Forum Replies Created

-

AuthorPosts

-

OmarAouane

ParticipantOk

I will then") Participant

ParticipantThanks Said for the answer.

My problem for volatility position sizing is more related to which reference should I take to establish the risk size.

I made some the reasearch and I seems I should decide the daily impact i want each stock to have on the portfolio ( in this case 0.15).

Still not very clear tough, as I get some very different backtest results for a small change in risk allocation percentage.ParticipantHello,

I write on this thread as the topic is postion sizing. I am currently struggling to grasp the concept of risk adjusted sizing.Nick, sent me the following formula as risk position sizing :

Risk = 0.15*Ref(C,-1)/Ref(ATR(20),-1);I cannot visualize how the close divided by the ATR end up giving me a percentage.

When I use it I am often using leverage versus equal weighted position.

Sorry if the question seems stupid.

Thanks guzys.ParticipantThanks Nick.

almost fully recovered.

I ll have to evaluate the yearly costs of running the account and then decide.ParticipantI think I found the issue, not sure if you experienced something similar.

Basically, If the stock is added to the universe ( for ex S&P500) less then 50 days ago, you cannot calculate the 50 day moving average hence it gets excluded.ParticipantHello,

When running your MOC systems between AB and RT, do you find any small differences in trades between the two softwares?

My statistics are slighly different too ( using compound equity in both cases)And Big shout out to Trent for having posted a template on the forum.

It was very helpful!ParticipantHi Guys,

Currently recovering from Covid so I was kind of slow lately.

I intend to start live trading next month and need some advise regarding the use of API for MOC systems.

Can you direct me to some resources how to use and implement the API between AB and IB?

Thanks a lot

OmarParticipantsorry to see that Seth… I didn’t mean to jinx you

hopefully it was a small account…as they say you are not a true trade if you haven’t crash couple of accounts

good luck!ParticipantThanks a lot Trish!

ParticipantHi Nick,

Unfortunately this presentation is not available anymore.

Any chance to have it reposted?

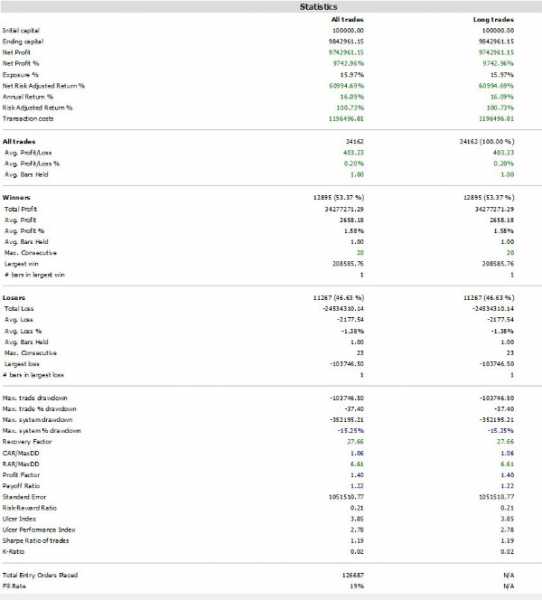

CheersParticipantlooks like I messed up the posting… sorry will try to show a better picture

ParticipantAs promised here is the statistics on my first MOC system.

Following Nick guidelines using volatility expansion. Only 2x leverage, looks promisiing but intend to let paper trade for couple of weeks more to get a better feeling.

Happy to have your feedback.

Participant

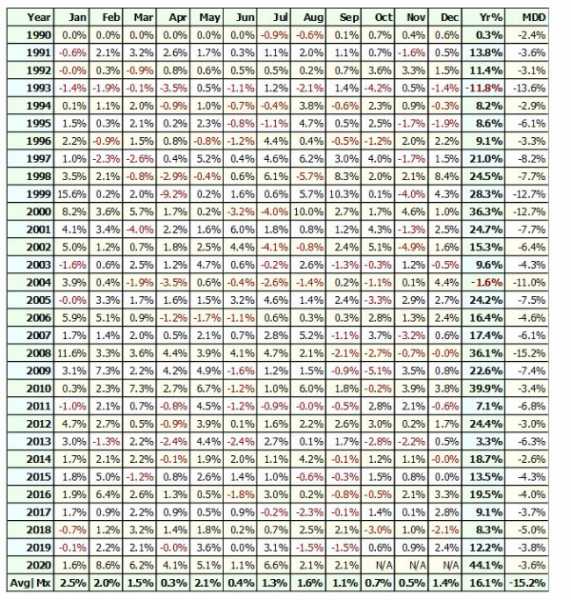

ParticipantVery interesting topic that you brough in there Terry. I am currently in the process of finalizing couple of MOC systems. I have a hard time to define optimum strech. I found that the higher the strech the lower the CAGR and the DD. But more importantly the lower strech, the lower the average profit per trade meaning a small distorsion in market conditions and you turn on the negative side. I prefer lower CAGR but higher avg profit to get some margin.

Regarding Nick’s adage, I understood it like you meaning be patient and consistent and definitely not about getting to 1000 trades the quickest way possible.Once approved by Nick I will post backtest on my journal.

ParticipantHi Seth,

great job indeed. I am not expert at all in crypto and does not have a side really, in the sense that I am not sure if these are real financial assets or not. My pragmatic view is that it could make sense to allocate couple of percent as diversification as long term view.

But the leverage – or possible leverage – numbers you are talking about sound like sure ruin to me. And you would not even need to do anything wrong.

Just my 2 cents…

cheers!ParticipantThanks a lot Seth for all the details. I am still digging but first feedback from Nick was encouraging. Will keep you posted!

-

AuthorPosts