Forum Replies Created

-

AuthorPosts

-

May 30, 2020 at 7:09 am in reply to: Incorporating an Index Volatility Based Trailing Stop with the WTT #111490

BenJeffery

MemberFound the problem. It was because I had the volume filters defaulted to on in the code. When I changed the volume settings in the backtester paramaters, the chart would be displaying the buy/sell according to the code and not the backtest I was running. Most confusing was seeing things like that example I posted. It looks like it’s picking up the 130 buy trailstop, but the backtester trailstop would have started much lower and only lifted when the index filter turned red, so it sold at the same point.

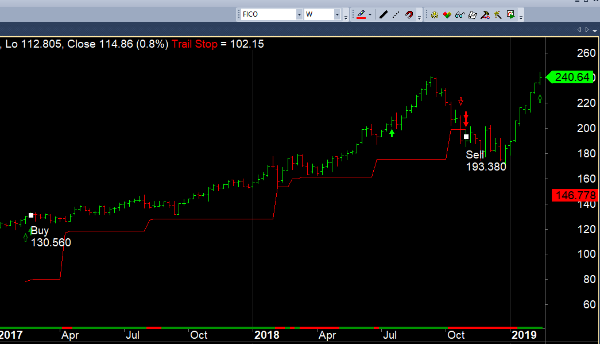

May 22, 2020 at 4:35 am in reply to: Incorporating an Index Volatility Based Trailing Stop with the WTT #111488MemberYep it’s a trade arrow. To get that arrow I right click ‘show current trade arrows’, which is where the actual trade is taken in the backtester. I can’t replicate that trade, but for that example, the backtester showed a buy at about 200 and sold at 193. If it wanted to buy at 200, it should have placed the stop much lower, rather than taking the stop from the 130 buy. A buy at 130 never occurred in the backtest, the 200 buy is the only time that symbol was traded in that backtest. Hope that kind of makes sense?

Trent try a bit earlier in this thread, I posted it as an attachment.

MemberHey Trent, I looked at something like this a while ago, they only populate the current sector. Conclusion I came to was you would need something like norgate historical sector constituents for it to work.

May 21, 2020 at 6:53 am in reply to: Incorporating an Index Volatility Based Trailing Stop with the WTT #111484MemberI’m finding when randomly checking the backtest, about 15% of the trades are appearing like this chart, with the bright green arrow as the actual trade.

It’s picking up the trailing stop from the first time LE is met – rather than when the trade is made. any idea? :unsure: May 19, 2020 at 3:07 pm in reply to: Incorporating an Index Volatility Based Trailing Stop with the WTT #111462Member

May 19, 2020 at 3:07 pm in reply to: Incorporating an Index Volatility Based Trailing Stop with the WTT #111462MemberThanks Craig.

May 18, 2020 at 5:52 am in reply to: Incorporating an Index Volatility Based Trailing Stop with the WTT #111460MemberYep Nick, I have historical constituents and dividends on.

Haven’t tested on asx yet as I only have US data, but the asx is where I’m looking to bring it in, or a rotational system.

Just wanted to compare with R3000 for coding or rule errors.settings: https://imgur.com/a/dfKcMXv

May 16, 2020 at 5:47 pm in reply to: Incorporating an Index Volatility Based Trailing Stop with the WTT #111441MemberJust concerned I might have a coding error or didn’t interpret the rules properly.

If a backtesting setting or PositionScore is why I only get 11% vs 17%, then I’m fine with that.

Here is a txt file of my rules and looping. If anyone wants to do a quick check, much appreciated.

MemberScott McNab wrote:Will give it a go..thanks Saidyou can also look at using switch().

MemberNick Radge wrote:Could be worth some investigation that a level of volatility gets too low the stretch needs to increase, or something a long those lines.Hey Nick, I had this problem too. What I do is set a minimum stretch for all trades, then take the minimum price of that and my regular stretch. A different option is to exclude any trades that don’t meet the min stretch in the entry setup rules.

May 14, 2020 at 4:25 pm in reply to: Incorporating an Index Volatility Based Trailing Stop with the WTT #111430MemberThanks Craig.

Using H > Ref(HHV(H,20),-1) gives me 11.8% with drawdown of 31%.

Is there a default PositionScore I should be using?May 13, 2020 at 5:37 pm in reply to: Incorporating an Index Volatility Based Trailing Stop with the WTT #111350MemberHey all, the WTT seems to have a cult following around here. Coded it up from the rules on thechartist website.

Tried to replicate the results below on the Russell 3000.

https://www.thechartist.com.au/product/weekend-trend-trader-amibroker-code/Could only pull a 12.7% return and 33% drawdown with dividends on.

No mention of any ranking so left PositionScore empty.

Used h==hhv(h,20), spx as the index filter and used C not L of prior bar as exit trigger, applied all price and volume filters.Can’t see where else you’d get tripped up, but could have botched it somewhere.

Is the base code available to us all or are you coding it up yourselves? -

AuthorPosts