Forum Replies Created

-

AuthorPosts

-

ScottMcNab

ParticipantI have always just used the index code for the market I am trading ($xto.au in this case). I have found the index filter to both have a marked impact on trading results and to be more susceptible to curve fitting than other components of the rotational system

ParticipantSaid Bitar wrote:Very interestingAnd what data provider you are using

Metastock has a free trial (1 month?) I believe if you want to try..as Julian mentioned, we installed on separate computer to avoid potentially corrupting Norgate database…even if not planning to trade those markets the data seems accurate enough to expose your systems to some fresh data

ParticipantSaid Bitar wrote:Very interesting

Does TSE work better in Comparison to ASX for MOC in terms of liquidity I know that they should be more liquid

And what data provider you are usingMRV system not MOC so not sure about the closing auction….I agree TSE should be more liquid but different markets seem to each have their idiosyncrasies that are not always immediately apparent…I was thinking of starting with same amount of ASX rather than replacing it…will then slowly increase size and see if hit issues…at worst it should be able to handle the same volume and becomes a useful addition

ParticipantI have been trading the CBT MRV system on RUI and XAO for a few months. Julian and I started Tokyo this month. So far all live trades for TSE MRV system have agreed with backtest exactly. Taking things slowly and only started live on TSE with 2 million (yen).

I did have an issue with an update where the stocks for the LSE folder was incomplete. Early days at the moment….will monitor ongoing accuracy of data but so far so good.

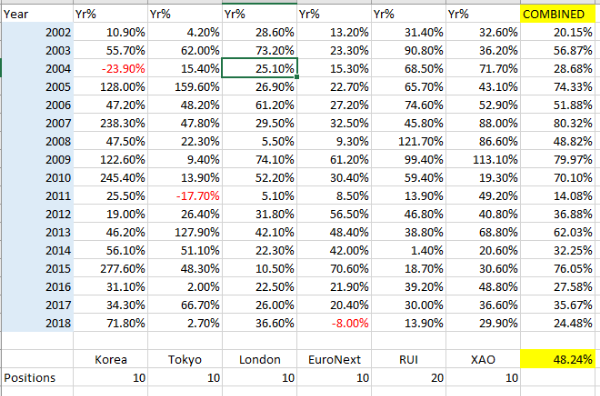

Had to eliminate HKSE and National Stock Exchange of India as Julian mentioned due to issues with variable batch lot…disappointing as both tested very well. At this stage, likely future candidates are LSE, EuroNext, and Korea. One breakdown may be 50% RUI and 10% each for remaining 5 markets.

ParticipantPreviously I posted results using Metastock data for the rotational momentum system

Here is the same table for the MRV system I use. I use the same system for all markets (except price/volume filter)

Participant

ParticipantMost seem 3 or 4 letters without the .L

https://www.interactivebrokers.com/en/index.php?f=2222&exch=lse&showcategories=

ParticipantMarket On Close…..system exits at end of each day

ParticipantA man after my own heart..I too struggle with technology and am in my third year here (reflection of my shortcomings….not the mentors). The templates for the systems at the end of the course are gold so don’t panic in the next few months. Sadly, for me coding is still a bit like reading a foreign language when on holiday…I know enough to find where the toilet is and how to get to the airport but attempting something more complex is always going to raise a few eyebrows. I am turning 50 and enjoy thinking how one day I will be fit and active. All the best.

ParticipantJuly 2018

MRV CBT

RUI: 6.5%

XAO: 3.7%Rotation

NDX: -0.8%

RUI: -1.3%

XTO: -5.7%ParticipantIts not a direct answer to your question Matthew but an improvement may be achieved by reducing the volume for each order…you may be at the limits of what can trade with this type of system without moving the market. Does your system test ok on other markets? I am running my MRV on RUI but it also works well on RUT excluding RUI…so could halve the volume by constructing 2 markets from RUT…hopefully this would reduce impact.

ParticipantAs a rough rule, the larger the ave proft/loss % the better of course but I would focus on raising that for the in-sample testing before going oos.. imho at the moment it is a bit skinny

ParticipantGood point Trent.

ParticipantLink to free download on book on Trend Following by Niels Kaastrup-Larsen (manager at Dunn and hosts the podcast “Top Traders Unplugged”)..

https://toptradersunplugged.lpages.co/frank-optin-the-many-flavors-of-trend-following/

ParticipantI agree…just thinking that if this was significant effect then would only see a drop in the last week of Dec, Mar, June etc rather than every month as was suggested previously for rotational systems…

a variation on the “sell in may and go away”…

instead short the monday of last week of dec/mar/jun/sep…cover the first trading day of the next month (+/- Index filter)doesn’t quite have the same ring to it

ParticipantWonder if testing only a week or two before the end of each quarter would make a difference ?…have heard it said that managers like to dump their under performing stocks before the end of the quarter so don’t have to explain why they hold them

-

AuthorPosts