Home › Forums › Trading System Mentor Course Community › Progress Journal › Nics Journal

- This topic is empty.

-

AuthorPosts

-

January 29, 2021 at 9:13 am #102097

nicBecker

ParticipantSo this will be a thread of random thoughts and observations over the next 6 months, basically something I can look back on and see my own progress. I hope to update it once a week.

January 29, 2021 at 9:14 am #112929ParticipantAs for my first 7 days since enrolment I browsed through the section 2 content. I figured there would be content that I would struggle wish and other bits that would be easier so I wanted to find that harder content just so I didn’t get caught later on. Alas I found the looping section. So that has been the focus this week. I don’t have a programming background but have been working through the code line by line trying figure out what it is saying. I then copied the moving average crossover system and some chart plotting from other pages to help visualise what the code is saying and that has really helped. This section will be something that I will have to come back to a couple of times but it should be easier next time. As for the 3rd looping assignment I won’t worry about that one for a couple of weeks :sick:

This coming week I will pick another of the later sections and work through that coding and maybe attempt some of the earlier assignments.

January 29, 2021 at 9:46 am #112931JulianCohen

ParticipantI found it was best to do everything on a big desktop computer…it’s much easier to throw a laptop out of the window…you tend to think twice with a desktop…just my 2 cents worth

January 31, 2021 at 8:32 pm #112932MichaelRodwell

MemberGood luck Nic!

Great idea to keep a journal along the way… I have revisited a few of my earlier posts and its a good way to gain perspective.

February 1, 2021 at 9:01 am #112933Participant😆 😆 Thanks for the heads up Julian

February 1, 2021 at 9:05 am #112965ParticipantThanks Michael, that’s the plan, also a bit of accountability

February 1, 2021 at 9:07 am #112967ParticipantMy first “System” before staring at the computer screen for 10mins. Its a start

")

//Moving Average Crossover;

// 50 day and 200 day moving averages

//need to create a list of a system;

// i.e. entry, exit, position sizing, market, filtersFastMA = MA(Close, 50);

SlowMA = MA(Close, 200);Buy = Cross(FastMA, SlowMA);

Sell = Cross(SlowMA,FastMA);//============================================================

//Chart Plotting

//============================================================Plot(Close,”Closing Price”,colorDefault,styleBar);

Plot(FastMa,”Fast Moving Average”, colorRed,styleLine);

Plot(SLowMA,”Slow Moving Average”, colorGreen,styleLine);//Importance of coding settings, so i think SetOption and then I need a list of things to think about for these

//short cover is the first obvious one as the system wouldn’t run without me going into the settings for that one.

//I also need to go through chart plotting and indicators on the chart to see the buy and sell points.March 19, 2021 at 2:44 am #112930ParticipantSo its been a little while since updates. I’ve finished going through the theory section and have been playing around with a mean reversion based system.

Essentially this one uses a z-score to find a value away from the mean. I think the results are not tooooo bad except for 2018 onwards. However I seem to be going around in circles ATM trying to figure a way to curb that level of drawdown.

March 19, 2021 at 8:37 am #113094GlenPeake

ParticipantHi Nic,

A couple of thoughts come to mind….

What sort of numbers, CAR/MDD would you like to realistically be aiming for?

Are you using margin for this system or is this a cash account?

What universe are you testing? Russell1000?

For me just looking at your stats from 2014 to current… How would you go if you had been trading the system LIVE starting in 2014 through to 2019 where the biggest return was approx. 17%, for the year of 2016? How would you be feeling…? (From my perspective…. I would maybe find it a bit tough). But for you, maybe it’s close to what you’re looking for etc…..

What combination of number of positions/position size have you tried….? e.g. is this system 5 positions @ 20% or 10 positions @ 10%..etc. or another combo etc. perhaps play around with these settings/parameters…and see what comes out.

FWIW, my system(s) kind of under performed in 2014/2015. (similar to your stats).

The post covid 2020 performance for Mean Reversion systems ‘in general’ was pretty favourable, so for me in hindsight, it would be nice to see ‘strong’ out performance from a MR system post that March 2020 period. But, having said that, each system is different and built by differing personalities, so there might be a degree of ‘risk management’ / volatility parameters built into your system etc…. hard to say for sure from where I sit….. but what I’m trying to say is….. generally I’d like to see ‘out performance’ during this period….i.e. really cash in etc

As a comparison, here is my MR#1 system that I trade live on the Russell1000 using 5 positions @ 20% per position (i.e. no margin)….

2015/2016 and the COVID period were the deeper drawdown periods for me.

March 19, 2021 at 8:51 am #113096Participant

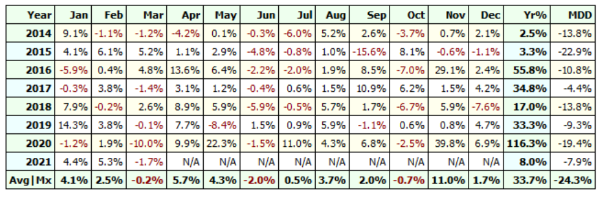

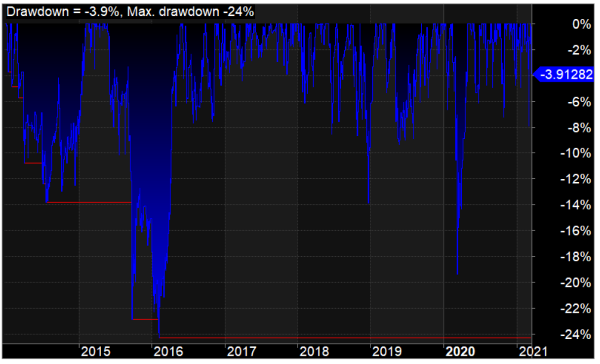

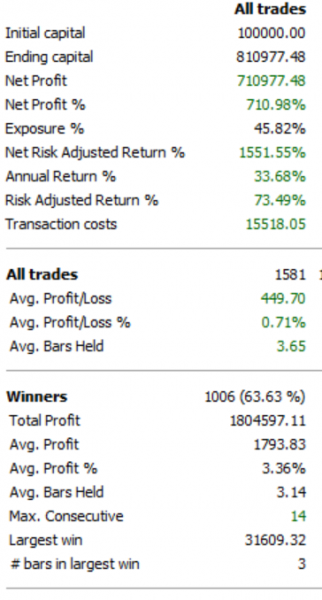

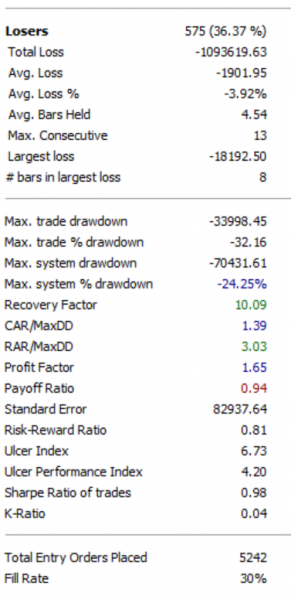

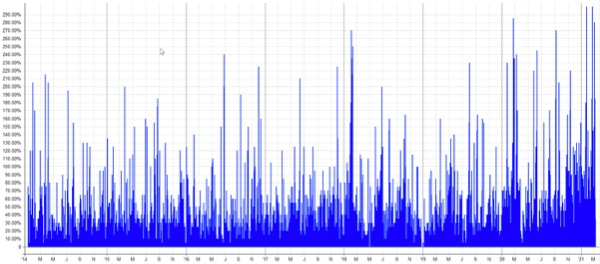

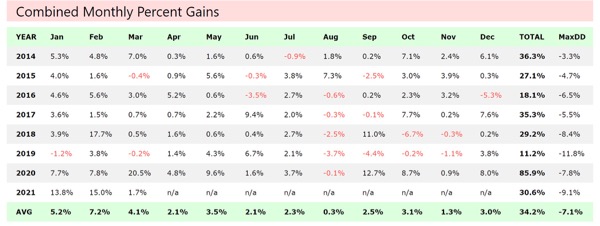

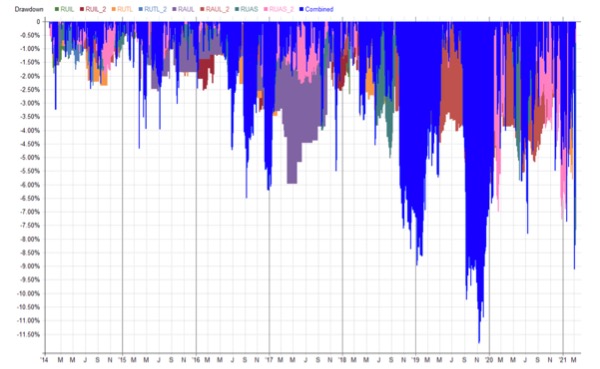

March 19, 2021 at 8:51 am #113096ParticipantGlen has made some very good points. I’m not sure in live trading after 2 years of < 10% CAGR you would still be trading this, and that happens twice since 2014. I just ran my MOC from 2014 to give you a comparison. This is a portfolio of strategies, but basically is two or three ideas/algorithms, run on a variety of different universes in order to give diversity. I’m using Real Trade so it’s a little harder to say what the actual margin is, although it works out as 310% maximum; every strategy has either 5 positions at 10% of the total portfolio equity or 10 positions at 5% of the total portfolio equity. Here is the Usage graph

Here is the Drawdowns and CAGR

March 19, 2021 at 11:52 am #113098

March 19, 2021 at 11:52 am #113098Howard Lask

ParticipantThose are awesomely impressive stats Julian, many thanks for sharing.

March 20, 2021 at 1:05 am #113095ScottMcNab

ParticipantNic wrote:So its been a little while since updates. I’ve finished going through the theory section and have been playing around with a mean reversion based system.Essentially this one uses a z-score to find a value away from the mean. I think the results are not tooooo bad except for 2018 onwards. However I seem to be going around in circles ATM trying to figure a way to curb that level of drawdown.

If its not too much, maybe try adding one more parameter ?…such as

C>MA

IndexC>IndexMA

ROC(C)<-?

C

variable PS (lower PS if C

variable stretch for buylimitMarch 20, 2021 at 11:39 am #113097ParticipantThanks Glen!

Not sure if you have the data going back till 2000 but that would be impressive if you’re getting similar results. I thought my results were not too shabby up until around 2013 (not sure what the annualized return is but probably high 20’s. I guess at the moment I have kinda rationalised that away on the sense that post 2010 markets may have behaved a bit different than prior – ‘the death of mean reversion’, lower returns on value funds vs growth funds. So i thought that would align itself with Nick’s thoughts of a combination of strategies – there would be times were mean reversion may under-perform and times when trend following would out perform.

I don’t really have a return profile that i’m after – obviously greater than a passive buy and hold post expenses. I’ve always been under the belief that ~15-20% p.a. is something to aim for, but maybe that’s a bit naive. Those backtest results were in the R1000, cash only, and using a 10% / 10position allocation. Again, i would have thought having only 5 positions active would increase your potential risk of a drawdown.

How would I have felt trading it? with much envy compared to your last 5 years!

thanks for your comments

March 20, 2021 at 11:45 am #113099ParticipantJulian….returns relative to drawdowns :woohoo:

I presume being market on close your volatility or drawdowns would naturally be quite low. Do you find all your systems have similar return/drawdown profiles or do they support each other to create the end result?

My systems would be purely be cash only with nil / minimal margin.

I think I have some work to do.

thanks

March 20, 2021 at 11:51 am #113100ParticipantHi Scott,

I will have a look over the coming days as I have to work tomorrow onwards for a few days. I have run the system using say, larger then normal equity and a low % allocation and maximal open positions to try and see how many trades are possible before position sizing and ranking. There is definitely some room to move with additional parameters.

More out of interest would be to find out why over recent times performance has waned relative to 2000’s.

Thanks

-

AuthorPosts

- You must be logged in to reply to this topic.