Forums › Trading System Mentor Course Community › Trading System Brainstorming › Trading system broken?

- This topic is empty.

-

AuthorPosts

-

January 13, 2020 at 12:57 pm #110792

LEONARDZIR

ParticipantDaniel,

The other explanation is that mean reversion in stocks in the US has been losing its edge for the past several years and your testing reflects that.

I suppose it is possible to trade mean reversion if you develop a system that uses variables nobody else has thought of.

It says something when Trent’s highly sucessful mean reversion in the ASX falls apart in the US.January 13, 2020 at 4:41 pm #110793DanielBaeumler

MemberGreat feedback. Thank’s a lot to all of you.

Back in 2018, Craig reviewed the code and Nick also looked at the system and liked it.

I also played with the parameters and the equity/underwater curve keep more or less its shape. No spikes etc.@Len, I believe you are spot on. The market simply has changed. I also doubt that it’s good enough these days to develop a system using a set of standard indicators such as RSI and expect it to make money. Especially not in popular markets like NDX/SPX. Like everywhere else, our ‘business’ has become more competitive.

I will sit down again and revisit my approach. Developing a truly unique system nobody else thought is for sure a challenge…

January 13, 2020 at 8:50 pm #110794Nick Radge

KeymasterTwo of my mean reversion systems made 19.4% and 20.5% respectively last year. Neither use conventional indicators…

January 13, 2020 at 10:14 pm #110795ParticipantNick,

Great results. Said as well.

I wonder if we could poll all the members in the forum who used mean reversion in the US last year to find out how many people were profitable and what percent did they achieved?January 13, 2020 at 11:59 pm #110777ScottMcNab

ParticipantHard to know if market changed…certainly possible crowded space as more people look into MRV systems…or HFT may have changed landscape…etc etc

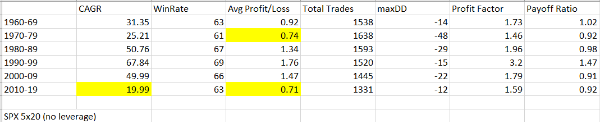

I tested my mrv on spx (using 5 positions at 20%)…last decade the worst but not all that different to the 70’s….in another decade we will know more..:unsure:

January 15, 2020 at 3:06 am #110796

January 15, 2020 at 3:06 am #110796Anonymous

InactiveI think like any other indicator/method things always evolve and limits/values used on such indicators will always need to evolve along with them.

A moving average that was effective at 180 days twenty years ago but now needs to be more like 120 days is no different to a 20 day RSI at 30/70 limits 20 years ago now needing to be at 5 days 15/85 in more recent years (or vice versa, of course I’m just plucking examples from the air).

Just because some settings that worked 20 years ago are no longer as effective these days doesn’t necessarily mean the method/style is broken, they just need some re-tuning for today’s conditions.

I reckon the human psyche in dealing with trading in the market has always probably been of the mindset of “Enter via the stairs, leave via the elevator” but these days it is probably more like “Enter via the elevator, leave via the firepole”. With pc/algo driving so much, it is no wonder the speed at which the market operates today is quite different to the way it operated even just 10 or 15 years ago. The same mathematical methods/theories can likely be used, just need to ensure the methods are tuned to react to today’s (and hopefully tomorrow’s) needs, not necessarily the needs that were in play 15 years ago or more.

January 15, 2020 at 5:11 pm #110778InactiveDisclaimer: I am new around here and I don’t have much experience.

However, I do not like RSI. It is too popular. Everyone and their brother knows about it and can plot it on tradingview with no code experience and can trade it (and automate it, too). When I see people (may be showing my green thumb here) on bitcoin forums/chats influencing malleable minds with fancy charts with RSI and STOCHRSI plastered all over them, I commit to memory that said instrument is overused.

Before I started this course I had made a note to go back and listen to Cesar Avarez’s episodes again on BST once I had some code experience. Check them out and see if you like anything that he says…. and then let me know so that I can make further note of it!

http://bettersystemtrader.com/127-building-mean-reversion-strategies-with-cesar-alvarez-part-1/

Cheers

January 15, 2020 at 10:56 pm #110800KeymasterHere’s a link to another mean reversion vendor that trades very similar to Larry Connors…note the equity curve.

January 16, 2020 at 12:25 am #110801InactiveCertainly stinks after Q1 2018 that equity curve Nick. Looks like the same pain Daniel is wearing with his system.

@Seth: Absolutely, what works for you is what you need to roll with. Not trying to tell anyone anything different. And don’t worry about disclaimers of knowledge/experience/skill. We are all new, all learners and all infants in this trading game around here. Even Nick who has been in the business for over 30 years will tell you he is still learning and still often gets a smack in the face that teaches him something about this game we are in.

Agreed that many know about RSI. However by that token, many people also know how to calculate a moving average, have known this for a long time, yet this is something still proving the test of time. It is not as if it is a secret of some sort that is now finding its way into the market in general. I reckon like anything it takes a mix of things, applied in your way, to give you the edge you are happy to trade with.

January 28, 2020 at 12:43 am #110802TerryDunne

ParticipantHi Guys,

Been away on holiday – no electronics – so late to this discussion.

I share Daniel’s concerns (although I haven’t traded only back tested). My version of MRV has the following rules:

1. Russello 3000 (with all of the historical components etc) and average liquidity > $1m;

2. RSI(2) < 20;

3. 3 consecutive days of new lows;

4. Intra-day trigger being 1 ATR lower than yesterday’s low;

5. Sell at the close on the following day.I back tested from 1995 and broke my testing into 3 sections. While I don’t have my results in front of me, they were roughly:

1995-2004

Win % 60

Win/Loss ratio 1.2

CAGR 30+%(!!!)

Max drawdown <15%2005-2015

Win % 55

Win/Loss ratio 1.1

CAGR 20%;

Max drawdown 20%2016-2019

losses (albeit small) each yearNow I didn’t for a moment expect to generate returns in the 30% region. However, the system doesn’t appear (to me?) to be curve fitted and the drop off in performance has been ‘spectacular’. Imagine you started trading this system sometime around 2010. Are you still trading the system today? And if you are, what would cause you to stop?

As you can imagine, I’m reluctant to start trading this system, partly because of broader psychological issues, but really the results suggest at least the possibility that the market has ‘changed’ in some way…one thought I had was pricing and execution through brokers may have made it difficult to cash in on the MRV opportunities back in the 90s/00s?

I was encouraged by the results Nick posted for his MRV systems – it’s nice to know that mean reversion is still ‘working’. So is using short RSI the problem? That seems to conflict with the idea that authors often have that it won’t harm their system to disclose their rules?

It would be great to hear people’s experiences/war stories…

Regards,

Terry

January 28, 2020 at 12:51 am #110834KeymasterDid I see that system Terry? I have none in my files for you?

I have to say this again, but the RSI(2) is an extremely well known concept as are all Larry Connors concepts. The more widely known the more likely they’ll be arbitraged out of the market.

January 28, 2020 at 1:17 am #110835MichaelRodwell

MemberHi Nick,

On your recent presentation you shared the HFT results and as you commented 2016 to 2018 was pretty ordinary.

2016 (3.05%)

2017 (-0.68%)and 2018 was one to forget (-21.31% October blood bath)

The above doesn’t seem to different to what Daniel has experienced.

What gave you the confidence to keep trading it after such a drop off in performance.

I notice there was one other year (2004) with similar stats too but otherwise very consistently profitable.

January 28, 2020 at 3:14 pm #110836InactiveThanks for the discussion guys – very interesting and helpful.

Anecdotally I agree that, post-2016 it seems that the market structure changed or the systematic trading space became more challenging – specifically focusing on short-term mean reversion and MOC systems. In many of my system tests, performance is strong up until 2016 and then becomes weaker/more erratic.

Regarding the use of data back to 1960, I question if any data pre-2000 is really relevant. The market structure, fees, algo participation in the market was so different pre-2000, or even pre-2008. Personally, I don’t think testing from the 1990 is representative of today’s market.

Scott – thank you for sharing your thoughts regarding testing on different markets. How or what data source do you use for these other markets that you list. I have struggled to find anything even close to Norgate. I would love to look at other markets but haven’t felt comfortable without historical constituents.

January 28, 2020 at 9:08 pm #110846ParticipantHi Dustin..I have a metastock subscription too..has survivorship bias as it is current constituents…i was using it initally to trade Hong Kong and Tokyo but then started using it for backtesting in the desire to find an “unseen” data set…not perfect but is still OHLC and volume…would not use it for system design but just an extra hurdle system has to clear to go live

The pre 1990 data also obviously has issues …but if a system works essentially the same on the metastock data and the pre 1990 data then I see that as a positive….raised here to illustrate how I determine if an underperforming system should be turned off…just the way I answer that question…keen to find a more objective way but no luck yetJanuary 28, 2020 at 10:16 pm #110847KeymasterQuote:On your recent presentation you shared the HFT results and as you commented 2016 to 2018 was pretty ordinary.Well, I’m not quite sure when this theory of a down year means the system is broken?

2018 I can write off as a black swan.

2016 and 2017 were extremely low volatility years. As pointed out, my system is volatility based, so low vola doesn’t help.

-

AuthorPosts

- You must be logged in to reply to this topic.