Home › Forums › Trading System Mentor Course Community › Progress Journal › Trents Weekly Journal

- This topic is empty.

-

AuthorPosts

-

December 1, 2017 at 6:33 am #108078

TrentRothall

ParticipantDec results

MR1 = 7.75%

MR2 = 2.87%

Total = 5.42%

December 1, 2017 at 9:36 am #108117JulianCohen

ParticipantNoice!!

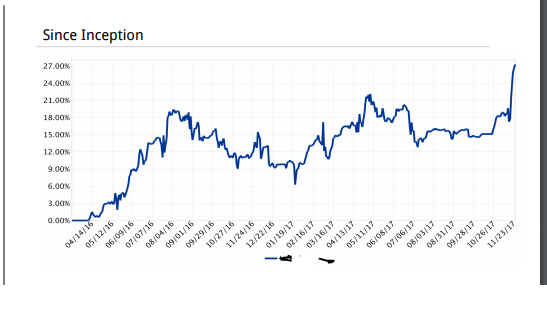

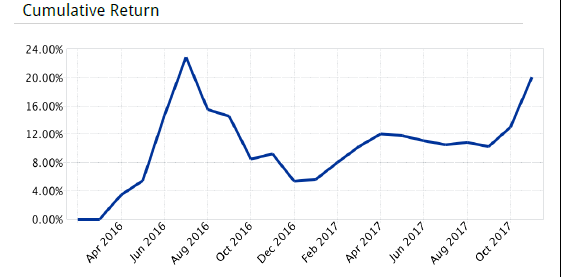

December 2, 2017 at 2:02 am #108121ParticipantPretty confused with IB reports, here is my equity curve from the same account from two different reports.

Actual return on capital in this account is around 27% since inception, after rebalancing funds once i brought the other account into play. So i guess i’ll take the better looking curve??

December 13, 2017 at 1:35 am #108129Participant

December 13, 2017 at 1:35 am #108129ParticipantHas anyone thought of running or does anyone run a small aggressive MR account? My thinking was a almost all in type scenario where you have only 2 or 3 positions depending on account size. For example on the asx you could have a 15k account with only 2 positions, then once the account grows another $7500 add another position (anything under $7500 commissions start to hurt). Obviously it would be volatile but i ran some MCS on only 2 positions and it’s nothing over the top when you consider the $$ as part of a larger portfolio.

December 13, 2017 at 2:19 am #108189Nick Radge

KeymasterSounds viable. Selection bias?

December 13, 2017 at 3:01 am #108191ParticipantYeah there would be big selection bias but i would trade one of the systems i’m trading now and at 20 positions SB is minimal. So my thinking is that even though there is a lot of possible entries, it shouldn’t really matter which ones get filled..

December 13, 2017 at 7:47 am #108192ScottMcNab

ParticipantAt the risk of sounding like a broken record….for such a system could maybe try an entry when open gaps below your buy limit….selection bias would not be as significant as the stock selected (on US when all open together) would be random….would also reduce the number of potential entries further reducing impact of selection bias

December 13, 2017 at 8:33 pm #108196ParticipantScott McNab wrote:At the risk of sounding like a broken record….for such a system could maybe try an entry when open gaps below your buy limit….selection bias would not be as significant as the stock selected (on US when all open together) would be random….would also reduce the number of potential entries further reducing impact of selection biasI have this on my list of things to test over Xmas Scott

December 13, 2017 at 10:03 pm #108197SaidBitar

MemberThe main issue with the ASX is when your limit price is the low of the day most probably you will not get filled so it is better when backtesting to make sure that the L < LimitPrice + few cents Regarding SB as Scott mentioned entry only on the open will help or extended stretch on smaller universe One point that confused me if you will run 2 positions each 7500 and you will add third with the profit of 7500 this means with time it will be less volatile

December 14, 2017 at 12:20 am #108198ParticipantAgree with the L < limit Said. My example of 7500 was just a way to have exposure to a MR system if you didn't have enough for a full system, if i was going to do it i'd probably just keep 2 positions until they got too large to get good fills, maybe 15k?? Then start to add another position. With the Open < BuyLimit i think you wouldn't get enough trades, well not with my current system anyway on the asx. It rarely happens to me

December 14, 2017 at 9:13 am #108190ParticipantTrent Rothall wrote:Has anyone thought of running or does anyone run a small aggressive MR account? My thinking was a almost all in type scenario where you have only 2 or 3 positions depending on account size. For example on the asx you could have a 15k account with only 2 positions, then once the account grows another $7500 add another position (anything under $7500 commissions start to hurt). Obviously it would be volatile but i ran some MCS on only 2 positions and it’s nothing over the top when you consider the $$ as part of a larger portfolio.Trent, I have been doing something similar with a MRV system on the ETF universe…2 positions at 50%….have found can simply buy the etf on the next open instead of a buylimit order requiring a further drop…which in turns allows use of positionscore and elimination of selection bias…use universe of ETFs with volume filter (eg MA(20)>400000 to weed out the ones with poor liquidity)

December 15, 2017 at 12:04 am #108204ParticipantOh that makes sense scott, i’ll have to look into that one! cheers.

How many ETFs in your watchlist out of interest?

December 15, 2017 at 1:51 am #108209ParticipantAt this stage I am just using all in group 4: ETF which is 2756…..but most dont meet volume requirements (using MA(Volume,25) > 500k to 1mill at the moment..).just want liquid ones without cherry picking etf’s …ideally want as much diversity as possible away from stocks…might be worth trying without stock etf…early days but encouraging

December 19, 2017 at 3:40 am #108210ParticipantFor those of you who are using risk parity position sizing in your momentum systems, is it current market conditions or current positions that will limit the max number of positions that can be held?

If you had max positions set to say 10 in high volatiity conditions you might only use 75% of funds wouldn’t you, because each position is small? but if volatility decreases then each position becomes larger.

December 19, 2017 at 5:07 am #108229KeymasterYou wouldn’t have a max number of positions. In your example you’d continue to add positions until 100% is allocated.

-

AuthorPosts

- You must be logged in to reply to this topic.