Home › Forums › Trading System Mentor Course Community › Progress Journal › Julian’s Journal

- This topic is empty.

-

AuthorPosts

-

October 2, 2019 at 5:07 pm #104250

JulianCohen

ParticipantSeptember’19

Short-Term Systems

US MR: -5.69%

US MOC: 1.22%Long Term Systems

S&P 500 Momentum: -3.87%

NASDAQ Momentum: -2.98%

Long Term NASDAQ: -4.48%

US WTT: -11.17%ASX Growth 2.38%

Total Account: -2.64%

November 2, 2019 at 2:05 am #104251ParticipantOctober’19

Short-Term Systems

US MR: 0.39%

US MOC: 3.85%Long Term Systems

S&P 500 Momentum: 3.02%

NASDAQ Momentum: -1.42%

Long Term NASDAQ: 4.85%

US WTT: 5.19%ASX Growth 1.46%

Total Account: 0.98%

November 4, 2019 at 1:34 am #104252ParticipantI discovered a trade I hadn’t logged in my Growth Portfolio….IFM.AU which has increased by 50% since purchase in March so all my Growth Portfolio figures were understated for most of this year. Still, not recording the actual Buy is a lot better than finding I should have bought it but hadn’t!

So for me this adds a procedure into my end of month chores. Compare actual holdings in my brokerage accounts with the holdings I am showing in STT. Because I am running 7 different systems this is a process I should have been doing all along but will be doing in the future.

November 4, 2019 at 4:58 am #110530Nick Radge

KeymasterYep. I do it weekly across my portfolios.

November 4, 2019 at 9:25 pm #110531TimothyStrickland

MemberNice Julian, a good error to make I guess. I had to start doing that out of necessity because I had thought my system wasn’t working for a while, now I check it weekly to make sure the trades that I took match everything.

November 12, 2019 at 1:40 am #110541ParticipantWell actually you’d think it was a good error to make but think of the extra funds I didn’t invest when adding on over the last few months.

November 30, 2019 at 3:16 am #104253ParticipantNovember’19

Short-Term Systems

US MR: 3.03%

US MOC: -1.71%

US RUA MOC: -0.8% 207 tradesBacktest results 0.18% 265 trades….not looking good if it’s missing around 20% of trades. However during trading I didn’t notice such a large discrepancy on a daily basis so I will start logging daily differences for next month and see how it compares

Long Term Systems

S&P 500 Momentum: 5.82%

NASDAQ Momentum: 4.08%

Long Term NASDAQ: -0.39%

US WTT: 4.13%ASX Growth -3.24%

Total Account: 1.73%

December 10, 2019 at 2:02 am #104254ParticipantI started trading an MOC system on the R2000 on 5th November

So far the backtest is down 0.76% but actual is down 3.5%

Last few days it has done 10 or so trades each day and the one trade it has missed is the one that made the profit that would have made it level with the backtest.

Alongside this I have been trading a different system on the SP1500…no issues at all.

I realise I should probably run it for a longer period of time, but I won’t be able to increase the equity in it if it performs like this, so I’m close to binning it.

I realise that my underlying bias is that this would happen, as is obvious from my previous posts, but is this confirming my bias? Am I allowing the missed trades to make me guilty of confirmation bias?

Thoughts?

December 10, 2019 at 2:05 am #110672ParticipantMy first thought is the “binning ” might have only one n

December 10, 2019 at 7:08 am #110673ScottMcNab

Participant2 n’s..as in sinning ..

I have R3000 system going live 1Jan…tests are with price/vol/turnover at $1/500k/1M …what are u using live J ?December 10, 2019 at 7:10 am #110674Anonymous

InactiveJulian,

Any hints on position sizing, number of positions etc?

Also I am guessing it is using some method for ranking, picking stocks.

I continue to have good success with my R3000 MOC, including backtests accurately reflecting the live traded results. The only misses are those after 3.43pm, but that will be any MOC based system.

December 10, 2019 at 8:45 pm #110677ParticipantI’m running 80 positions at 5% with volume filter at > 250,000 as there are no positions over 1000 shares in a day. Price filter > $1

Too aggressive on the Volume filters do you think, allowing too many “non performing” tickers

Ranking is ROC

December 10, 2019 at 10:55 pm #110678InactiveDoesn’t sound too aggressive to me. At the R3000 level even the lowest market cap companies at the bottom of the pile are still worth something like 150m USD plus. So they are not exactly small companies with 50 employees or penny stocks. I’m doing similar number of positions and size, and I’m even using a $10 min and still getting plenty of signals and fills.

Over what period do you do your ROC ranking?

Any other indicators/methods for a buy signal?

December 10, 2019 at 11:38 pm #110679ParticipantThe ROC is 3 days

The issue isn’t so much with plenty of fills, it is missing those one or two fills that actually make a big difference to the P/L. Maybe I am judging too small a sample size time wise.

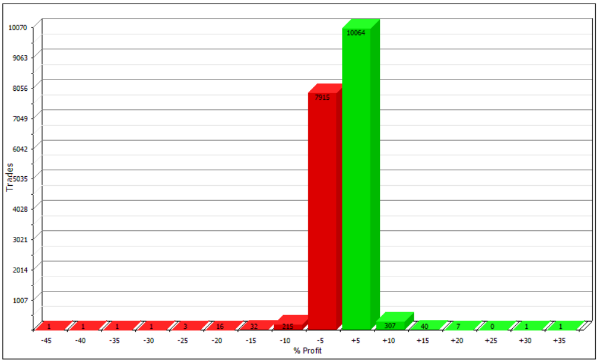

December 11, 2019 at 12:29 am #110680InactiveAre those few magic fills that were missed in the lower range, price wise? I mean, are the missed trades 1, 2, 3 dollar stocks or are they $10+ stocks?

What’s the distribution of trades look like?

Here is mine below over a 15 year period. Around 18,000 trades. Sure, I wish I didn’t have a few of those long tails, but there are only a handful of trades in there. Also if I manually delete those long tails from the backtest results (about 280 losing trades greater than 5% loss, about 350 trades greater than 5% profit) then the overall results are pretty much the same which is just perfect. My annual CAR might go from perhaps 18% to 17% when I do this (DD doesn’t change too much either). You want the profits/drawdowns coming from the bulk of the trades in the +/- 5% band, not from a handful of long tails (which would seem to be your issue at the moment).

My price filter is $10 minimum. Maybe there is something to be said that even though our systems are based on percentages of price and ATR’s etc, that still generally speaking the lower priced stocks in the 1, 2, $3 area that these more wildly fluctuate in a day of trade than those above 10 bucks? Not sure if I’m right or not, just a wild theory.

I also notice that even though I do “unadjusted” pricing for backtesting that I still get results for trades from many years ago (very early in the period, for example I test over last 15 years, and in those first years I am still getting trades on 50 cent, 1 dollar, 2 dollar stocks). I can only assume that the unadjusted values are used in the backtest, but you do still take fills in the backtest if the price, adjusted for dividends etc, is Today’s equivalent of your price limit. Again, for me, this only represents about 400 trades below 10 dollars in 18,000 trades, and again I delete them from the results and the total results over time change very little which again is just perfect because this tells me these are not skewing my results. The reason I raise this point is perhaps with you at a $1 limit means you may actually be getting some results from 15 years ago in the 5 or 10 cent region? These must surely be wildly fluctuating in a given day, moreso than the larger cap stocks.

-

AuthorPosts

- You must be logged in to reply to this topic.