Forums › Trading System Mentor Course Community › Progress Journal › Trents Weekly Journal

- This topic is empty.

-

AuthorPosts

-

March 15, 2016 at 1:18 am #102648

TrentRothall

ParticipantWhen combining two separate mean reversion systems I was hoping to increase trade frequency which in turn should equal more profits. The two systems are fairly similar so there are a lot of overlapping signals when they are run separately. My thinking was that if I could take the signals that triggered by system 1 then I could also take additional signals that triggered in system 2. While the number of trades increase by about 25% when the systems were combined the annual return only increased by about 2%.

So I went back and tested all the signals from system 2 that did NOT meet the entry criteria from system 1. Basically it is all the additional trades that show up in the back test when the two systems are tested together.

As I thought might be the case these additional trades are not as successful as trades that meet the criteria from system 1 AND system 2.

Winning percentage on these additional trades are about 5% lower than system 1

expectancy per trade is 0.92% compared to 1.42%

MAR is 0.57 compared to 2So although the trades add a bit to the overall return of the system without adding to much to the maximum drawdown, and you might feel a bit better because you are placing more trades I’m not really sure if it is worth it in this instance.

It might work better if you are combining systems that don’t have as many overlapping signals, you might be able to tighten the restrictions on both systems so that you are only taking quality trades from both

March 15, 2016 at 5:06 am #102649Nick Radge

KeymasterSome great findings there Trent. Well done.

March 15, 2016 at 7:03 am #102650ParticipantThanks Nick.

Tuesday 15.3.16

3 Entries

0 Exits1 Pending Exit

15 Pending EntriesWill be 4 open positions

A bit more action today which is good, would still like a big lump of entries to ensure the explorations track the trades properly.

ARF bucked the trend today with a nice bounce to trigger a exit tomorrow morning. Nice and quick in and out hopefully

March 16, 2016 at 7:25 am #102651Participant

March 16, 2016 at 7:25 am #102651ParticipantWednesday 16.3.16

1 Exit

0 Entries4 Open positions

16 PendingMarch 17, 2016 at 6:44 am #102652ParticipantThursday 17.3.16

1 Entry

1 Exit signal

Will be 4 open positions4 Pending

March 18, 2016 at 7:17 am #102653ParticipantFriday 18.3.16

0 Entries

1 Exit2 Pending exits

6 Pending entrieswill be 2 open positions

System Weekly Wrap – to date

8 closed trades

6 wins

2 lossesA few more entries this week with a few pending exits. Trading MR system I expect fairly quiet times with the lower exposure. Hopefully won’t be far off trading it live.

Got out just in time here on HFR – I had a feeling it was going to pop one way or another

March 21, 2016 at 7:30 am #102654Participant

March 21, 2016 at 7:30 am #102654ParticipantMon 21.3.16

2 Exits

0 Entries3 Pending entries

2 Open positions

Trying to get the IB DDE to work through TWS, keep getting an error message but i haven’t spent too long on it yet.

March 21, 2016 at 9:07 am #102655ParticipantWhen I was combining 2 MR systems together I noticed that when a trade triggers that met the conditions from both system 1 and system 2 those trades tend to be of a better quality with a higher win rate and profit per trade. But when ran like this the lower trade frequency hurt returns

The 2nd system that I added to my main system doesn’t have as high CAR as my main system, one thing that appeals to me out of it is that it seems to be a bit more consistent in the leaner years. I.e in 2008 it returned around 15% where my other system was around 5%.

Because my system doesn’t use an index filter I thought I might be able to use my main system when a normal index filter is up but once the index turns down then take the higher quality signals (signals from both system 1 and system 2)

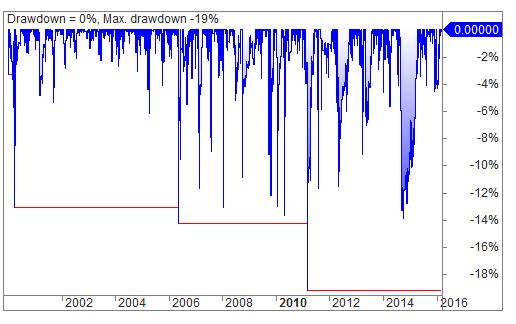

This is my main system run only when the index is DOWN

This is taking only the quality signals that come from the combined system 1 and 2 when the index is down.

This does 30% less trades

The ave trade p/l per trade is 2.5% compared to 1.67%

CAR is also higher just March 21, 2016 at 9:20 am #102656Participant

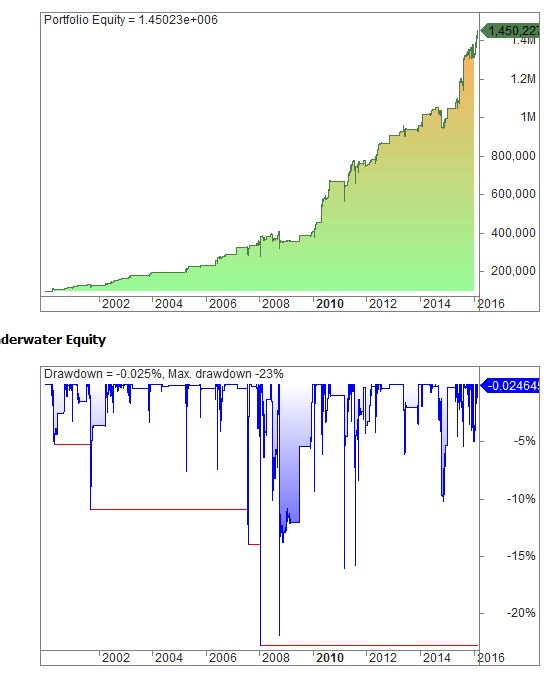

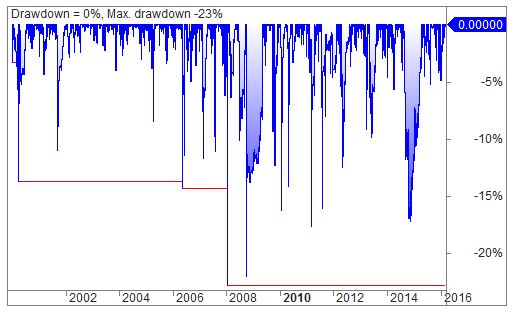

March 21, 2016 at 9:20 am #102656ParticipantThis is my original system on XAO – no index filter

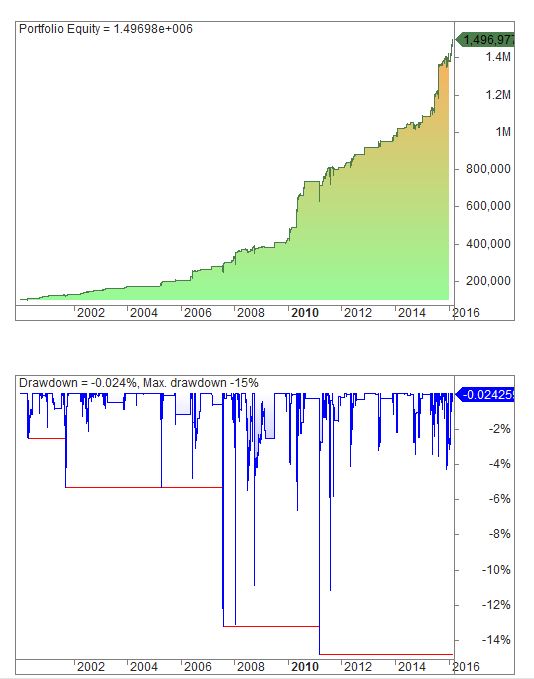

This is the ‘Hybrid’ syystem only taking quality signals when the index is down

Looks better so far returns are the same exposure drops – about 12% less trades

March 21, 2016 at 12:27 pm #103390SaidBitar

MemberHere are my observations from doing the same exercise

If you want higher exposure try changing the exit to a longer one such as

Two higher closes

Cross with moving average

Oversold level on short term oscillatorIf you want to increase trade frequency use

Fast exits such as one higher close or the close of the same day

Or decrease the stretchAll the above are doable on the system that you like

What I noticed that higher frequency is good at least for me since it is returning higher profits with a bit deeper drawdown but my aim is to make profits

So I started putting systems with each other and merge them in one system

The initial plan was to merge four systems and control the priority by stretch length so higher priority will be with shorter stretch and so onFour systems together were not doing what I expected from them since of overlapping signals and some early entries of one system that didn’t allow other system to play their role. Still they are profitable but I was expecting better results so I decreased from 4 to 3 and I found out that the three together are having same performance as the one that went out.

At the moment I am paper trading this combination and hopefully in the future if this system will generate enough profits I will use the profits as trading capital for the remaining system.

No idea if it is good idea or not

So what I want to say is to check which direction is better for your systems is it higher frequency or higher exposure

March 22, 2016 at 9:02 am #103391ParticipantThanks for that Said will keep those points in mind, and let you know how i go. At the moment i am finding increasing frequency is not necessarily as profitable if the extra trades are half as profitable as the main ones.

Tues 22.3.16

no entries or exits

1 Exit signal

4 Buy signals1 Open position

March 23, 2016 at 8:40 am #103414ParticipantWednesday 23.3.16

1 Exit

No entries10 Pending entries

1 Open

March 26, 2016 at 1:24 am #102657ParticipantThursday 24.3.16

0 Exit

2 Entries – should have been 3 but i made a mistake and the order cancelled. Hopefully the API will not allow these errors17 Pending orders

1 Exit signalWeekly Wrap

11 Closed trades

8 Wins

3 Losses3 Open Positions

March 29, 2016 at 8:01 am #103456ParticipantTues 29.3.16

1 Exit

3 Entries – 1 partial fill in one though24 Pending Entries

5 Open positionsHaving the API up and running defiantly makes things easier!

March 30, 2016 at 7:30 am #102658ParticipantWednesday 30.3.16

2 Entries

12 Pending orders

7 Open posiions -

AuthorPosts

- You must be logged in to reply to this topic.