Home › Forums › Trading System Mentor Course Community › Progress Journal › Scott’s Journal

- This topic is empty.

-

AuthorPosts

-

May 26, 2016 at 8:31 pm #103063

ScottMcNab

Participant77 buy limit orders placed…..4 entries overnight….

May 27, 2016 at 11:10 pm #103064ParticipantOnly 1 entry TEX overnight….gapped down on open and then rallied 4% during the day

1st week down with new MRV system

13 trades…9 winners and 4 losers

so far so good

June 5, 2016 at 10:14 am #103065ParticipantLooking over paper trading for week2

34 entries

14 trades completed – 8 winners and 6 losers

20 trades remain open…13 in the black and 7 in the red….hope its a strong open on Monday3 trades taken by Amibroker not filled in paper acct; 2 of them (HBAN and VOYA) hit the lows before 10am open and were above buy limit at 10am) but the third I’m not sure about…..BRK.B had a buy limit order on 3Jun for 140.37 and was sitting at 140.14 at 10.30am and 140.16 at 11.30am but did not trigger…

in total 34 buy signals of which 3 occurred in Amibroker but not in paper….backtest works fine ok with 25% trade skip so should be ok with 1 in 10

June 5, 2016 at 10:44 pm #103066Nick Radge

KeymasterBRK.B will never get a fill. I think you need to engage the actual exchange designation for it to be placed.

June 6, 2016 at 12:31 am #103067Participantok..thanks Nick…I will cross it off the list

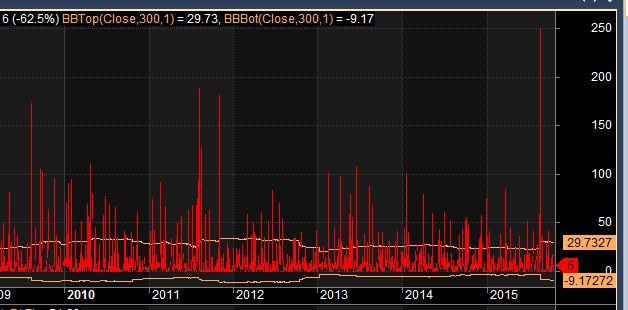

June 15, 2016 at 11:54 pm #103068Participantmade some changes to position size and margin….now 30 positions using chart of Darryl’s based on the following (upper BB 1 SD from 300 MA)…any comments/feedback received with thanks

June 16, 2016 at 12:25 am #103069Participant

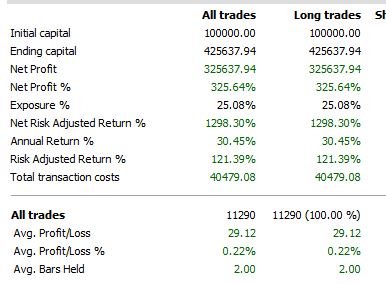

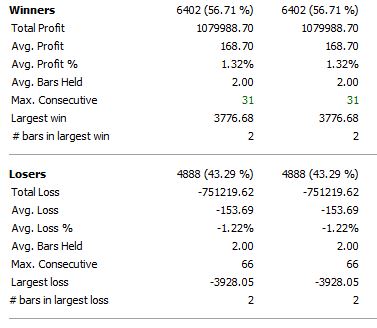

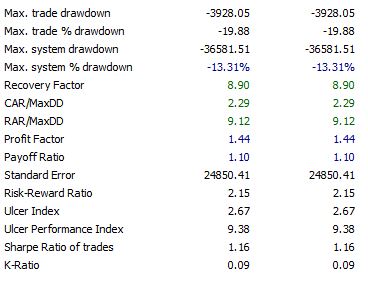

June 16, 2016 at 12:25 am #103069Participantother stats… single run 2011 to 2016

June 17, 2016 at 5:40 am #104365

June 17, 2016 at 5:40 am #104365Anonymous

InactiveScott McNab wrote:other stats… single run 2011 to 2016Hi Scott… just wondering what position size and max positions your using?

June 17, 2016 at 5:43 am #103070Participant30 positions at 6%

made some changes to tighten entry criteria and reduce selection bias

June 17, 2016 at 6:53 am #104371InactiveScott McNab wrote:30 positions at 6%

June 17, 2016 at 6:53 am #104371InactiveScott McNab wrote:30 positions at 6%made some changes to tighten entry criteria and reduce selection bias

its an interesting exercise trying to find the best combination of margin, position size and max positions. after many tries and fails at consistency i went back to 20 positions with 10 % equity with my system due to consistent results. im still not sure what is best…

June 17, 2016 at 7:57 am #103071KeymasterQuote:im still not sure what is best…Simple works best

") June 17, 2016 at 9:04 am #104374ParticipantDarryl Vink wrote:Scott McNab wrote:30 positions at 6%

June 17, 2016 at 9:04 am #104374ParticipantDarryl Vink wrote:Scott McNab wrote:30 positions at 6%made some changes to tighten entry criteria and reduce selection bias

its an interesting exercise trying to find the best combination of margin, position size and max positions. after many tries and fails at consistency i went back to 20 positions with 10 % equity with my system due to consistent results. im still not sure what is best…

I made the decision to use 30 positions based on the code/graph you were kind enough to post. It was a bit of an arbitrary decision but I wanted to limit the number of days where the system couldn’t take all the available trades to 3 or 4 a month. The systems’s metrics are better with a lower number of positions but the message I took away from the last group call was that we each had to decide whether to trade for CAR or comfort…so I went for 30 positions. It may be diluting CAR but so be it. The results I posted were for 2011-2016. I used this as this was the worst period for the system and I wanted to base any changes around this time frame in case this is a reflection of changes to market structure etc (ie changes that are likely to persist into the future) rather than just an anomaly . I too am constantly trying different combos. If I find one I like, i then try it on NDX (looking at win/loss ratio,payoff ratio and profit factor) The addtocomposite has kept me experimenting for hours by adding a new element to the mix.

June 17, 2016 at 9:16 am #104375LeeDanello

ParticipantWhy not use the MAR ratio and pick the highest one

June 17, 2016 at 9:42 am #103072ParticipantIt was my concern regarding selection bias. I was finding that the systems with the best metrics were not taking a significant number of trades.

June 17, 2016 at 9:46 am #104376TrentRothall

ParticipantCorrect me if i am wrong but doesn’t tht chart only shows trades on that DAY so the graph might show 5 trades but you may already have 25 open. So if you are thinking you dont want to miss trades it might be different if when you start trading it?

Is that right?

When i did this to calculate total possible trades was exit on the next open after a buy, this way you wouldn’t have a full portfolo. But i guess if you are testing with 500 max positions it might be ok

-

AuthorPosts

- You must be logged in to reply to this topic.