Forum Replies Created

-

AuthorPosts

-

July 17, 2016 at 11:19 pm in reply to: How to Calculate use of Funds in a Portfolio of Systems #104756

LeeDanello

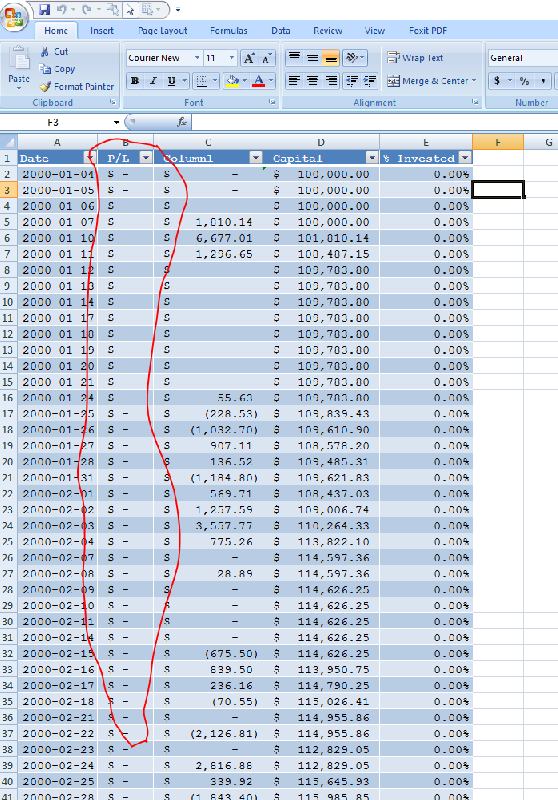

ParticipantSaid Bitar wrote:couldn’t find the afl for itbut i made the excel file

hope it will help

Nice spreadsheet but I got zeros in the P/L column

July 17, 2016 at 8:57 am in reply to: How to Calculate use of Funds in a Portfolio of Systems #104746ParticipantJulian Cohen wrote:So if I run a backtest can I put the trades straight into Share Trade Tracker? I haven’t really used it yet

July 17, 2016 at 8:57 am in reply to: How to Calculate use of Funds in a Portfolio of Systems #104746ParticipantJulian Cohen wrote:So if I run a backtest can I put the trades straight into Share Trade Tracker? I haven’t really used it yetIt’s not for backtesting. It’s a trade management spreadsheet. It records your trade entries and exits and it also keeps track of your dividends for however many stock trading portfolios you have. You can do portfolio summaries for EOY tax reporting. Nick has done a webinar and posted it on The Chartist website.

ParticipantNick spoke about max wait days in another thread which measures the time it takes to make new equity highs from the draw down.

https://edu.thechartist.com.au/Forum/performance-metrics/125-how-to-calculate-max-wait-days.html

Personally and at this stage I’m looking for high win rates>65%, Low drawdown <15% Profit factor >1.5, Ave Win/ Ave loss ~ 1.0

ParticipantBuy on the open, sell at the close? Excuse my ignorance but is this as simple as it sounds?

I’m only a beginner systems trader! Is this to enable the system to use the maximum leverage in IB?ParticipantFrom your back testing what is the average number of trades taken per day

ParticipantI thought something was up. I did another run the day after and it took about an hr and a half. I’m not sure what was up with the computer.

I should do another run. I just went into Amibroker and cranked up the following settings. You learn something new every day. ParticipantJulian Cohen wrote:Ah it’s just a short run MCS…sorry thought it was from 2000 !! Was thinking you might have had a brain fart but in fact it was me

ParticipantJulian Cohen wrote:Ah it’s just a short run MCS…sorry thought it was from 2000 !! Was thinking you might have had a brain fart but in fact it was me")

Its a short and long strategy!

ParticipantMaybe this will help

http://www.amibroker.org/userkb/2007/06/26/data-holes-in-real-time-trading/

ParticipantOK.

ParticipantCraig Fisher wrote:Yes, I’ve only been alerted to the Line Comment recently so I gather it’s quite new.Re MCS – depends on what you want to achieve.

The example of Variant is not full code – just an example to use the identifier ‘Variant’ instead of RandPercent(MCRP) as in the course notes – thought it might be easier.

An easier way to get the monthly data for an index when doing correlation analysis would be to use something like:-

MonthReturn = ROC(C,1);

Filter = MonthReturn;

AddColumn(MonthReturn,”Month ROC”);Once you have run the test on your system, replace the filter with the above, select the index on a chart, select ‘Current’ in the analyser filter, select Monthly in settings and run Explore. Then the monthly returns can be copied straight into excel.

So if you want to use the variant code on it’s own, MCP should be MCRP in the following block.

Code://MCS code part 2

if (MCRP)

LE = LE && Random()*100 >= MCRP;If you wanted to use it in combination with trade skipping, the code given below is OK

Code://MCS code part 2

if (MCP)

LE = LE && Random()*100 >= MCP;ParticipantThanks Craig,

Is the “engage / disengage blocks of code, highlight block > right click > Line Comment” a new feature of Amibroker? I haven’t noticed it before.

Just wondering whether the signal and data variance code should be run with the Monte Carlo code.

If you wanted to modify the closing price wouldn’t the code be Close = Close * Variant.

ParticipantJulian Cohen wrote:Sorry Paul, I only just saw your post.I changed my settings on Fusion to allow 4 threads and 8 GB of RAM to the virtual machine. As long as I don’t try and run anything like Photoshop and leave the MacBook Pro alone to run the MCS, I can get 1000 runs on the Russell 1000 from 2010-2016 on a 25% trade skipping done in an hour and a half. I’m quite happy with that.

I don’t think it’s worth my while to get a Windows machine just to run Monte Carlos faster, so I’ll keep going as is for the moment.

I just did a thousand runs on the Russell 1000 from Jan 2000 to June 2016 in just over 5 hrs using a Windows 64 bit machine with a SSD. Before I started the test I thought an hr and half might do it.

ParticipantPeter Hammersly was saying in his reviews that it might go down to about 4400. All we know is that volatility will be high which is good for these type of systems.

ParticipantIs this a sucker rally that we’re experiencing at the moment? Do you think we’ll see lower prices in the next month. Seems like at the moment the market doesn’t care much about the Brits?

ParticipantDarryl has brought up the idea of using include files in his code. I prefer this method for blocks of repeatable code rather than using snippets. Everything stays nice and compact. Where you need to modify code like looping structures, then obviously snippets need to be used.

-

AuthorPosts