Home › Forums › Trading System Mentor Course Community › Progress Journal › Matthew O’Keefe’s Journal

- This topic is empty.

-

AuthorPosts

-

August 7, 2020 at 1:07 pm #111980

Anonymous

Inactive1) I want one of those little daily calendars with Len’s motivational quotes on them.

2) Disco.Long was much cooler before I realized it was “discretionary” long. How lame is that compared to something like using a disco ball for a random number generator, or Earth, Wind & Fire songs to place your entries. Ugh. Disappointed.

August 10, 2020 at 2:00 am #111981MichaelRodwell

MemberMatt,

I have a discretionary itch that i like to scratch occasionally… good luck!

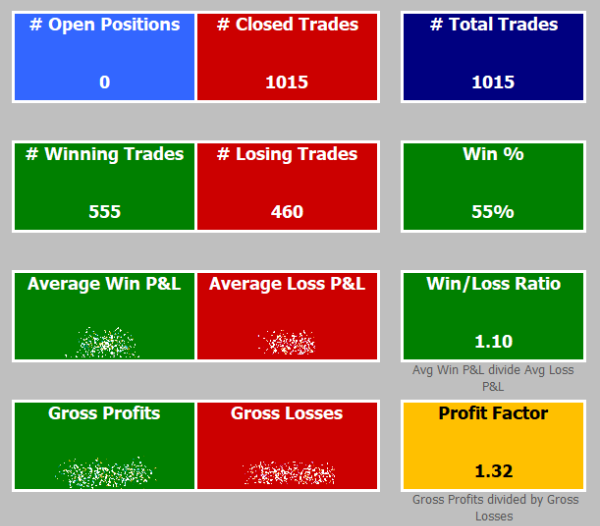

August 10, 2020 at 11:12 pm #111636InactiveWell I made an interesting milestone today. 1000 trades on my combined long/short MOC system which I have been running since 26th May.

Here is how it is looking….

So overall it is going well.

To be honest I was hoping to get Win/Loss Ratio a bit wider to more like 1.2 which would then get Profit Factor up a bit to more like 1.4 or 1.5, however 1.32 Profit Factor is still fine.

It was in fact running at around the 1.5 to 1.6 Profit Factor level up until end July at which point in the last week or two I have been hit by a few heavy losses on some earnings announcements going against me. Still, I need to be prepared to trade at all times, including through earnings, because history shows these periods can provide some juicy returns. I think things are a little “Weird” at the moment in regards to earnings. Some things which don’t meet earnings still pop up and keep going up, then others that still meet their earnings expectation drop, and keep going lower. Certainly some weird times we are in…

YTD performance is at about +7%, which is great considering it has only been running since end May. If that is near enough to one quarter of performance I should surely be able to get a 20% plus CAGR, which is all that I’m hoping for. This is not supposed to be a “load the boat” strategy, so a nice comfy 15 to 20 CAGR would be more than enough on a simple, take your brain out, leave your opinions at the door, just press the damn buttons each day you idiot kind of strategy like this.

Weaknesses at the moment are the flat spots in the short side between the volatile periods (you will have seen this in my previous posts where in the volatile periods the short profits are great but outside of these periods the returns are quite flat) and also that the long side is down (short side doing all the heavy lifting right now).

So a bit of work needed on both the long and short side. I am combing through my systems to see if there are any obvious things I can do to smooth out the ride. Some ideas include;

– Adjusting the number of positions along with a minimum threshold for the ranking (instead of just “above 0” which is what I currently have Ranking set to).

– Minimum dollar value of $20 or $30.

– Minimum volume/liquidity requirement.

– A longer range for the Barcount minimum, say 1000 days (Idea being that a stock needs to have traded for at least 3 or 4 years before I’ll start trading it. This might help with general stability of what is traded. Perhaps it could be that super young stocks are much more erratic, volatile etc and not following the general pullback/reversion characteristics of more mature stocks.

– Using much wider increments in my parameters/optimization steps so I hopefully am targeting much broader plateaus in my settings which may be more repeatable/dependable into the future instead of unique peaks in settings (E.g. for Percent Multiplier on ATR stretch price do it on increments of 0.1 so it is like 0.8 or 0.9 or 1.0 or 1.1 or 1.2x instead of doing it on finer 0.02 increments like 0.9 or 0.92 or 0.94 or 0.94 or 0.96 etc.

– Instead of using an Index filter to stop me from trading in general when things are bumpy perhaps use something more aimed to the individual stock like perhaps a 15 day RSI below 20 means I shouldn’t be trying to go long or above 80 means don’t go short because this would mean the stock is really quite extended in the direction you don’t want it to be going if you are going to expect a quick one day reversion.

August 10, 2020 at 11:39 pm #111987JulianCohen

ParticipantA couple of initial thoughts.

1. Be careful of over optimisation…changing the parameters too much. The broader the better I would think.

2. My way of thinking is that if you are using smaller increments in the ATR stretch already, that could be over optimisation. I’d be looking at that first. I only ever use 0.1 increments; I hadn’t thought to use anything smaller to be honest.

3. I managed to find a short system that didn’t need an index filter so I’d also put that high on the list too. Something that keeps you trading irrespective of market conditions.August 11, 2020 at 12:10 am #111988InactiveThank you for the feedback Julian.

Yes, definitely want to avoid the over optimization trap. I wasn’t using increments of 0.02 on my stretch, was just illustrating the point. But yes, was using 0.05 which might be on the edge of too fine also. I have been using 0.1 in my latest tests and still coming up a winner with some good broad regions to be working within.

Index Filter: This is a hard one. Having it helps the heart, those moments when the market is falling apart and you start to worry. Not having it is probably the right thing to do though, from a pure data and trade maximization perspective. Of course finding the right balance between what your head and heart can do each day is important.

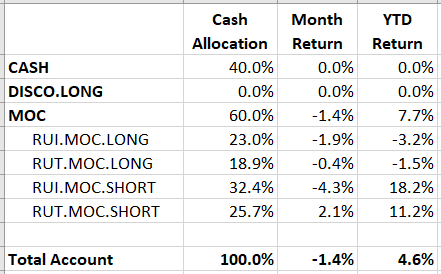

September 2, 2020 at 2:27 am #111989InactiveWell it was a down month for me.

Still trading the MOC only system.

So three out of the four MOC strategies were down.

Overall there were some long tail trades both long and short that took the shine off. The overall win% is still generally on track, just the win/loss ratio is out of kilter

It seems that a few of the Bio/Pharma stocks are fluctuating wildly on even just a sniff of news on anything remotely related to coronavirus, good or bad. For example one company that has an announcement which could mean its virus treatment will be released soon of course means the competitors suffer so on some of my long positions those competitor companies then drop 30% in one session.

Similar story on the short side. Tech stocks that just relentlessly go up for no typical reason whatsoever. I mean, an announcement where the earnings are actually less than expectation, and yet it still rockets up by 25% in the session. Crazy.

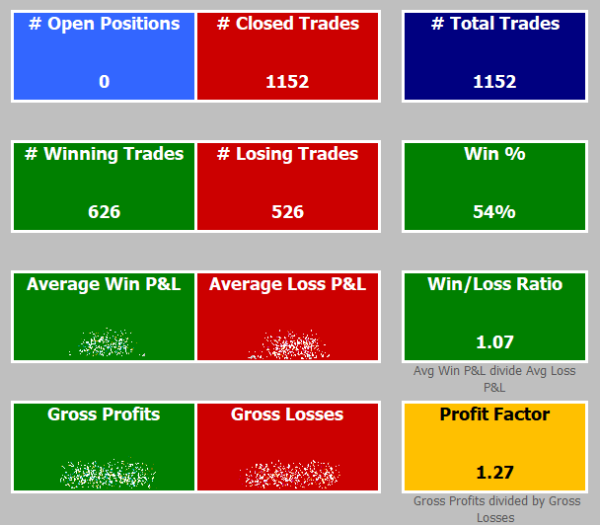

Here is how the system across all four strategies is going since launch in May. As you can see the long term stats are still all going fine. It is definitely the long game…

In order to combat the Bio/Pharma volatility I did some backtests to see if I excluded this sector for a while if this would be of benefit. Overall, no, history shows I should leave it in there as it does provide a bit of an influence on the results. This means I will just have to whether the storm and quit my whinging.

Still, to have my first down month since go live is nothing to complain about. At just a -1.4% result it is definitely within expectation.

Going forward, for the month of September I have decided to park my MOC system (which is the only system I have been trading last few months) because I am working on my longer term system. I will do another post on that one….

September 2, 2020 at 3:32 am #112094InactiveOK so I have been working on my Discretionary Long system. I am starting to do some manually managed test trades this month.

As a refresher, the methodology I am trying is to look for stocks breaking out to new highs and may have further upwards momentum. It is very much a momentum or O’Neil/Minervini style methodology looking for patterns etc.

The development of my API to manage this system/trades is not complete yet, but it is getting there. So in anticipation of getting to use it soon I thought I would start trading the method (but manually managed by me during the open and in the first hour or two of the live session). I thought that this would give me some real live trade practice on this method so that I can be more confident that my system/method actually works such that when the API is ready I can be confident in what I need it to do correctly and I would therefore have more conviction in enabling it when it is ready.

In order to do this well I therefore just can’t have the MOC system running at the same time in the live session because it will be too much noise for me to bear if it is a day of many fills and I won’t be able to run this discretionary thing properly/clearly at the same time. So the MOC trading will be parked this month (September).

I have decided I will run it in two baskets. Discretionary long trades with your typical patterns, breakouts etc will be named DISCO.BREAK and the discretionary system in much a similar manner but for IPO’s will be DISCO.IPO. I will probably also do a DISCO.PENNY at some point to try and target moves on penny stocks but that will come later. For now it is the breakouts and the IPO moves that I will focus on.

I am using Marketsmith for my tool in finding my target symbols. I find it provides a clean enough interface and also has some nice pattern recognition tools that can sometimes help me target the right symbols. Of course part of the O’Neil/Minervini methods is a connection to fundamentals somewhat. Although that may be a dirty word in some camps, it is clear this dimension has helped these traders in time, so even though recent price action may dictate fundamentals are superfluous/irrelevant I am not going to try to reinvent the wheel at this stage and simply take it as a given that I need to consider it in my approach. For this reason, I cannot entirely use Amibroker for this method.

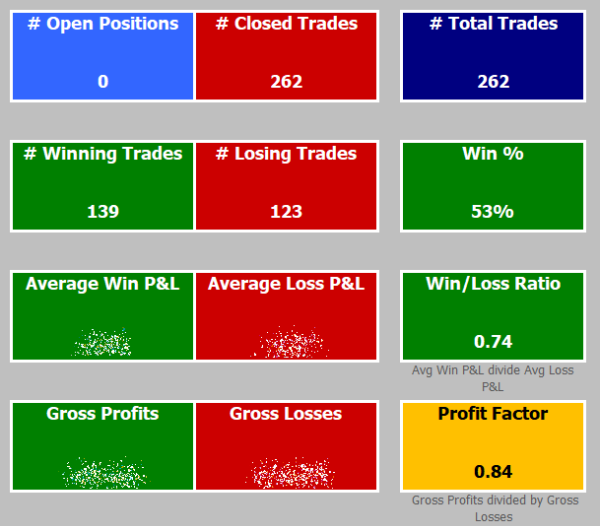

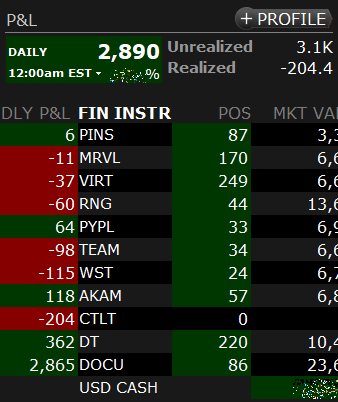

So, interestingly enough, I started the ball rolling on the system last night. Here is how it went just after the first session…

I had a total of 30 symbols on order. I had fills on 11 of them. I wouldn’t expect there to be any more than 10 or so symbols running on this system at any one time. The experts running these systems promote keeping the position count low, because you want to reward the winners and have a reasonable amount of exposure to large movers. I won’t reinvent the wheel. I’ll also target 5 to 10 at any one time.

I don’t mind sharing real dollars on my progress at the moment as it is just test trades/amounts to get a feel for it. I’ll ramp up the dollar amounts/position sizes when I can see I am doing it right. It is not the paper account as it just doesn’t give you the sense of ownership. The only thing I am using the paper account for is to ensure the API is doing the right things in terms of order execution.

The stats already produced in just one day of trade already look like what they are probably going to be over the long term. A win% of 30 to 40% is all that it is probably going to be. Win loss ratio at 8 is probably expecting a bit too much. It is inflated because of the big DOCU move today. I am hoping this can be more like 4 to 5 over the long term, which in the end should still make for a decent Profit factor of 2 more more.

I only had one position stop out at the 3% stop loss position which was CTLT. The CTLT buy order only executed on the lowest of the three buy targets, by the way.

It will be interesting to see how my mind approaches this strategy with its ups and downs and the balance between open/unrealised and closed/realised profits. In the past I have struggled with this because in particular on the momentum strategies which typically don’t run with an active stop loss methodology and you only close an open position tomorrow as a result of what market action happened today (or at the anniversary point like once per week or month on the rotational methods) as opposed to being able to do something immediately actively at any time in the live session is where I’ve struggled.

The way I am running this strategy is with active stop loss and trailing stop orders with a GTC validity. This is the part of the equation that I think I was missing from previous strategies/methods because I was always annoyed that there would be 4 more trading sessions until the rotation date and the stock was already tanking and I’d be so annoyed that I was “not allowed” to do something about the position. Or if there was some crap news 30 minutes before the open and I have already completed my analysis from the previous day and entered my orders two hours ago and already left the screens for the day and yet my orders execute at the open and then during the live session things just get worse and then after the close of that day I then do the analysis and it says I need to sell on the next open and then of course the overnight out of hours session just makes it worse and then I sell at the next open on an even steeper loss. In moments like this, having an active stop order in place which can simply take the action for me would give me a much greater peace of mind that I have less chance of being exposed to massive losing moves whilst “not being allowed to do anything because those are not the rules”. I know where the arguments lie, locking in steep losses with stops without giving them the chance to turnaround and correct, so I am just going to have to see how I go with that in time.

More on the order management methodology…

I am splitting each buy order up into three portions, with one third of the total volume on each. Buy orders are buy Stop above current market price (I am targeting an upward move of price into my target buy zone which will then hopefully mean momentum and keep pushing upwards) and the stop loss prices are three various percentage prices below fill, as well. One at the bottom of the price target zone, one in the middle and one at the top.Of the three orders/prices each one gets given a 3/6/9% initial stop loss price below the actual fill price (not the buy stop price). Of these three they are then also issued with a 9/18/27% trailing stop. So these are 3% initial stop + 9% trail, 6% initial stop + 18% trail, 9% initial stop + 27% trailer. The concept here is obviously to allow varying degrees of flexibility in price fluctuations.

Of these three they are each then further split up into two portions with a profit taking bracket order on one portion only. At this point I am using a 50% split at a 27/54/81% profit target. So if for example I had a symbol with total 10,000 volume position buy and the price moved only through the first of my target price buy zones only the first buy order will likely fill and for 3,333 units only. Then this 3,333 units position will see 1,666 units issued with a sell order of 3% initial stop, 9% trailing stop and that’s all. The other 1,666 units will be issued with a 3% initial stop, 9% trailing stop and 27% profit taker. Obviously the idea is that a portion will sell for a profit on a quick positive move should it happen, yet I’ll still hold a portion for longer term gains should that happen.

All the buy orders for today’s session are DAY validity and all the associated sell orders are a GTC validity. The concept is that if any buy order does fill today, the API will intercept and do its work on setting the appropriate hard sell stop price, percent trail and hard profit taker price with GTC validity so once the session and API closes today these GTC orders can effectively run into perpetuity and I never have to think about them again and the API does not need to pick them up to manage them any further tomorrow. This will help if I miss any trading days or decide to take a holiday.

The only portion of these positions I will have to manage into the future will be the portions that are still held from the non-profit taker portions, which if everything is going swimmingly, should be in profit and may be mentally ‘easier’ to sell out of manually at the right times or make further decisions on when things are just rocketing along in the future.

The reason I have approached this 3x3x3 (or “three three’s” method as I’ve decided to call it) is because after reading a number of books and following certain other successful traders many of them have different ideas on all of these fronts.

On entries, some buy right at the bottom of their target price zone and “Add to it if proven to be correct”. Others buy in the middle of their target zones and some even right at the top of their target price zones.

On exiting/managing open positions, some like using tight initial stops in the 3 to 5% zone. Others like initial stops in the 7 to 10% zone.

On profit taking, some of the experts say they do take a portion or half, others say they don’t take a portion and manage it by hand as things play out or only on the very extended moves.

For the trailing stop methodology, some use it, some don’t (or they use moving averages for stops and manage them manually). Some say to stay tight at 8 to 10% trailer. Others like more flexibility to allow for larger moves and set it at 20 to 30% trailer.

So overall my idea of devising this methodology is to have flexibility in some of these ways/methods of entry and exit (and drive it with an API to automate as much of this as possible) because the clear issue with many of the traders in this style is consistency. Either they say their pitfalls are that they have not been honoring the rules or not doing what they are supposed to be doing. I know that I am not going to be any better at managing/controlling these sorts of issues than they are, so the only way for me to make it work is to be a robot in approaching it.

Will the 3/6/9 and 9/18/27 and 27/54/81 and 50/50 profit take splits actually work well? Who knows, perhaps it may even be detrimental and I am trying to put too many insurance policies into play, but only time will tell and I can surely adjust in time.

September 2, 2020 at 7:00 am #112097ParticipantJust my two cents mate. Why park the MOC for a month? If it makes money in backtesting you will kick yourself.

Just run it and don’t look at it. Treat it as an exercise in intestinal fortitude

") September 2, 2020 at 7:04 am #112100

September 2, 2020 at 7:04 am #112100TrentRothall

ParticipantOr open a sub account and trade it in there. Agree with Julian, if you’re after the law of large numbers don’t hinder it for a month

September 2, 2020 at 7:13 am #112101InactiveIt is hard not to look at it when I am trying to manage the positions in the long system at the same time. I have to watch the open and see what fills during the first hour or two in my long system. If I am trying to do that whilst there are a butt load of fills one day, I will not be constructive.

Anyway, maybe I will get more confidence after a few days and try both at the same time.

September 2, 2020 at 7:20 am #112102ParticipantFair enough, you know yourself

September 2, 2020 at 8:17 am #112103ParticipantThink of it as a Zen exercise. If you can get on with your other system whilst ignoring the MOC you’re winning.

Or you can look at the MOC but just notice what it is doing and move on. There’s the exercise for you. If you can do that then you’ll be well on the way to helping your own mind ignore what is going on, and leave the system, that you have backtested to buggery, alone to do it’s thing and make you money.

After all how can the punters turn up at your casino if you shut the doors!

September 2, 2020 at 8:31 am #112105InactiveForgot to say, I think it would be hard to open a new corporate account in a short period of time. IB aren’t the best at moving quickly at the best of times…

September 2, 2020 at 7:07 pm #112104InactiveAgree with Trent and Julian. You are the “let the law of large numbers and large essay blocks play out” guy after all. Find a way to run it at the same time. Sub-account as mentioned?

September 3, 2020 at 1:01 am #112106ParticipantYou can open a sub account, i run two. It’s quick to setup i think from memory

-

AuthorPosts

- You must be logged in to reply to this topic.