Forum Replies Created

-

AuthorPosts

-

ScottMcNab

ParticipantWent through some of the trades and read post in detail several times

Early days as only worked on the idea for an hour or so

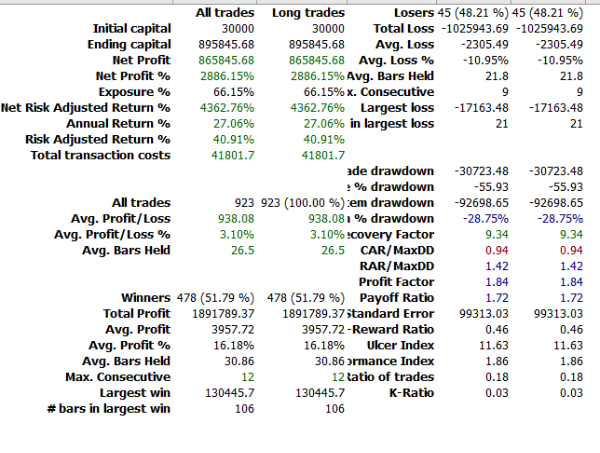

Results are for filters set to price> $1, 500k min turnover and volume and with MA(volume,20)>500k

Looks promising. Thank you for posting Nick

Participant

ParticipantCouple of things I noted.

The exposure at 56% caught my eye..and only 34 trades a year…lower than the rotational systems I have been trading (and allows up to 14 stocks)..win rate is good too…will explore this more as taken together indicating system is very selective in trades entering

No detail as to what actual liquidity filters are unfortunately…would have loved to see this (I might work through the trade list stock by stock when get time to try and gather more insight).

With system I am currently testing on XAO over these dates (previous live results been on XTO) then get (cagr/maxDD):

price $1 and turnover 100K: 24/-27

price $1 and turnover 200k: 22/-27

price $1 and turnover 300k: 21/-27

cagr drops further still for me (into high teens) if include MA(volume,20) filterother stats for Helix Trader system (cagr/maxDD, profit factor and payoff ratio) all good….like really, really good

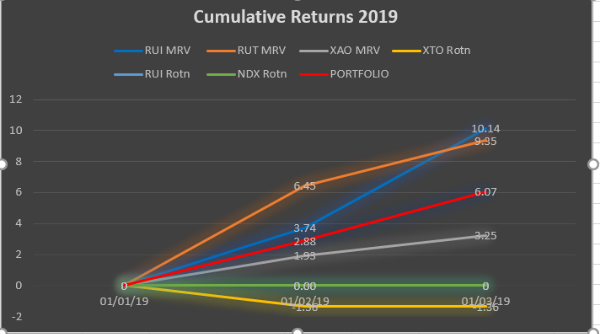

ParticipantGood news Rob as long as are matching. I try (not always successfully) to not worry too much about relative performance with other systems ..my MRV doing ok this year but this snapshot doesn’t tell the whole picture…they are all coming off significant drawdowns from Oct so were due for a good run based on probabilities…the XAO MRV is still not out of the drawdown yet

ParticipantThanks Nick. I will go ahead with Tradestation then.

ParticipantThanks Nick. I opened a Tradestation account a while back but haven’t funded it yet. I was trying to do some more homework on them before I did but the reviews of different brokers on the web are so conflicted with all the mud slinging its hard to put much credit in any of it. I was wanting to move some of my longer term systems over to another broker so I don’t need margin….just access to US stocks without paying excessive costs. Choices seem to be:

Tradestation (generally ok reviews)

Saxo CM (quite negative reviews)

Charles Schwab Australia (also not great)

Have your interactions with Tradestation been favorable on the whole Nick ? Or have any US residents on the forum used them?ParticipantI have unsuccessfully been trying to implement a variable lookback period to a breakout system since listening to it…maybe it works better on futures than stocks…. (better than the alternative !)

ParticipantI suspect you have copied one of my earlier metastock codes from a decade ago

ParticipantBoom….11%

ParticipantYep…just excel…I’m hoping it will give me a better overview than the numbers alone do over the years

rotn system on ASX would have done 9% for the month …gotta laugh……..amazing how it (trading) can mess with my head in ways I never imagined…I find myself repeating the mantra about the next 1000 trades at least every week…all goes back into perspective

ParticipantFeb 2019

All rotation systems offline for changes..

ParticipantLen Zir wrote:Glen,

ParticipantLen Zir wrote:Glen,

Ran my MR strategy from 2007 to present on R1000 using the ADX filter. CAR went from 34.97% with 25.4% drawdown with SPX index filter to 48.58% but with a 39.7% drawdown. I don’t think I could stomach a 40% drawdown.

Will play around with some different entry criteria.Another possible solution to try Len is to vary PS

eg

remove IndexPass from buy conditions and change (assuming 20@10%):SetPositionSize(IIf(Ref(IndexPass,-1),10,5),spsPercentOfEquity);

ParticipantWhat market Glen ? If it is R1000 or SPX then might be worth testing on R2000 as well? I run MRV systems on RUI and RUT separately (same code) as a way of dealing with the different liquidity between the stocks in each index..have 2/3 of US MRV funds allocated to RUI and 1/3 to RUT …..but RUT is still trading same amount as my ASX MRV and has had fewer partial fills than ASX system (although has been minimal in both really)

ParticipantWould love to have a MRV on short side but no success so far…better go back and have another look

ParticipantFingers crossed US and Chinese delegations play nice over the weekend

Participantmid to high 20’s Rob.

-

AuthorPosts