Home › Forums › Trading System Mentor Course Community › Progress Journal › Scott’s Journal

- This topic is empty.

-

AuthorPosts

-

November 1, 2018 at 10:16 am #103199

ScottMcNab

ParticipantOCT 2018

Rotation

NDX -2.3

RUI -17.6 (switched itself off for Nov)

XTO -4.1MRV

RUI -6.7

RUT -9.1

XAO -6.4

TSE -4.3Increased allocation to MRV systems 300% on 23 Oct

Suspended TSE due to issues with 100 lot causing significant divergence from backtest

Since increased allocation to XAO have noticed some slippage (already) that was not there previously which will require monitoring

Goal of allocating 40% to markets outside of US (no sound premise other than made me feel more comfortable investing more capital) looking less achievable for the momentDecember 1, 2018 at 8:17 pm #103200ParticipantNOV 2018

Rotation

NDX 0.7

XTO -10.4 (thought Oct was too good to be true)

RUI offMRV

RUI 3.5

RUT 1.1

XAO -1.5January 1, 2019 at 2:16 pm #103201ParticipantDEC 2018

Rotation (%)

NDX -11.2

RUI -6.3

XTO 4.9MRV (%)

RUI -1.1

RUT -3.4

XAO -0.8Happy New Year

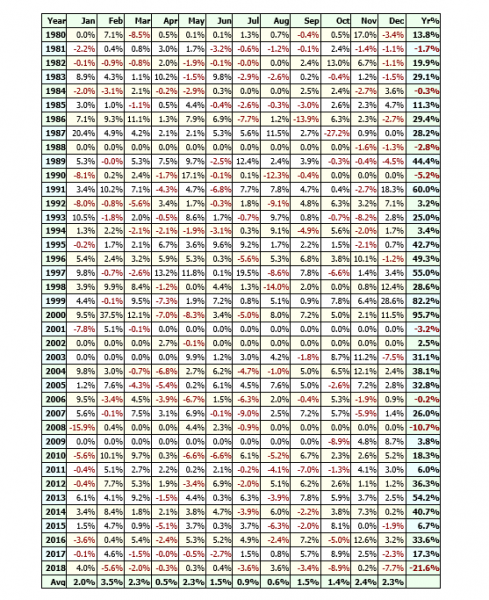

January 15, 2019 at 9:32 am #103202ParticipantWas interested to see how badly 2018 sucked for my US rotation systems so changed it from RUI the SPX and tested back to 1980

Not the worst DD (1987 still ahead)….

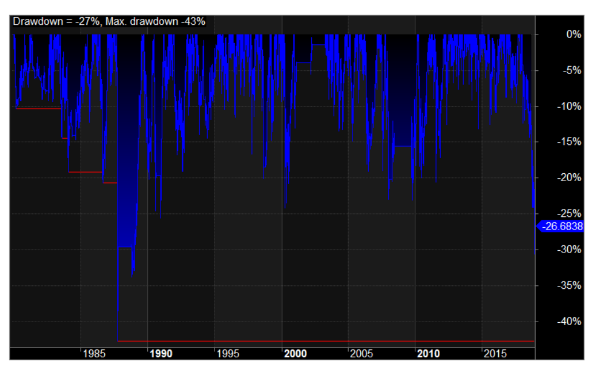

its tempting to try and rationalize that 2019 will bounce back …lucky don’t have to try and guess ..just place the tradesJanuary 15, 2019 at 10:01 am #103203Participantdrawdowns

January 15, 2019 at 8:56 pm #109537

January 15, 2019 at 8:56 pm #109537Nick Radge

KeymasterA good article written by Brent in this group. His system avoided much of the damage of Q4.

https://theintelligentallocator.com/articles/robusticity-what-it-is-and-why-its-important

January 16, 2019 at 2:53 am #109541TimothyStrickland

MemberGreat article

January 16, 2019 at 5:49 am #109542MichaelRodwell

MemberNick,

Does your comment – “His system avoided much of the damage of Q4.” – imply the approach discussed in the article would be the reason the system has avoided the Q4 damage?

Thanks

January 17, 2019 at 9:37 am #103204ParticipantArticle got me thinking a bit more about robustness…how a rotational momo system without the highest CAR may be better on basis of robustness

I tried optimizing a couple of different systems….not by optimizing a setup condition or filter but using the trading day of the month(0-20)…not for the reasons Larry Williams does but more to get an idea of how dependent the results were to my choice of using the first day of the month by default….found for some systems the variation (eg car/maxdd) was minimal and in others it was significant.

January 17, 2019 at 8:59 pm #109545KeymasterGoogle Swarm Theory. That’s basically what all the big funds do these days. Not sure how much we can do though.

January 17, 2019 at 10:40 pm #109546ParticipantNick, do you think it is too much of a stretch or just plain wrong to think that the system that has the least variation in stats over the 20 different trading days may be more robust ? I was thinking of using it as a means of differentiating between systems which are otherwise pretty similar.

To clarify my thoughts, I am wondering if I have inadvertently selected a system that looks better than it is going to be going forward

eg

System A has a 22% cagr and maxDD if traded on 1st day of month but the average over all the days is 16% with 28% maxDD

System B has 16% cagr and 26% maxDD when use the first day of the month but the average over the entire month may be 19%/26%January 18, 2019 at 5:55 am #109547KeymasterNot sure how you’d consider trading it ‘on average’. That’s leading to optimisation.

First day of the month makes sense. It’s logical. Middle of the month makes sense. A combination of the two makes sense.

If there is a specific day that has a specific reason for being more effective then its work investigating, but chances are its a random anomaly.

January 18, 2019 at 7:05 am #109548ParticipantThanks Nick. I might be barking up the wrong tree again. I was wondering if the “average” and the “spread around the average” would be a measure of robustness that could be used in the process of system stress testing and selection. I am not thinking of trying to trade an average of the days. Of the two systems I trade, for one of them the first day of the month is consistently the best result over all the time frames and for the other the first day of the month comes in about middle of the range over all those days…made me feel better about the second system and a bit concerned that I have cherry picked the first one.

Enough time spent…time to move on

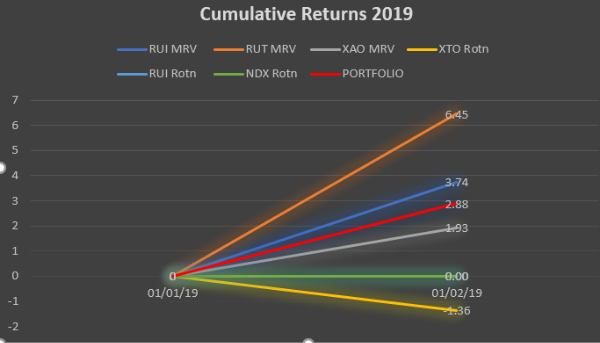

CheersFebruary 1, 2019 at 12:28 am #103205ParticipantHave been impressed with Said’s chart…so experimenting over next few months

Jan 2019

February 1, 2019 at 7:24 am #109585

February 1, 2019 at 7:24 am #109585JulianCohen

ParticipantNoice

-

AuthorPosts

- You must be logged in to reply to this topic.