Home › Forums › Trading System Mentor Course Community › Trading System Brainstorming › Same Day Trading Idea Discussed on the Group Call

- This topic is empty.

-

AuthorPosts

-

June 28, 2016 at 10:32 am #104499

SaidBitar

Memberstill way to early but here is the list of advantages and disadvantages of same day exit

Disadvantages:

[ol]

[li]no more dividends ( the dividends that i was getting they were covering the accrued interest on the margin account)[/li]

[li]no more having advantages of the over night gap up[/li][/ol]

Advantages:

[ol]

[li]no exposure to overnight gap downs (from what i noticed they tend to happen more often than gap up)[/li]

[li]Increase the margin from 2:1 to 4:1 (although I don’t believe it is good idea due to the fact that there have been some stocks that has distance from the Entry towards the Low of the day more than 25% although they closed higher but still 25% is all the real cash allocated for this trade example KOSP-200612 on 12/15/2005 the ROC was -27.3%)[/li][/ol]

It will be great if anyone can verify if there is any benefit from exiting on same day on the close, because there is chance i made mistake some where and day dreaming about the results

")

here is the code that should be modified

Code:if (LBIT[j]>=1)

{

Sell[j] = True;

SellPrice[j] = close[j];

LPriceAtBuy = 0;

}this will make exit on the same day and the exit will be on the close

June 28, 2016 at 10:36 am #104474ScottMcNab

ParticipantHmm. I suspect your correct..I used

if (LBIT[j]==1 AND Close[j])

{

Sell[j] = True;

SellPrice[j] = close[j];

PriceAtBuy = 0;

}June 28, 2016 at 10:39 am #104475ParticipantThe result I mentioned (same CAR but reduced maxDD) was using same leverage as when system was exiting next day.(35 at 5.5% for both)

June 28, 2016 at 10:42 am #104501Memberok then extend the stretch a bit more and actually make two stretches the first when the Index Filter is up and the second when the filter is down.

the reason behind extending the stretch more is to buy deeper in the dip and towards the low of the day.

June 28, 2016 at 10:48 am #104476JulianCohen

ParticipantI used the following, which Craig said was on the right track…I assume that means it’s OK. It appears to work.

Code:for (j = 1; j < BarCount; j++) { if (PriceAtBuy==0 AND LE[j]) { Buy[j] = True; PriceAtBuy = LEPrice[j]; BuyPrice[j] = LEPrice[j]; LBIT[j] = 1; } if (LBIT[j]==1) { Sell[j] = True; SellPrice[j] = Close[j]; PriceAtBuy = 0; } else if (PriceAtBuy > 0){

LBIT=0;

PriceAtBuy = 0;

}}

June 28, 2016 at 10:51 am #104477ParticipantI certainly got an improvement in both CAGR and MDD. I am going to investigate further, and I feel there is definitely something to be gained in combining this with a change in behavior on Index filter down.

June 28, 2016 at 10:55 am #104502ParticipantSaid Bitar wrote:ok then extend the stretch a bit more and actually make two stretches the first when the Index Filter is up and the second when the filter is down.the reason behind extending the stretch more is to buy deeper in the dip and towards the low of the day.

Thanks Said. It does this already but it just uses a couple of moving averages based on the stock price instead of an Index filter. I tried lots of things including atr ratios, index filters, distance from HHV etc and the moving averages seemed as good as anything else I could come up with.

June 28, 2016 at 11:12 am #104478TrentRothall

ParticipantI get a lot smoother equity curve and the results get a bit ridiculous when using 20 pos @ 20%. I think the idea would work – pretty well by the looks. Just a big hurdle would be placing the sell orders, a API you think could do it though. Also i think you would need to test a fair bit with adjusting the Close because i am thinking the fills wouldn’t be exactly correct

June 28, 2016 at 11:41 am #104503ParticipantTrent Rothall wrote:I get a lot smoother equity curve and the results get a bit ridiculous when using 20 pos @ 20%. I think the idea would work – pretty well by the looks. Just a big hurdle would be placing the sell orders, a API you think could do it though. Also i think you would need to test a fair bit with adjusting the Close because i am thinking the fills wouldn’t be exactly correctNick did mention that the API could be worked to handle the exits too…that would be quite nice. Leave it to trade for you while you sleep 👿

Why do you think the fills wouldn’t be correct?

June 28, 2016 at 11:42 am #104504MemberI am glad to hear that all are having similar results.

So most probably there are no mistakes

June 28, 2016 at 11:48 am #104500Anonymous

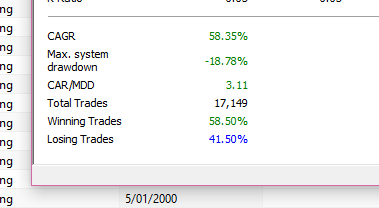

InactiveSaid Bitar wrote:It will be great if anyone can verify if there is any benefit from exiting on same day on the close, because there is chance i made mistake some where and day dreaming about the resultsI had a go with some interesting results: –edit: results based on 20/20 position size/max positions from 1/1/200 till 24/6/2016

Results at first glance are a bit misleading wtih my system. Here is the initial results table that looks good!:

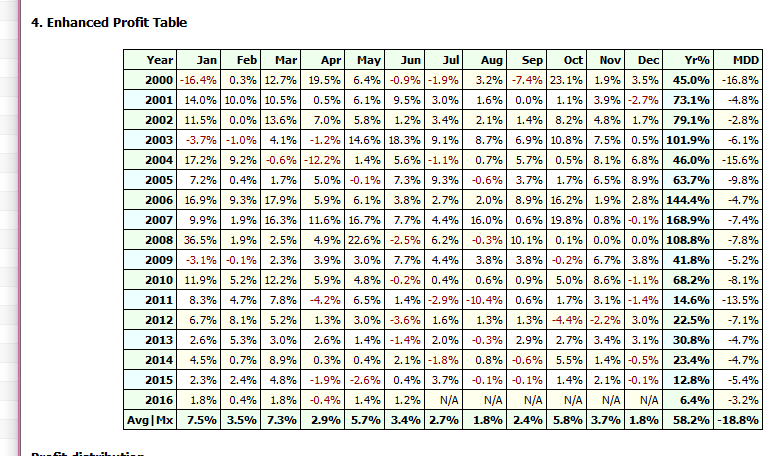

Then on closer inspection at the profit table. There are clearly some bumper years that skew the results:

Here is the code i dropped in (it seemed good at the time :unsure: ):

Code:for (j=1; j < BarCount; j++) { if(priceAtBuy==0 AND longEntry[j]) { Buy[j] = True; BuyPrice[j] = longEntryPrice[j]; priceAtBuy = longEntryPrice[j]; longBIT[j] = 1; Sell[j] = True; SellPrice[j] = Close[j]; priceAtBuy = 0; } }As well as the above code i made the suggested changes to increase stretch on the ATR when the index is down.

June 28, 2016 at 11:57 am #104505ParticipantNot many people made 100% odd in 2008!

June 28, 2016 at 12:06 pm #104507InactiveJulian Cohen wrote:Not many people made 100% odd in 2008!all we need is a time machiine…

Quote:Dr. Emmett Brown: If my calculations are correct, when this baby hits 88 miles per hour… you’re gonna see some serious shit.June 28, 2016 at 12:14 pm #104506ParticipantDarryl Vink wrote:Said Bitar wrote:It will be great if anyone can verify if there is any benefit from exiting on same day on the close, because there is chance i made mistake some where and day dreaming about the resultsI had a go with some interesting results: –edit: results based on 20/20 position size/max positions from 1/1/200 till 24/6/2016

Results at first glance are a bit misleading wtih my system. Here is the initial results table that looks good!:Then on closer inspection at the profit table. There are clearly some bumper years that skew the results:

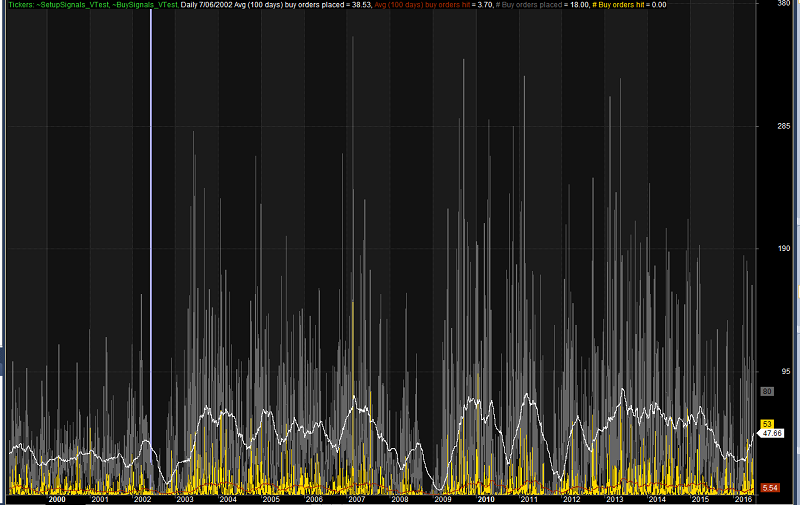

How does the ~buysignals chart look with 20/20 Darry ?

June 28, 2016 at 12:21 pm #104508InactiveScott McNab wrote:How does the ~buysignals chart look with 20/20 Darry ?… looks like a lot scott

-

AuthorPosts

- You must be logged in to reply to this topic.