Forum Replies Created

-

AuthorPosts

-

LeeDanello

Participantgood idea, I live in Perth Western Australia

My email is [email protected]

also on skype maurice.petterlin

ParticipantSaid Bitar wrote:Maurice Petterlin wrote:I’m trying to understand the logic here, especially this gapFilter = gapNumber == 0;Code:gap = (GapUp() OR GapDown()) AND abs(ratio) >= gapPercent;

gapNumber = Sum(gap,gapPeriod);

gapFilter = gapNumber == 0;

gapFilterOn = IIf(gapTog,1,gapFilter);line 1 gap is 1 if you have gap up or down and the gap percentage is greater than or equal to a pre specified value otherwise it is ZERO

line 2:

assume Today is Friday and the values were as following

Monday gap = 0

Tuesday gap = 1

wed gap = 0

Thursday gap = 0

so when you say gapnumber = sum (gap, duration) it will add the values of the gap (filter) to each other over this duration so in our case it will be Mon + Tues+WED +Thur ( 0+1+0+0) = 1line 3 : gapfilter it will check the answer from the previous step (gapnumber) and it will check if it is ZERO if yes it will return true otherwise false

line 4 : if gapfilter is on then check the value of gapfilter (to be true) if the filter is OFF then do not care about the value and return true

I understand line 1 and 2 but I’m lost on line 3. If gapfilter is false ie it has gaps over the lookback period, then the last line becomes

gapFilterOn = IIf(gapTog,1,0);And thats where I get lost

ParticipantI’m trying to understand the logic here, especially this gapFilter = gapNumber == 0;

Code:gap = (GapUp() OR GapDown()) AND abs(ratio) >= gapPercent;

gapNumber = Sum(gap,gapPeriod);

gapFilter = gapNumber == 0;

gapFilterOn = IIf(gapTog,1,gapFilter);ParticipantI don’t know much about rebalancing but you could check out Howard Bandy’s mean reversion book or his site. He may have an example in there

ParticipantHi Darryl,

What’s the gapFilter that you’re using?

Code:cond1 = C > longMA;

cond2 = L < bolliBot; cond3 = bolliWidth > bolliWidthMin;

cond4 = optionalFilter AND HDBFilter AND volFilter AND gapFilter;Those numbers are looking promising

ParticipantSo only good for companies that have been around for 20 years?

I always thought it was better to invest in the smaller cap stocks to get bang for your buck

ParticipantJulian Cohen wrote:This might be a little bit too much for me at the moment coding wise, but you guys might want to play around with this idea:http://blog.alphaarchitect.com/2016/05/18/return-seasonalities-are-everywhere/#gs.LozC_Oo

I wonder why these guys need to come up with complex mathematical equations to explain simple concepts?

So after trying to wade thru all the Greek symbols in the formulas, in plain English does the system say to compute the the one month ROC of all stocks in the index and buy the top 20. Next month sell those in the portfolio that are the weakest and replace with the strongest? So this a rotational system. If it’s so, it sounds similar to Clenow’s system. I’m probably completely wrong but I find it difficult reading stuff like this.

Can you provide a plain English set of rules for mathematical illiterates like myself?

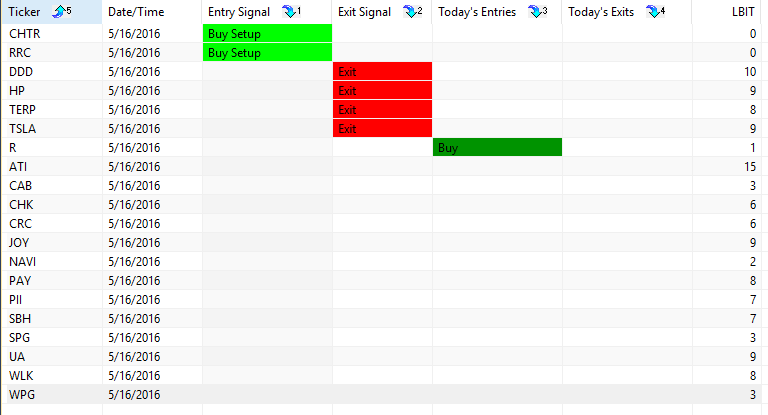

ParticipantTrent Rothall wrote:Is this about where we are at guys? Am i on track.

That’s about what I’m getting after sorting some glitches

ParticipantSaid Bitar wrote:another thing you can run this strategy on S&P500 with this condition the average volume is 5M the results will not be much different

ParticipantSaid Bitar wrote:another thing you can run this strategy on S&P500 with this condition the average volume is 5M the results will not be much differentWhat’s the main difference between the S&P and the Russell stocks?

ParticipantSaid Bitar wrote:Maurice Petterlin wrote:I definitely can’t keep up with Said. Way to quick for me. I’m on the slow burn.Oops sorry

Any how this group work I believe it has added value for all of us, I have some more ideas but I will wait for others to catch up or suggest some ideas

Don’t be sorry keep them coming. As Darryl Kerrigan from The Castle would say, “you can be the ideas man”

ParticipantI definitely can’t keep up with Said. Way to quick for me. I’m on the slow burn.

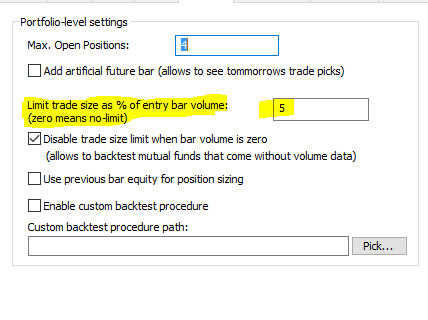

ParticipantSaid Bitar wrote:I was comparing the results of exploration between my code and the code that Maurice posted, i found that he has some stocks that are more than 100$ even though his code is specifying that it should be between 5 and 100 .for example CHTR and TSLA

Thanks I picked that up and changed the filter setting in Cond3 from VolFilt to OptFilt

So as a check, I should have looked at the Open Int field in the quote editor to check that the unadjusted price criteria was being met.

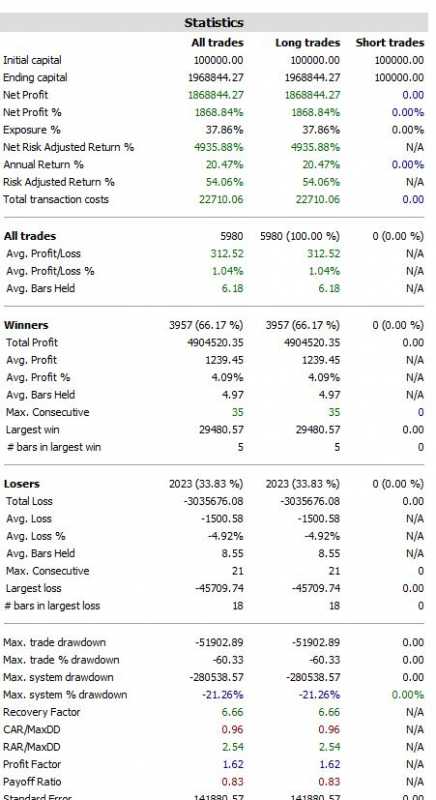

ParticipantSaid Bitar wrote:@ Trenti tested 20 positions 5% per position from 2000 till 2016 my results are a bit far from yours, the number of trades is almost half

What are you using wrt trade size limits or other settings?

ParticipantDarryl Vink wrote:My understanding is:

ParticipantDarryl Vink wrote:My understanding is:

– When you use the filter settings it provides the entire universe of symbols to run over

– When you use “IsIndexConstituent()” (from your HDBFilter) you are verifying the symbol exists in the filter list at that given dateJust setting the filter settings to Russell 1000 and Historical Constituents will include every symbol that has ever existed in the Russell 1000 over the entire period.

Hope that makes sense…

Sorry Darryl a bit confused..

Instead of the entire period, you mean that it includes the historical constituents for the dates tested. So if you exclude the HDBFilter you could be including stocks that weren’t part of the Index during your test period?

The video from http://edu.thechartist.com.au/guruTasks/7/41-section-2-module-18-full-system-coding-part-8-monte-carlo/284-historical-constituents.html shows the HDBFilter and filter = Russell 1000 Historical Constituents being selected.

ParticipantSaid Bitar wrote:Maurice Petterlin wrote:Darryl Vink wrote:Maurice Petterlin wrote:Code:Cond1 = C < LowerBand; //close below lower band Cond2 = C > MA(C,MArange);

Cond3 = VolFilt AND IndexUp AND UniverseFilter;

Cond4 = BBWidth > 5;Hi Maurice. Do your need to add something like “AND HDBFilter” into your “Cond3” ?

Correct, It did change the results

I’m wondering why the results should be different if I turn HDBFilter off and use the inbuilt filter set to Russel 1000 historical constituents?

Because you are testing on bigger universe I think this is why the results are different

Lets accept the better results then

-

AuthorPosts