Home › Forums › Trading System Mentor Course Community › Trading System Brainstorming › Group Collaboration System Ideas

- This topic is empty.

-

AuthorPosts

-

May 17, 2016 at 2:05 pm #103997

SaidBitar

MemberMaurice Petterlin wrote:Said Bitar wrote:Maurice Petterlin wrote:sell – Close is above MA 5 days or crosses with MA 5 days?It is the same

I don’t think so. Cross is only true at the point it crosses, Close is above MA 5 is always true as long as the close is above the MA

Technically speaking you are right, but for this system your buy signal is under the MA all the time

This is why I said it doesn’t matter

In my code I use crossMay 17, 2016 at 2:07 pm #103998MemberMaurice Petterlin wrote:Darryl Vink wrote:Maurice Petterlin wrote:Code:Cond1 = C < LowerBand; //close below lower band Cond2 = C > MA(C,MArange);

Cond3 = VolFilt AND IndexUp AND UniverseFilter;

Cond4 = BBWidth > 5;Hi Maurice. Do your need to add something like “AND HDBFilter” into your “Cond3” ?

Correct, It did change the results

I’m wondering why the results should be different if I turn HDBFilter off and use the inbuilt filter set to Russel 1000 historical constituents?

Because you are testing on bigger universe I think this is why the results are different

May 17, 2016 at 2:15 pm #103725LeeDanello

ParticipantSomething doesn’t add up for me.

I think there should be no difference in results between scenario1 and 2Scenario 1.

+

or

Scenario 2.

+

May 17, 2016 at 2:23 pm #104000ParticipantSaid Bitar wrote:Maurice Petterlin wrote:Darryl Vink wrote:Maurice Petterlin wrote:Code:Cond1 = C < LowerBand; //close below lower band Cond2 = C > MA(C,MArange);

May 17, 2016 at 2:23 pm #104000ParticipantSaid Bitar wrote:Maurice Petterlin wrote:Darryl Vink wrote:Maurice Petterlin wrote:Code:Cond1 = C < LowerBand; //close below lower band Cond2 = C > MA(C,MArange);

Cond3 = VolFilt AND IndexUp AND UniverseFilter;

Cond4 = BBWidth > 5;Hi Maurice. Do your need to add something like “AND HDBFilter” into your “Cond3” ?

Correct, It did change the results

I’m wondering why the results should be different if I turn HDBFilter off and use the inbuilt filter set to Russel 1000 historical constituents?

Because you are testing on bigger universe I think this is why the results are different

Lets accept the better results then

May 17, 2016 at 2:34 pm #103999

May 17, 2016 at 2:34 pm #103999Anonymous

InactiveMaurice Petterlin wrote:I’m wondering why the results should be different if I turn HDBFilter off and use the inbuilt filter set to Russel 1000 historical constituents?My understanding is:

– When you use the filter settings it provides the entire universe of symbols to run over

– When you use “IsIndexConstituent()” (from your HDBFilter) you are verifying the symbol exists in the filter list at that given dateJust setting the filter settings to Russell 1000 and Historical Constituents will include every symbol that has ever existed in the Russell 1000 over the entire period.

Hope that makes sense…

May 17, 2016 at 2:56 pm #104001MemberDarryl Vink wrote:Maurice Petterlin wrote:I’m wondering why the results should be different if I turn HDBFilter off and use the inbuilt filter set to Russel 1000 historical constituents?My understanding is:

– When you use the filter settings it provides the entire universe of symbols to run over

– When you use “IsIndexConstituent()” (from your HDBFilter) you are verifying the symbol exists in the filter list at that given dateJust setting the filter settings to Russell 1000 and Historical Constituents will include every symbol that has ever existed in the Russell 1000 over the entire period.

Hope that makes sense…

EXACTLY

the number of symbols are exactly same but it is related to the dates

suppose XYZ was in the Russell 1000 starting from 1/1/2015 then it will be in the list but you can only take trades in it starting from the date that is listed. this is the difference. Not the number of symbols but the dates (number of bars )May 17, 2016 at 3:15 pm #104004Member@ Trent

i tested 20 positions 5% per position from 2000 till 2016 my results are a bit far from yours, the number of trades is almost half

May 17, 2016 at 3:23 pm #104002ParticipantDarryl Vink wrote:My understanding is:

May 17, 2016 at 3:23 pm #104002ParticipantDarryl Vink wrote:My understanding is:

– When you use the filter settings it provides the entire universe of symbols to run over

– When you use “IsIndexConstituent()” (from your HDBFilter) you are verifying the symbol exists in the filter list at that given dateJust setting the filter settings to Russell 1000 and Historical Constituents will include every symbol that has ever existed in the Russell 1000 over the entire period.

Hope that makes sense…

Sorry Darryl a bit confused..

Instead of the entire period, you mean that it includes the historical constituents for the dates tested. So if you exclude the HDBFilter you could be including stocks that weren’t part of the Index during your test period?

The video from http://edu.thechartist.com.au/guruTasks/7/41-section-2-module-18-full-system-coding-part-8-monte-carlo/284-historical-constituents.html shows the HDBFilter and filter = Russell 1000 Historical Constituents being selected.

May 17, 2016 at 3:38 pm #104005ParticipantSaid Bitar wrote:@ Trenti tested 20 positions 5% per position from 2000 till 2016 my results are a bit far from yours, the number of trades is almost half

What are you using wrt trade size limits or other settings?

May 17, 2016 at 3:45 pm #104006MemberMaurice Petterlin wrote:Darryl Vink wrote:My understanding is:

May 17, 2016 at 3:45 pm #104006MemberMaurice Petterlin wrote:Darryl Vink wrote:My understanding is:

– When you use the filter settings it provides the entire universe of symbols to run over

– When you use “IsIndexConstituent()” (from your HDBFilter) you are verifying the symbol exists in the filter list at that given dateJust setting the filter settings to Russell 1000 and Historical Constituents will include every symbol that has ever existed in the Russell 1000 over the entire period.

Hope that makes sense…

Sorry Darryl a bit confused..

Instead of the entire period, you mean that it includes the historical constituents for the dates tested. So if you exclude the HDBFilter you could be including stocks that weren’t part of the Index during your test period?

The video from http://edu.thechartist.com.au/guruTasks/7/41-section-2-module-18-full-system-coding-part-8-monte-carlo/284-historical-constituents.html shows the HDBFilter and filter = Russell 1000 Historical Constituents being selected.

I hope this will help

run this in the explorerCode:Filter = 1;

AddColumn(IIf(IsIndexConstituent(“$RUA”),1,0),”In Russell 1000″,1);here is the result of one symbol “A”

you will notice it is added to the index on 7/3/2000 so before this date the system should not take any trade in itMay 17, 2016 at 3:48 pm #104008MemberMaurice Petterlin wrote:Said Bitar wrote:@ Trenti tested 20 positions 5% per position from 2000 till 2016 my results are a bit far from yours, the number of trades is almost half

What are you using wrt trade size limits or other settings?

this will affect the trade size not the number

May 17, 2016 at 3:55 pm #104009MemberI restarted Amibroker and it is the same maybe i have additional filter

May 17, 2016 at 4:53 pm #104007InactiveMaurice Petterlin wrote:Darryl Vink wrote:My understanding is:

– When you use the filter settings it provides the entire universe of symbols to run over

– When you use “IsIndexConstituent()” (from your HDBFilter) you are verifying the symbol exists in the filter list at that given dateJust setting the filter settings to Russell 1000 and Historical Constituents will include every symbol that has ever existed in the Russell 1000 over the entire period.

Hope that makes sense…

Sorry Darryl a bit confused..

Instead of the entire period, you mean that it includes the historical constituents for the dates tested. So if you exclude the HDBFilter you could be including stocks that weren’t part of the Index during your test period?

The video from http://edu.thechartist.com.au/guruTasks/7/41-section-2-module-18-full-system-coding-part-8-monte-carlo/284-historical-constituents.html shows the HDBFilter and filter = Russell 1000 Historical Constituents being selected.

Having the filter settings with Russell 1000 and Historical Constituents

will include every symbol that ever went into (and possibly out again) the Russell 1000 at any time during your backtesting periodHaving IsIndexConstituent()

will ensure that the symbol was actually a part of the Russell 1000 at the given date.without running IsIndexConstituent() you are potentially backtesting symbols that went out of (or not yet part of) the Russell 1000 (or whatever is in your filter settings)

May 17, 2016 at 5:44 pm #103726StephaneFima

ParticipantGuys, you are too quick for me!

")

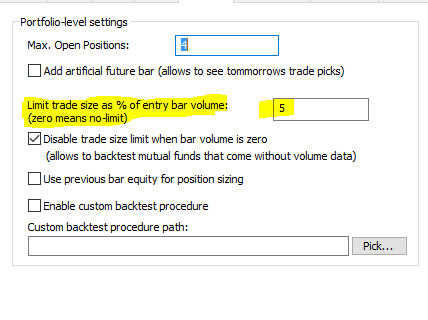

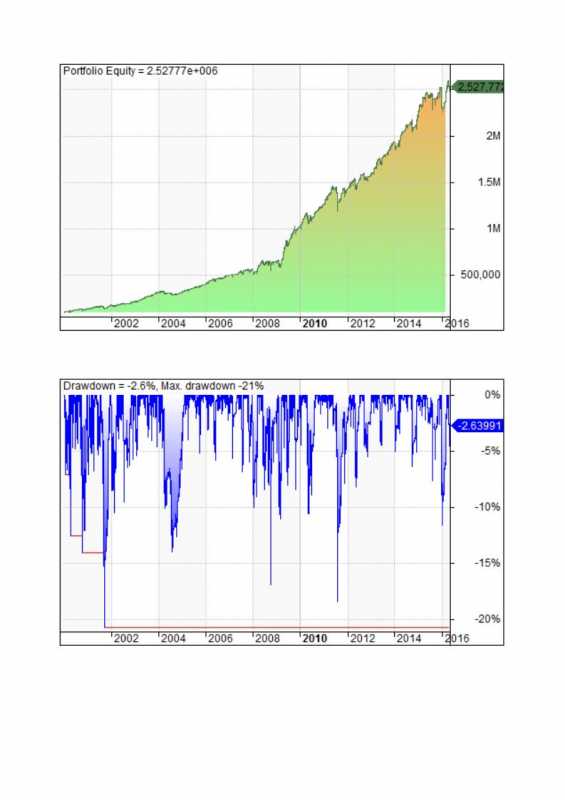

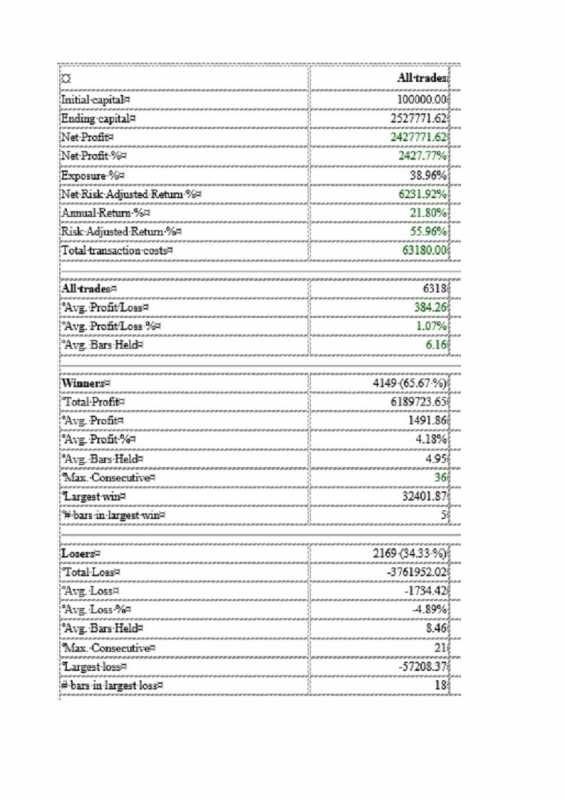

Here are my results based on :

– Russell 1000 from 01/01/00 to yesterday

– 100K portfolio

– Position size = 5% fixed

– Slippage and commission = $5 per trade May 17, 2016 at 5:45 pm #103727Participant

May 17, 2016 at 5:45 pm #103727Participant

-

AuthorPosts

- You must be logged in to reply to this topic.