Forum Replies Created

-

AuthorPosts

-

ScottMcNab

ParticipantMichael Rodwell wrote:Scott McNab wrote:After starting XTO rotn system middle of last year it went straight down into 12% drawdown…finally back in black

Apologies to all for imminent correctionPerfect timing Scott. Im just about to launch my ASX rotational system.

Shall we crash the market together?

Wow…its all lining up for the big short

ParticipantDon’t Ignore the Ozzie ?

ParticipantAfter starting XTO rotn system middle of last year it went straight down into 12% drawdown…finally back in black

Apologies to all for imminent correctionParticipantMaybe

EOM = Month() != Ref(Month(),-1);

score = Ref(Rank,-1) ;

Score = IIf(LE,score,0);

TradeDay = BarsSince(EOM) ==15;

PositionScore = IIf(Year()>=1955 AND TradeDay,score,scoreNoRotate);Please test/verify….and all that stuff

ParticipantHard to know if market changed…certainly possible crowded space as more people look into MRV systems…or HFT may have changed landscape…etc etc

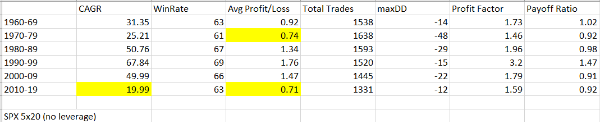

I tested my mrv on spx (using 5 positions at 20%)…last decade the worst but not all that different to the 70’s….in another decade we will know more..:unsure:

Participant

ParticipantDaniel

At the risk of sounding like a broken record I will explain my approach to this problem. What is needed is a definitive test to allow you to decide if you will continue to trade this system. Stay with me as I digress for a minute and I will come back to the test I use.

I currently believe that the most likely problems I will encounter arise from either

1. curve fitting or

2. obtaining a good result (back test) purely by chance (having done over 15,000 back tests in the last year months this is highly likely).

There is also the possibility that

3. markets will change fundamentally in the future such that my current systems no longer work.The only solution I could come up with to try and detect these problems and avoid them is using a technique that is applied initially in the testing phase and subsequently in the monitoring of the live performance of the system. My current solution is multiple markets. For me to continue testing any system, it must have similar expectancy (not cagr) in all markets or I throw it away. I have discarded several systems that were excellent for US or AUS markets but not both. Am I throwing out good systems? Highly likely, but I see it as the lesser of two evils. I would rather toss out a good system than risk trading one that has been curve fitted or obtained good results simply due to chance.

Performing this test on multiple markets in the design stage then allows me to also use this as a method of monitoring live systems. If the system performs poorly in one market but continues to perform well (paper trading) in the other markets then I will continue to trade it. It was a source of reassurance for me in 2019 when my US MRV system tanked in May that the system trading XAO did not. I also test and monitor my live systems on Tokyo (always enlightening), Korea, Hong Kong and London (problem with survivorship bias notwithstanding) but then I am particularly paranoid about losing my savings. If a live system performs poorly in one market but remains acceptable in others then I will continue to trade it.

In your case, I would start with NDX (always makes me nervous as such a small group of stocks with exposure to limited sectors), then move to RUI excluding NDX and then RUA excluding RUI (RUT)…again looking at expectancy (or win/loss rate, average profit/loss %, PF and payoff ratio. If you have ASX data then obviously that is good. I like to test on SPX back to 1960. To me, the extra (tax deductible) cost of the subscription is money well spent.

I have not been able to come up with a better practical test to make these decisions.

ParticipantDaniel Baeumler wrote:Thanks, Scott.

What do you mean with using ‘unseen’ data?Not sure if u have run the system on asx (or spx before 1990)? If not then this would be unseen data…I am thinking about eliminating any potential concern regarding curve fitting as the cause of the sudden drop.

ParticipantHi Daniel,

Could try running it on unseen data (SPX back to 1960 or asx 1992-present) ….if ok on unseen data then it will give u confidence it was just a bad year…Just out of interest..noticed average hold almost 8 days…..what is ave bars in winning trade ? Does adding an “n” bar exit help system at all?

ParticipantNo prob with IB…just had to open a couple of new accounts, then link to FnF acct, then shuffle money around from old accts to distribute some into new ones

ParticipantDec 2019

no MRV trading as house keeping with IB accts

XTO Rotn -1.5% (was looking better yesterday)Happy New Year

ParticipantRUI

price $1-200

vol/aveVol/turnover/aveTurnover all 1M

entry: buy limit

positionsize: 20k USDresults July-Nov2019

AB back test:

89 trades/PF 1.64/PR 0.83

Live:

88 trades(forgot to place order 1 nights)

1 partial fill

PF 1.59/PR 0.84ParticipantMatthew O’Keefe wrote:Is 5% limit a good number to use? Maybe. That’s what I use for this part of testing. I think the default in Amibroker is 10%. Some people don’t even like to exceed 1% of the daily volume.

No doubt varies for systems, market and the orders using with it…issues that have been raised multiple times…how large can the orders be before live results deviate sig from backtest ?

might be helpful to start a new post where people (if comfortable) can post the results of live systems with respect to position size..ie what they have traded successfully….is a sensitive topic tho as introduces element of personal finances….in a mature private forum like this people may be comfortable sharing ? Break down into

MOC

MRV

Rotn (buy on mkt open?)

TF (buy stop, MOC etc)ParticipantOr maybe keep the $1 min to get exposure to the larger % moves but compensate with turnover filter ?

Participant2 n’s..as in sinning ..

I have R3000 system going live 1Jan…tests are with price/vol/turnover at $1/500k/1M …what are u using live J ?ParticipantDustin Johnson wrote:Also, has anyone done any intraday testing with Amibroker. This is one of the reasons why I am considering looking into Python more. I would like to test a MOC strategy that automatically hedges market exposure but shorting the index in proportion to the long exposure taken on the MOC trade.Another option may be to use futures to short the index ?…develop a system that goes short on breakout to downside…these are the days MOC would be loaded up…can test using tradestation intra-day data but would need to learn easylanguange

-

AuthorPosts