Home › Forums › Trading System Mentor Course Community › Trading System Brainstorming › Group Collaboration System Ideas

- This topic is empty.

-

AuthorPosts

-

May 17, 2016 at 5:55 am #103985

TrentRothall

ParticipantMine are different again! haha

What are people/Nicks thoughts on testing systems pre 2000 in the US espically Mean reversion systems. The returns are so high compared to most years after that i feel it distorts the backtesting results. The way people operate in the market has changed a lot since then with internet/computer trading surely the market has changed a bit?

Is it better to focus on this century 2000-today?

May 17, 2016 at 6:39 am #103720Nick Radge

KeymasterPrior to 2000 there was no decimalization in US.

Always better to focus on more recent data in my opinion.

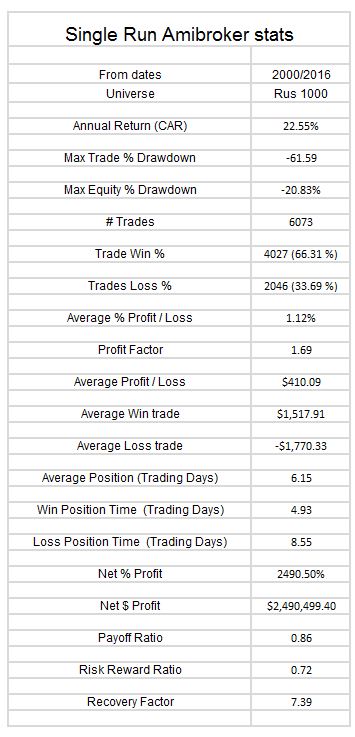

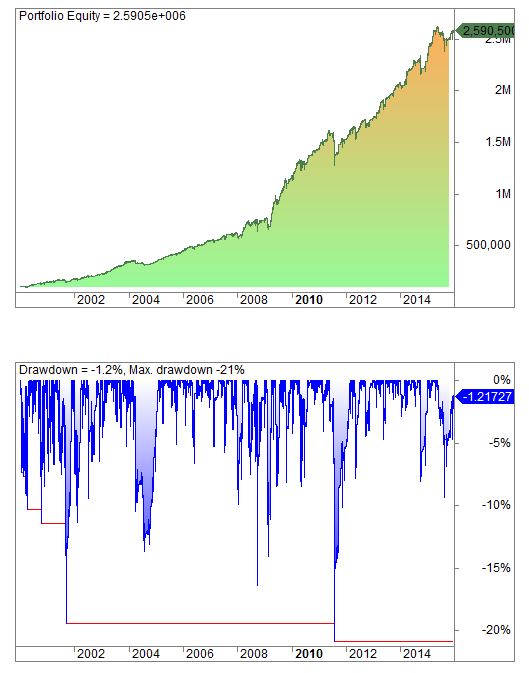

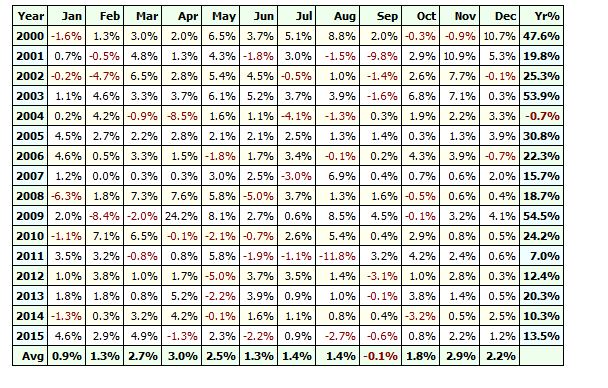

May 17, 2016 at 7:04 am #103721ParticipantThis is my results from 2000 – 2016

i used for the exit Close > MA(c,5) – exit next open

No leverage

May 17, 2016 at 8:03 am #103722

May 17, 2016 at 8:03 am #103722LeeDanello

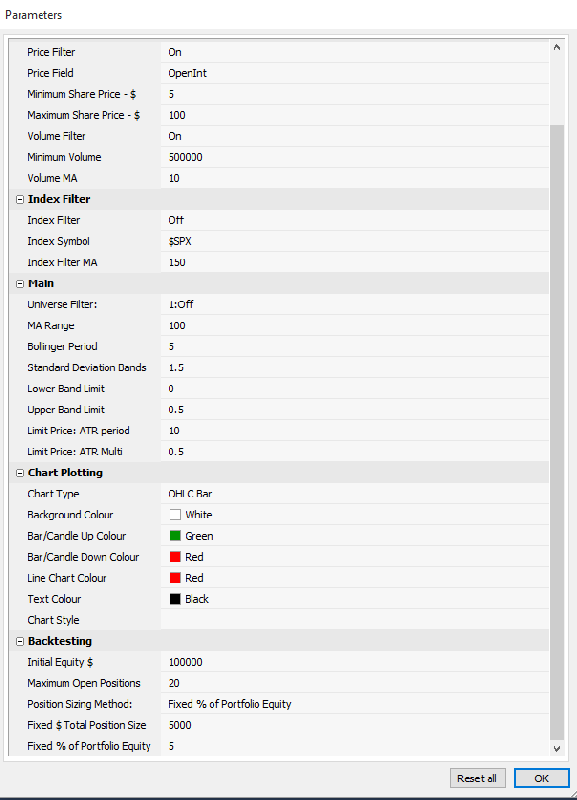

ParticipantTrent, These are my parameters

May 17, 2016 at 8:15 am #103989Participant

May 17, 2016 at 8:15 am #103989Participantwhat’s lower & upper band limit?

What’s your stats from 2000-1/1/16

May 17, 2016 at 8:28 am #103990ParticipantJust bollinger stuff. Sometimes I like to plot percentb as an indicator

Code:UpperBand = BBandTop( C, Periods, stddev );

LowerBand = BBandBot( C, Periods, stddev );

percentb = (C – LowerBand)/(UpperBand – LowerBand);/*

%b = (Price – Lower Band)/(Upper Band – Lower Band)

%b equals 1 when price is at the upper band

%b equals 0 when price is at the lower band

%b is above 1 when price is above the upper band

%b is below 0 when price is below the lower band

%b is above .50 when price is above the middle band (5-day SMA)

%b is below .50 when price is below the middle band (5-day SMA)

*/

lowerbandlimit = Param(“Lower Band Limit”,0.0,-0.5,0.5,0.1);

upperbandlimit = Param(“Upper Band Limit”,0.5,0,1.5,0.1);

BBWidth = (UpperBand – LowerBand)/ LowerBand *100;Code:percentb < lowerbandlimit;is the same as

Code:C < LowerBand01/01/2000 to 31/12/2015

May 17, 2016 at 9:51 am #103723Participant

May 17, 2016 at 9:51 am #103723ParticipantIs that with leverage?

How about we get on the same page with these rules. I believe they are the same as Said’s original ones.

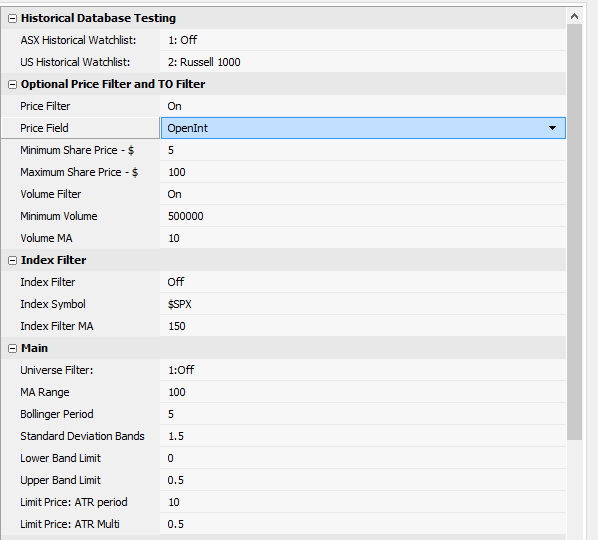

no leverage for now 20 positions @ 5%

V > 500k

No index filter

Rus 1000 from 1.1.2000 – 1.1.2016

C > 100 day MA

5 period bollinger bands with a width of 1.5 std dev

width between band needs to be > 5%

C < bottom band Buy on limit at L – (ATR(10*0.5)

sell on next open when C > 5 day MAMay 17, 2016 at 11:01 am #103724ScottMcNab

ParticipantBased on those rules Trent:

May 17, 2016 at 11:29 am #103991ParticipantThese are my entry and exit conditions – no margin

Code://====================================================================

//Entry and Exit Rules

//====================================================================

MArange = Param(“MA Range”,100,1,1000,1);

Periods = Param(“Bollinger Period”,5,1,100,1);

stddev = Param(“Standard Deviation Bands”,1.5,0,3,0.1);UpperBand = BBandTop( C, Periods, stddev );

LowerBand = BBandBot( C, Periods, stddev );

BBWidth = (UpperBand – LowerBand)/ LowerBand *100;

//——————————————————————–

//Limit Entry using the stretch

//——————————————————————–

ATRp = Param(“Limit Price: ATR period”,10,1,20,1);

ATRmulti = Param(“Limit Price: ATR Multi”,0.5,0,1.5,.1);

ATRVal = ATR(ATRp)*ATRmulti;

BuyLimP = L – ATRval; //stretch

TickLo = IIf(MarketID(0) == 10 OR MarketID(0) == 14 ,IIf(L<0.10,0.001,IIf(L<2.00,0.005,0.01)),0.01);

BuyLimVal = round(BuyLimP/TickLo);

BuyLim = BuyLimVal * TickLo; //stretchCond1 = C < LowerBand; //close below lower band Cond2 = C > MA(C,MArange);

Cond3 = VolFilt AND IndexUp AND UniverseFilter;

Cond4 = BBWidth > 5;OnLastTwoBarsOfDelistedSecurity = BarIndex() >= (LastValue(BarIndex()) -1) AND !IsNull(GetFnData(“DelistingDate”));

OnSecondLastBarOfDelistedSecurity = BarIndex() == (LastValue(BarIndex()) -1) AND !IsNull(GetFnData(“DelistingDate”));BuySetUp = Cond1 AND Cond2 AND Cond3 AND Cond4;

LE = Ref(BuySetUp,-1) AND L <= Ref(BuyLim,-1) AND NOT OnLastTwoBarsOfDelistedSecurity; LEPrice = Min(O,ref(BuyLim,-1)); LExPrice = O; SellSetUp = C > MA(C,Periods); //sell at middle band

LEx = Ref(SellSetUp,-1);May 17, 2016 at 12:58 pm #103981SaidBitar

MemberMaurice Petterlin wrote:sell – Close is above MA 5 days or crosses with MA 5 days?It is the same

May 17, 2016 at 1:05 pm #103993Member@Maurice I think the code is similar to mine but your results are way high for non leveraged

May 17, 2016 at 1:07 pm #103992Anonymous

InactiveMaurice Petterlin wrote:Code:Cond1 = C < LowerBand; //close below lower band Cond2 = C > MA(C,MArange);

Cond3 = VolFilt AND IndexUp AND UniverseFilter;

Cond4 = BBWidth > 5;Hi Maurice. Do your need to add something like “AND HDBFilter” into your “Cond3” ?

May 17, 2016 at 1:20 pm #103994ParticipantSaid Bitar wrote:Maurice Petterlin wrote:sell – Close is above MA 5 days or crosses with MA 5 days?It is the same

I don’t think so. Cross is only true at the point it crosses, Close is above MA 5 is always true as long as the close is above the MA

May 17, 2016 at 1:23 pm #103995ParticipantDarryl Vink wrote:Maurice Petterlin wrote:Code:Cond1 = C < LowerBand; //close below lower band Cond2 = C > MA(C,MArange);

Cond3 = VolFilt AND IndexUp AND UniverseFilter;

Cond4 = BBWidth > 5;Hi Maurice. Do your need to add something like “AND HDBFilter” into your “Cond3” ?

Darryl, you could be right, but shouldn’t change the results.

Here’s the code I usedCode:/*For the sake of getting started here is a swing trading strategy using BB.the rules are as follows:

No index Filter

Min average Volume is 500K

Close is above MA 100 days

BB (5,1.5)

Close below the lower band

BB width is greater than 5% (BBWidth = (BBTop – BBBot)/ BBBot *100;)

Buy on limit order if the price drops a bit under the low (0.5ATR(10))

Sell cross with MA 5days*/_SECTION_BEGIN( “Historical Database Testing” );

//====================================================================

//Historical Database Testing

//====================================================================ASXList = ParamList( “ASX Historical Watchlist:”, “1: Off|2: ASX 20|3: ASX 50|4: ASX 100|5: ASX 200|6: ASX 300|7: ASX All Ordinaries|8: ASX Small Ordinaries|9: ASX Emerging Companies|10: Excluding ASX 300|11: In XAO but Exc ASX 100|12: Exc XAO”, 0 );

HistDB = 1;//set to 1 to start

if( ASXList == “1: Off” ) HistDB = 1;

if( ASXList == “2: ASX 20” ) HistDB = IsIndexConstituent( “$XTL” );

if( ASXList == “3: ASX 50” ) HistDB = IsIndexConstituent( “$XFL” );

if( ASXList == “4: ASX 100” ) HistDB = IsIndexConstituent( “$XTO” );

if( ASXList == “5: ASX 200” ) HistDB = IsIndexConstituent( “$XJO” );

if( ASXList == “6: ASX 300” ) HistDB = IsIndexConstituent( “$XKO” );

if( ASXList == “7: ASX All Ordinaries” ) HistDB = IsIndexConstituent( “$XAO” );

if( ASXList == “8: ASX Small Ordinaries” ) HistDB = IsIndexConstituent( “$XKO” ) AND NOT IsIndexConstituent( “$XTO” );

if( ASXList == “9: ASX Emerging Companies” ) HistDB = IsIndexConstituent( “$XEC” );

if( ASXList == “10: Excluding ASX 300” ) HistDB = IsIndexConstituent( “$XKO” ) == 0;

if( ASXList == “11: In XAO but Exc ASX 100” ) HistDB = IsIndexConstituent( “$XAO” )AND NOT IsIndexConstituent( “$XTO” );

if( ASXList == “12: Exc XAO” ) HistDB = IsIndexConstituent( “$XAO” ) == 0;//———————————————————————————

USList = ParamList(“US Historical Watchlist:”,”1: Off|2: Russell 1000|3: Russell 2000|4: Russell 3000|5: NASDAQ 100|6: Dow Jones Industrial Average|7: S&P 500|8: S&P 100|9: S&P MidCap 400|10: S&P SmallCap 600|11: S&P 1500|12: Russell MicroCap|13: Russell MidCap”,0);

USHistDB = 1;//set to 1 to startif(USList == “1: Off”) USHistDB = 1;

if(USList == “2: Russell 1000”) USHistDB = IsIndexConstituent(“$RUI”);

if(USList == “3: Russell 2000”) USHistDB = IsIndexConstituent(“$RUT”);

if(USList == “4: Russell 3000”) USHistDB = IsIndexConstituent(“$RUA”);

if(USList == “5: NASDAQ 100”) USHistDB = IsIndexConstituent(“$NDX”);

if(USList == “6: Dow Jones Industrial Average”) USHistDB = IsIndexConstituent(“$DJI”);

if(USList == “7: S&P 500”) USHistDB = IsIndexConstituent(“$SPX”);

if(USList == “8: S&P 100”) USHistDB = IsIndexConstituent(“$OEX”);

if(USList == “9: S&P MidCap 400”) USHistDB = IsIndexConstituent(“$MID”);

if(USList == “10: S&P SmallCap 600”) USHistDB = IsIndexConstituent(“$SML”);

if(USList == “11: S&P 1500”) USHistDB = IsIndexConstituent(“$SP1500”);

if(USList == “12: Russell MicroCap”) USHistDB = IsIndexConstituent(“$RUMIC”);

if(USList == “13: Russell MidCap”) USHistDB = IsIndexConstituent(“$RMC”);//———————————————————————————

HDBFilter = HistDB AND USHistDB;

//====================================================================

_SECTION_END();_SECTION_BEGIN(“Optional Price Filter and TO Filter”);

//====================================================================

//Price and Volume Filters

//====================================================================

PriceTog = ParamToggle(“Price Filter”,”Off|On”,1);

PF = ParamField(“Price Field”,6);

MinSP = Param(“Minimum Share Price – $”,5,0.00,1000,0.01);

MaxSP = Param(“Maximum Share Price – $”,100,0.00,2000,0.01);

MinMaxSP = PF >= MinSP AND PF <= MaxSP; PriceFilt = IIf(PriceTog,MinMaxSP,1); //-------------------------------------------------------------------- VolTog = ParamToggle("Volume Filter","Off|On",1); MinVol = Param("Minimum Volume",500000,0,10000000,1000); VolMA = Param("Volume MA",10,1,200,1); AveVol = EMA(Volume,VolMA); VolFilter = AveVol > MinVol AND Volume > MinVol;

VolFilt = IIf(VolTog,VolFilter,1);

//——————————————————————–

OptFilt = PriceFilt AND VolFilt;

//====================================================================

_SECTION_END();_SECTION_BEGIN(“Index Filter”);

//====================================================================

//Index Filter

//====================================================================

IndexTog = ParamToggle(“Index Filter”,”On|Off”,1);

IndexCode = ParamStr(“Index Symbol”,”$SPX”);

Index = Foreign(IndexCode,”C”);

IndMA = Param(“Index Filter MA”,150,2,250,1);IndexFiltUp = Index > MA(Index,IndMA);

IndexUp = IIf(IndexTog,1,IndexFiltUp);

//====================================================================

_SECTION_END();//====================================================================

//Universe Filter

//====================================================================

List = Paramlist(“Universe Filter:”,”1:Off|2:Resources|3:Industrials”,0); //– this sets the drop down list

UniverseFilter = 1; //– set the filter to 1 to start

If (List == “1:Off”) UniverseFilter = 1;

If (List == “2:Resources”) UniverseFilter = InGics(“10”) OR InGics(“151040”);

If (List == “3:Industrials”) UniverseFilter = InGics(“10”)==0 OR InGics(“151040”)==0;

//====================================================================

_SECTION_END();//====================================================================

//Entry and Exit Rules

//====================================================================

MArange = Param(“MA Range”,100,1,1000,1);

Periods = Param(“Bollinger Period”,5,1,100,1);

stddev = Param(“Standard Deviation Bands”,1.5,0,3,0.1);UpperBand = BBandTop( C, Periods, stddev );

LowerBand = BBandBot( C, Periods, stddev );

percentb = (C – LowerBand)/(UpperBand – LowerBand);

BBWidth = (UpperBand – LowerBand)/ LowerBand *100;

/*

%b = (Price – Lower Band)/(Upper Band – Lower Band)

%b equals 1 when price is at the upper band

%b equals 0 when price is at the lower band

%b is above 1 when price is above the upper band

%b is below 0 when price is below the lower band

%b is above .50 when price is above the middle band (5-day SMA)

%b is below .50 when price is below the middle band (5-day SMA)

*/

lowerbandlimit = Param(“Lower Band Limit”,0.0,-0.5,0.5,0.1);

upperbandlimit = Param(“Upper Band Limit”,0.5,0,1.5,0.1);function ParamOptimize(pname,defaultval,minv,maxv,step)

{

return Optimize(pname,Param(pname,defaultval,minv,maxv,step),minv,maxv,step);

}

//——————————————————————–

//Limit Entry using the stretch

//——————————————————————–

ATRp = Param(“Limit Price: ATR period”,10,1,20,1);

ATRmulti = Param(“Limit Price: ATR Multi”,0.5,0,1.5,.1);

ATRVal = ATR(ATRp)*ATRmulti;

BuyLimP = L – ATRval; //stretch

TickLo = IIf(MarketID(0) == 10 OR MarketID(0) == 14 ,IIf(L<0.10,0.001,IIf(L<2.00,0.005,0.01)),0.01);

BuyLimVal = round(BuyLimP/TickLo);

BuyLim = BuyLimVal * TickLo; //stretchCond1 = percentb < lowerbandlimit; //close below lower band Cond2 = C > MA(C,MArange);

Cond3 = VolFilt AND IndexUp AND UniverseFilter;

Cond4 = BBWidth > 5;OnLastTwoBarsOfDelistedSecurity = BarIndex() >= (LastValue(BarIndex()) -1) AND !IsNull(GetFnData(“DelistingDate”));

OnSecondLastBarOfDelistedSecurity = BarIndex() == (LastValue(BarIndex()) -1) AND !IsNull(GetFnData(“DelistingDate”));BuySetUp = Cond1 AND Cond2 AND Cond3 AND Cond4;

LE = Ref(BuySetUp,-1) AND L <= Ref(BuyLim,-1) AND NOT OnLastTwoBarsOfDelistedSecurity; LEPrice = Min(O,ref(BuyLim,-1)); LExPrice = O; SellSetUp = percentb > upperbandlimit; //sell at middle band

LEx = Ref(SellSetUp,-1);

//——————————————————————–

//Stops

//——————————————————————–

Short = Cover = False;

//====================================================================

//Looping

//====================================================================

Buy = 0;

Sell = 0;

LPriceAtBuy = 0;

LBIT = 0;

//====================================================================

for( j = 1; j < BarCount; j++ ) { if( LPriceAtBuy == 0 AND LE[j] ) { Buy[j] = True; LPriceAtBuy = LEPrice[j]; BuyPrice[j] = LEPrice[j]; LBIT[j] = 1; if( LBIT[j] > 1 AND LEx[j] OR OnSecondLastBarOfDelistedSecurity[j] )

{

Sell[j] = True;

SellPrice[j] = LExPrice[j];

LPriceAtBuy = 0;

}

}else

if( LPriceAtBuy > 0 )

{

LBIT[j] = LBIT[j – 1] + 1;if( LBIT[j] > 1 AND LEx[j] OR OnSecondLastBarOfDelistedSecurity[j] )

{

Sell[j] = True;

SellPrice[j] = LExPrice[j];

LPriceAtBuy = 0;

}

}

}//====================================================================

LESetup = IIf(LBIT==0 OR Sell==1,BuySetUp,0); //Long Entry Set Up

LExSetup = IIf(LBIT>0 AND Sell==0,SellSetup,0); //Long Exit Set Up//——————————————————————–

Filter = Buy OR Sell OR LESetUp OR LExSetUp OR LBIT>0;

AddTextColumn(WriteIf(LESetup,”Buy Setup”,””),”Entry Signal”,1.2,colorDefault,IIf(LESetup,colorBrightGreen,colorDefault),130);

AddTextColumn(WriteIf(LExSetup,”Exit”,””),”Exit Signal”,1.2,colorDefault,IIf(LExSetup,colorRed,colorDefault),100);

AddTextColumn(WriteIf(Buy,”Buy”,””),”Today’s Entries”,1.2,colorDefault,IIf(Buy,colorGreen,colorDefault),130);

AddTextColumn(WriteIf(Sell,”Sell”,””),”Today’s Exits”,1.2,colorDefault,IIf(Sell,colorRed,colorDefault),130);

AddColumn(LBIT,”LBIT”,1.0);

SetSortColumns(-3,-4,-5,-6,1);/*Filter = 1;

AddColumn(BuySetUp,”Buy Setup”,1);

AddColumn(Buy,”Buy”,1);

AddColumn(SellSetUp, “Sell Setup”,1);

AddColumn(Sell,”Sell”,1);

*/

//====================================================================

//Interpretation Window

//====================================================================

//”Stop Level: “+NumToStr(StopLossExit,1.3);

“3 Lower Closes and below lower band: “+WriteIf(Cond1,”Yes”,”No”);

“Above long term MA: “+WriteIf(Cond2,”Yes”,”No”);

“Index Filer On: “+WriteIf(IndexTog,”No”,”Yes”);

“”;

“Bars In Trade: “+NumToStr(LBIT,1);

“Close above mid band: “+WriteIf(SellSetUp,”Yes”,”No”);

//====================================================================

_SECTION_BEGIN(“Chart Plotting”);

//====================================================================

SetChartOptions(0,chartShowArrows|chartShowDates);

_N(Title = StrFormat(“{{NAME}} – {{INTERVAL}} {{DATE}} Open %g, Hi %g, Lo %g, Close %g (%.1f%%) {{VALUES}}”, O, H, L, C, SelectedValue( ROC( C, 1 ) ) ));

ChartType = ParamList(“Chart Type”,”OHLC Bar|Candle|Line”,0);

SetChartBkColor(ParamColor(“Background Colour”,colorWhite));UpColour = ParamColor(“Bar/Candle Up Colour”,colorGreen);

DownColour = ParamColor(“Bar/Candle Down Colour”,colorRed);Colour1 = IIf(C > Ref(C,-1),UpColour,DownColour);

Colour2 = IIf(C > O,UpColour,DownColour);

Colour3 = ParamColor(“Line Chart Colour”,colorRed);

TextColour = ParamColor(“Text Colour”,colorBlack);if(ChartType == “OHLC Bar”) ChartOption = styleBar;

if(ChartType == “Candle”) ChartOption = styleCandle;

if(ChartType == “Line”) ChartOption = styleLine;if(ChartType == “OHLC Bar”) ColourOption = Colour1;

if(ChartType == “Candle”) ColourOption = Colour2;

if(ChartType == “Line”) ColourOption = Colour3;

//——————————————————————–

Plot(Close,”Close”,ColourOption,styleNoTitle|ChartOption|ParamStyle(“Chart Style”));

GraphXSpace = 10;PlotShapes(shapehollowUpArrow*LESetup,colorGreen,0,L,-40); //plots an arrow for a setup bar

PlotShapes(shapehollowdownArrow*LExSetup,colorRed,0,H,-40); //plots an arrow for an exit bar

PlotShapes(shapeHollowSmallSquare*Buy,TextColour,0,BuyPrice,0); //plots a small hollow square right at the buy price

PlotShapes(shapeHollowSmallSquare*Sell,TextColour,0,SellPrice,0); //plots a small hollow square right at the sell price

//——————————————————————–

FirstVisibleBar = Status(“FirstVisibleBar”);

LastVisibleBar = Status(“LastVisibleBar”);for( b = Firstvisiblebar; b <= Lastvisiblebar AND b < BarCount; b++) { if(Buy[b]) PlotText("n Buyn "+NumToStr(BuyPrice[b],1.3),b,BuyPrice[b]*0.9985,TextColour); else if(Sell[b]) PlotText("n Selln "+NumToStr(SellPrice[b],1.3),b,SellPrice[b]*0.9985, TextColour); } //==================================================================== _SECTION_END(); _SECTION_BEGIN("Backtesting"); //===================================================================== //options in automatic analysis settings //===================================================================== SetTradeDelays(0,0,0,0); SetOption("UsePrevBarEquityForPosSizing",True); Capital = Param("Initial Equity $",25000,1000,1000000,100); SetOption("InitialEquity",Capital); MaxPos = Param("Maximum Open Positions",10,1,100,1); SetOption("MaxOpenPositions",MaxPos); SetOption("AllowSameBarExit",False); SetOption("AllowPositionShrinking", False ); SetOption("InterestRate",0); SetOption("Minshares",1); //SetOption("CommissionMode",2); //Fixed Dollar Amount //SetOption("CommissionAmount",6); //Use IB commision rates Margin = Param("Margin",100,1,100,1); SetOption("AccountMargin",Margin); PositionScore = mtRandom(); //--------------------------------------------------------------------- ""; "Position Sizing Method:"; PosSizeMethod = ParamList("Position Sizing Method:","Fixed Fractional Risk %|Fixed $ Risk Amount|Fixed $ Total Position Size|Fixed % of Portfolio Equity",3); //Risk Calculation FDAmount = Param("Fixed $ Total Position Size",5000,100,100000,100); //Fixed % of Portfolio Equity FPAmount = Param("Fixed % of Portfolio Equity",10,1,100,1); if(PosSizeMethod == "Fixed Fractional Risk %") SetPositionSize(Risk1,spsPercentOfEquity); if(PosSizeMethod == "Fixed $ Risk Amount") SetPositionSize(Risk2,spsShares); if(PosSizeMethod == "Fixed $ Total Position Size") SetPositionSize(FDAmount,spsValue); if(PosSizeMethod == "Fixed % of Portfolio Equity") SetPositionSize(FPAmount,spsPercentOfEquity); //==================================================================== _SECTION_END();

May 17, 2016 at 1:29 pm #103996ParticipantDarryl Vink wrote:Maurice Petterlin wrote:Code:Cond1 = C < LowerBand; //close below lower band Cond2 = C > MA(C,MArange);

Cond3 = VolFilt AND IndexUp AND UniverseFilter;

Cond4 = BBWidth > 5;Hi Maurice. Do your need to add something like “AND HDBFilter” into your “Cond3” ?

Correct, It did change the results

I’m wondering why the results should be different if I turn HDBFilter off and use the inbuilt filter set to Russel 1000 historical constituents?

-

AuthorPosts

- You must be logged in to reply to this topic.