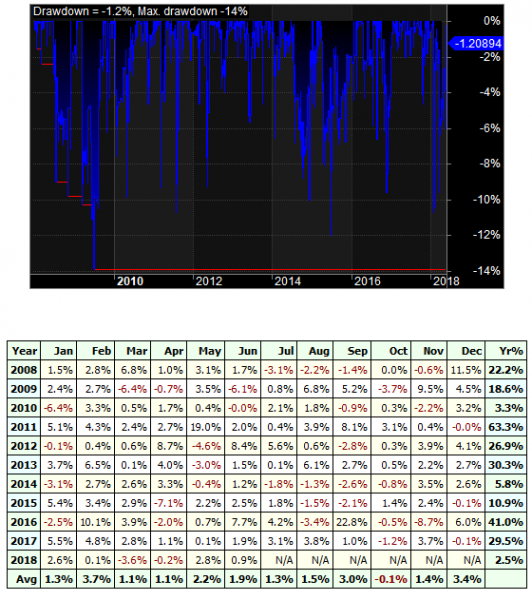

How does the MOC look in the backtest if you had been able to take all the trades Rob ?

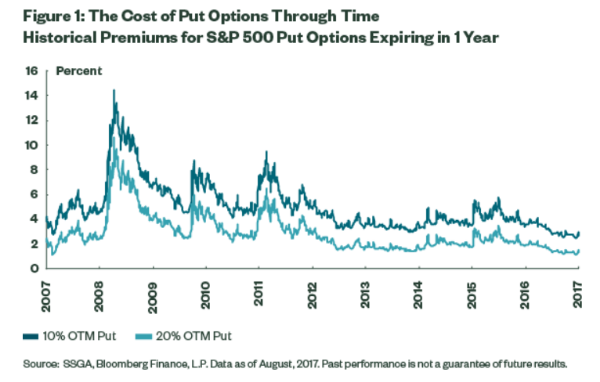

Participantthinking a bit about tail risk and came across this graph…I am thinking about falls greater than 20% (maybe even 25% to make it cheaper still)

Participant

ParticipantOk..found my error….last update from NDU on Friday was done before market close (3.45) and when logged on this morning saw there was data for Friday without realising not the final data…not done that before….have to stop the late nights on Sundays !

Participantstarted CBT on RUI and XAO

was checking backtest and noticed that backtest for today had a trade that I did not take live…further looking indicated that this stock was not even in my DDE that I made this morning before market open…but it is now (for the date 6/7/2018 to 6/7/2018)… don’t recall seeing this in last few years but it is most likely error on my part somewhere rather than CBT

DDE from 6am this morning

DDE tonight at 5pm

Participant

ParticipantI haven’t been able to get a decent result with a rotational strategy on ETF’s Len. This is a MRV (buys at mkt on open) system.

ParticipantHi Len….If you look under “Groups” heading (below Markets) in Amibroker Symbols tab then #4 is ETF’s…almost 3k of them but no “current and past” WL for ETF at this time

ParticipantScott McNab wrote:worst drawdown is always in front of you ?I started paper trading this ETF system at the end of 2017….hasn’t really enjoyed 2018 to date…made me think a bit harder about that statement

I thought this was interesting…when I run the same backtest today….magic…better results…guessing this is survivorship bias in action with the volatility ETF’s that blew up in Feb no longer being in Group 4

Participant

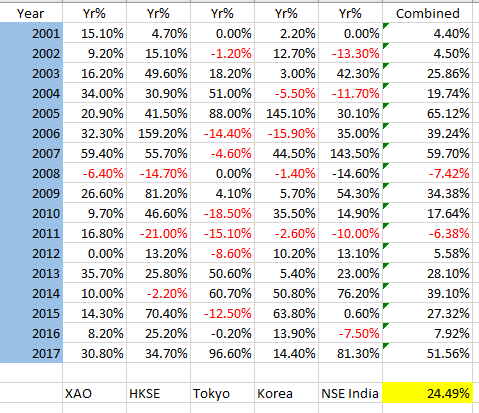

Participantwas a bit hasty it seems when I said on the monthly call on Monday that the Asian markets weren’t that great for my rotation system…the exception is Singapore which is such a dog for both MRV and rotn that it makes me think I have configured something incorrectly or there is a fundamentally different market behaviour

the following results are using the current rotation system I use in US and Australia …10 positions at 10%

Participant

ParticipantJune 2018

RUI LOO 0.7%

RUI MRV 0.0%ROTN

NDX -2.6%

RUI 1.6%

SPX -1.7%

XTO 3.4%Participantconcerning use of eodhistoricaldata for other exchanges:

there are 2 types of api data queries at the moment:

1. historical data for a particular ticker

2. data (eod) for the day for entire exchangeso the initial set up for each new exchange would be a bit of work…download 2000-3000 csv files and then upload them …then repeat for each new exchange need data for

ParticipantAndrew Bennett wrote:The postdictive error is correct. I am only concerned in determining that every order becomes a trade,

That way you take the data into excel ( There trade results are irrelevant)

I just do this to know how many orders existed on any given day.

This performance enhancement is in excel. Scaling up on the days where your orders are less than the max orders.

Its working for me…..so far.Nick trialed a system where position size varied depending on number of buysetups that were generated for the following day…are you doing this on buysetup signals Andrew or on buy signals ?

//

AddToComposite(buy == 1,”~BuySignals”,”X”,atcFlagDeleteValues|atcFlagEnableInBacktest);

Graph0 = Foreign(“~BuySignals”,”C”);AddToComposite(buysetup == 1,”~SetUpSignals”,”X”,atcFlagDeleteValues|atcFlagEnableInBacktest);

Graph0 = Foreign(“~SetUpSignals”,”C”); -

AuthorPosts