Forum Replies Created

-

AuthorPosts

-

ScottMcNab

ParticipantInteresting !…thanks Trent…will look into it

ParticipantIf not using CBT you may just be able to add

SetOption(“SettlementDelay”, 2);

Best call Craig I guessParticipantJulian Cohen wrote:I keep my own spreadsheet alongside of STT so I use that.My MOC did over 500 trades in three weeks so I’m not gonna manually log everyone of them

slacker

Was wondering if difference could have been due to currency conversion

ParticipantI keep a paper diary where I write every entry and exit in MRV so can compare with AB backtest and STT….in last 6 months since went to IB Aus (using RUI) I have done 88 trades and not missed a trade ..(well…not quite true..only trade I missed was on a Friday night when forgot to place orders due to appt with Mr Guiness but who wants to admit to that)..have had one partial fill in that time

What are u using for calculation of actual…STT or IB ?

ParticipantTrent Rothall wrote:Scott, i haven’t come across this problem yet, i really only went 10 by 10 mid month. But from what i can see that is the only option.Thanks Trent. I gave up my XAO MRV when I went to IB Aus as couldn’t get my head around it all…didn’t know what impact placing buy order 5-10 min after the open would have on system profitability… and not laid back enough to give it the time to play out

was also confused about T+2 settlement delay …the testing I did with settlement delay showed it wasn’t as easy as just using the SetOption when using CBT… I think you said not using CBT so dodged that issue I guess

Congrats again…100% quite a milestone

ParticipantCongrats Trent !!

On the days you have to sell and buy, do you have the buy orders delayed to 10.09:30 or something similar ?ParticipantNov 2019

RUI MRV 3.2%

XTO Rotn 3.3%ParticipantNup….thanks Nick

Participantjust ran that system over NDX as remember did quite well on that when designed it

Participant

ParticipantWill keep an eye on it..some of it seems to come down to universe of etfs select

On another topic…did anyone else have any execution issues on US overnight ?….when checked at 3pm (New York) both TWS and API running fine but all orders on API had been cancelled…

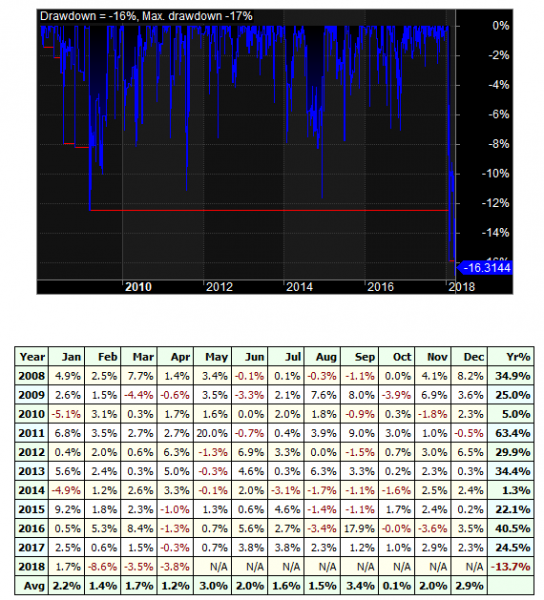

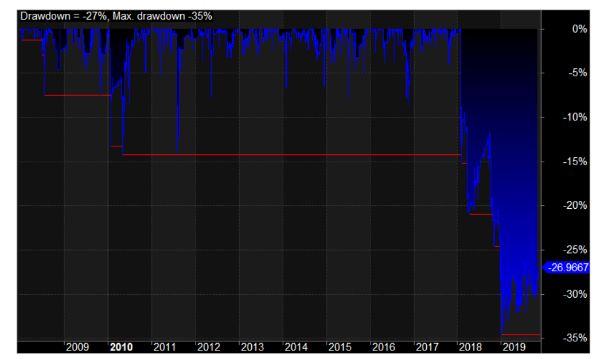

ParticipantScott McNab wrote:worst drawdown is always in front of you ?I started paper trading this ETF system at the end of 2017….hasn’t really enjoyed 2018 to date…made me think a bit harder about that statement

always interesting to go back and test the systems in the graveyard

glad didn’t start with this one…was tempted in Jan 2018 when hit -16%

i was thinking must have just been case of curve fitting…then remembered ripped idea of a Larry Williams book and designed system for stocks and then decided to see if would do ok on etf….at the end of 2017 when first tried it on etf’s it looked great

ParticipantJulian Cohen wrote:Follow up from Alera:I’m in two minds. I like the idea of setting it all up on Sunday and then leaving it until the following Saturday. But I also like to double check the trades each day against the backtest, and scan the entries for the next day, plus correct the odd tic issue.

Makes me break out in cold sweat just thinking about how badly I would screw this up

Participantas a start…

EOM = Month() != Ref(Month(),-1);

TradeDay = BarsSince(EOM)==15;

PositionScore = IIf(Year()>=1990 AND TradeDay,score,scoreNoRotate);doesn’t account for public holiday ?

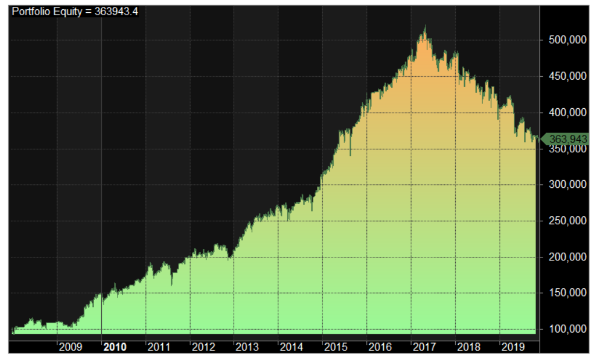

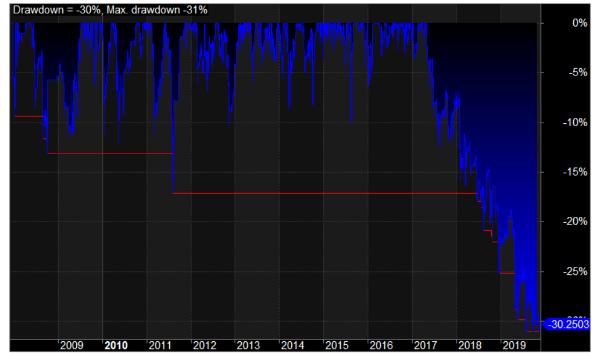

ParticipantMichael Rodwell wrote:Quote:Nah…just thought the difference in the decades 2000-09 and 2010-19 may well be reflection of ASX performance rather than your system…maybe SPXWithout tweaking it at all it does pretty ordinary…

15% CAR, 30% DD…

Personally don’t think anything wrong with that…think the tweaking can over-inflate expectations sometimes…solid returns on data never seen

ParticipantMichael Rodwell wrote:Not sure why I kept that subject line…What universe you want me to try? Any specific?

Nah…just thought the difference in the decades 2000-09 and 2010-19 may well be reflection of ASX performance rather than your system…maybe SPX

-

AuthorPosts