Forum Replies Created

-

AuthorPosts

-

ScottMcNab

ParticipantMight be easier to focus on one system type at a time (mean reversion or momentum/rotational) and do a deep dive into the system to get your head around the intricacies of what makes each one good or bad. I remember feeling really under pressure for time but in retrospect would advise focusing on just one for however long it takes…but that was just me of course

ParticipantI’ve been exposed as a fraud coder again…I just clicked on a template excel gave me…bloody coders !

ParticipantHave been impressed with Said’s chart…so experimenting over next few months

Jan 2019

ParticipantLen Zir wrote:Now that our trend following systems are out of the US market I would be interested in knowing what people are doing with their cash.

ParticipantLen Zir wrote:Now that our trend following systems are out of the US market I would be interested in knowing what people are doing with their cash.

In my retirement accounts I have 30% in BND 5% in GLD the rest in cash

In my personal accounts I have 8% in US moc and the rest in cash.The best use I could find last year when tested various options historically was to actually use the funds in the MRV systems…but while gave best return (by a significant margin) it obviously came with other issues so I am in cash..depending on individual circumstances some people may allocate a portion to short term over those times perhaps?

ps I should have mentioned that testing on MRV was done with no leverage (10×10) with settlement delay included

ParticipantWe’re just jealous Mike..and its simpler to hate the coder than blame ourselves

ParticipantTrent Rothall wrote:Not sure how everyone else trade frequency is tracking but i’ve done 3 trades since 1/12. Very quiet. Had to check that i was actually running my MR correctly!Also slow here…picked up a few in last day or two though

Since 1/1/19 mrv tradesXAO: 5

RUI: 8

RUT: 12ParticipantThanks Nick. I might be barking up the wrong tree again. I was wondering if the “average” and the “spread around the average” would be a measure of robustness that could be used in the process of system stress testing and selection. I am not thinking of trying to trade an average of the days. Of the two systems I trade, for one of them the first day of the month is consistently the best result over all the time frames and for the other the first day of the month comes in about middle of the range over all those days…made me feel better about the second system and a bit concerned that I have cherry picked the first one.

Enough time spent…time to move on

CheersParticipantNick, do you think it is too much of a stretch or just plain wrong to think that the system that has the least variation in stats over the 20 different trading days may be more robust ? I was thinking of using it as a means of differentiating between systems which are otherwise pretty similar.

To clarify my thoughts, I am wondering if I have inadvertently selected a system that looks better than it is going to be going forward

eg

System A has a 22% cagr and maxDD if traded on 1st day of month but the average over all the days is 16% with 28% maxDD

System B has 16% cagr and 26% maxDD when use the first day of the month but the average over the entire month may be 19%/26%ParticipantArticle got me thinking a bit more about robustness…how a rotational momo system without the highest CAR may be better on basis of robustness

I tried optimizing a couple of different systems….not by optimizing a setup condition or filter but using the trading day of the month(0-20)…not for the reasons Larry Williams does but more to get an idea of how dependent the results were to my choice of using the first day of the month by default….found for some systems the variation (eg car/maxdd) was minimal and in others it was significant.

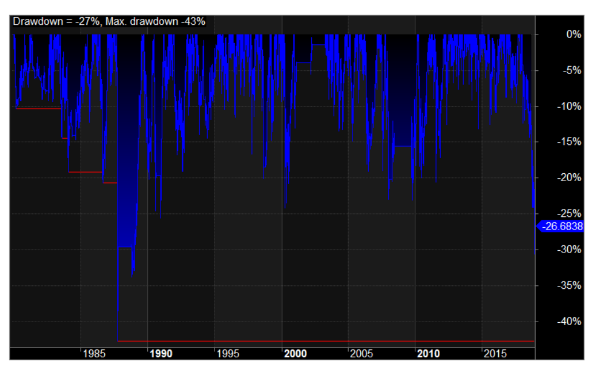

Participantdrawdowns

Participant

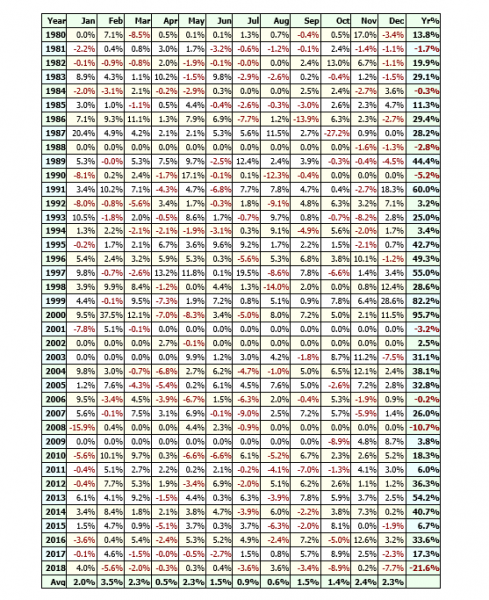

ParticipantWas interested to see how badly 2018 sucked for my US rotation systems so changed it from RUI the SPX and tested back to 1980

Not the worst DD (1987 still ahead)….

its tempting to try and rationalize that 2019 will bounce back …lucky don’t have to try and guess ..just place the tradesParticipantDEC 2018

Rotation (%)

NDX -11.2

RUI -6.3

XTO 4.9MRV (%)

RUI -1.1

RUT -3.4

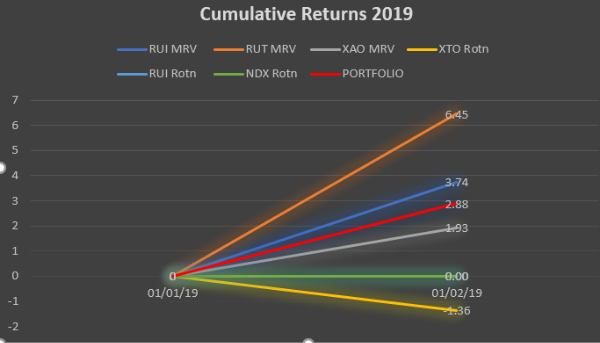

XAO -0.8Happy New Year

ParticipantThe MRV systems with hold times of 3-5 days seem viable alternatives even without any leverage Dustin…gets you into that 15-20% range and often the returns have low correlation to the rotational momentum systems. I used to be 4x MOC but use 2x MRV now along with rotational momentum systems….whatever lets you sleep easy…go with your gut ….”(insert favourite cliche here”)

ParticipantNOV 2018

Rotation

NDX 0.7

XTO -10.4 (thought Oct was too good to be true)

RUI offMRV

RUI 3.5

RUT 1.1

XAO -1.5November 6, 2018 at 9:22 am in reply to: Migration to IB Australia Pty Ltd: Margin Restrictions for Retail Accounts #109389ParticipantJulian Cohen wrote:What’s Settlement Delay Scott?Settlement delay if using cash acct (T+2) to avoid violations

setoption(SettlementDelay,2);

Also with RUA I think you might find actual fills won’t meet expectations.

Its a concern for sure. I have been trading RUT (20 positions at 10%) for several months now gradually increasing size and so far so good….on that basis was anticipating that using RUA (10 at 10) with even higher hurdle for turnover and volume filters should work too (aiming for top 2000 rather than the current bottom 2000 with RUT) .

..not sure when the tipping point will come when partial fills and/or slippage will become an issue…… and not sure how to work that out other than by slowly stepping my way up and monitoring ?

-

AuthorPosts