Home › Forums › Trading System Mentor Course Community › Trading System Brainstorming › Group Collaboration System Ideas

- This topic is empty.

-

AuthorPosts

-

June 15, 2016 at 9:48 am #103761

ScottMcNab

ParticipantNot sure if I could trade a single system with 10% position size…seriously doubt I would sleep at night….just know that I wouldn’t deal with the stress very well..would be checking market every 15 min…esp with a system that uses a buy limit entry….if it was one of a number of different systems then probably would

with 20 positions at 5%, it still has excellent metrics though….20% CAR with maxDD under 10% (assuming I having coded incorrectly) is impressive. I think back to the goals I submitted at the start of the course….if somebody had asked me if that was ok I would have jumped at it

June 15, 2016 at 9:59 am #104351Anonymous

InactiveSaid Bitar wrote:Darryl Vink wrote:Nick Radge wrote:600pxls wide are about as wide as you want. Anything over and the system tries to resize which causes the distortions.yes i tried resizing to 600pxls horizontal with aspect ratio maintained. the images are now too small though to see the detail. said’s images all seem large (around 1000 pxls it seems) and clear :huh:

I don’t attach the images I use photo bucket to insert the links to the forum

ok… good idea. thanks

June 15, 2016 at 9:59 am #104356LeeDanello

ParticipantDepends on your capital. If you don’t have much to start with ie less than 50k, I think it’s pretty pointless having 20 positions. I think with a high win rate, 10 positions is ok. Your system will make more with a higher drawdown but if you accept the testing as being Ok then why not.

June 15, 2016 at 10:39 am #103762ParticipantTrents comment on potential selection bias has me thinking if there is there a way to automate/code the number of new positions entered per day for a system like this one over a (eg) 10 year period.?..maybe making an exploration with only a “buy” filter and then sorting the results according to date, copying into an excel file….and then I’m lost….is there some way excel can then look through the date column and somehow tally/count the number of entries for each date? Anyone out there with some excel knowledge point me in right direction please

Might be simple ….will go and ask google…some of you may be doing this already ?

June 15, 2016 at 10:50 am #103763TrentRothall

Participantjust set number of positions to 500 or something with a $50000000 account then $1000 per position. Run a backtest and export to excel and can sort them easy then.

is that what your after?

June 15, 2016 at 10:56 am #104358Participantyep….just not sure how to get excel to count the number of buy entries for each day in the 10-20 year output

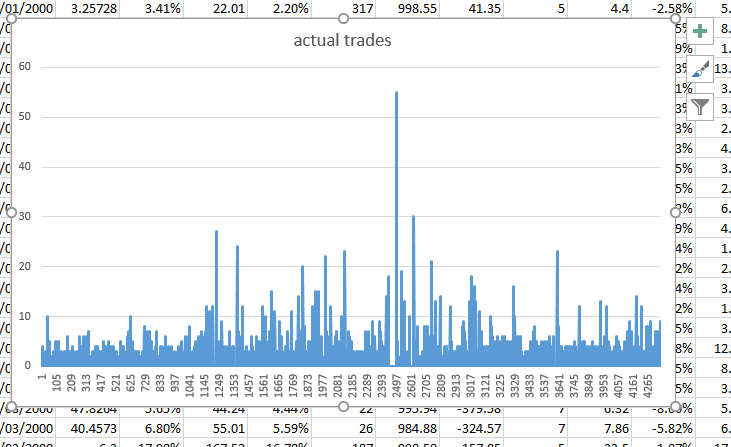

June 15, 2016 at 10:58 am #103764Participantaim is to create a histogram of average number of days with (eg) 10/20/30/40 buy orders etc so can quickly see visually what number of positions system really needs to be using to try and minimize selection bias

June 15, 2016 at 11:01 am #104357InactiveScott McNab wrote:Trents comment on potential selection bias has me thinking if there is there a way to automate/code the number of new positions entered per day for a system like this one over a (eg) 10 year period.?..maybe making an exploration with only a “buy” filter and then sorting the results according to date, copying into an excel file….and then I’m lost….is there some way excel can then look through the date column and somehow tally/count the number of entries for each date? Anyone out there with some excel knowledge point me in right direction pleaseMight be simple ….will go and ask google…some of you may be doing this already ?

hi scott. i made a post here the other day regarding that:

https://edu.thechartist.com.au/Forum/amibroker-coding-and-afl/121-generating-signal-order-plots.htmlits prettty simple.

place this code in your mcs script (somewhere after your LE or in my case i call it longEntrySetup. change it to match yours)

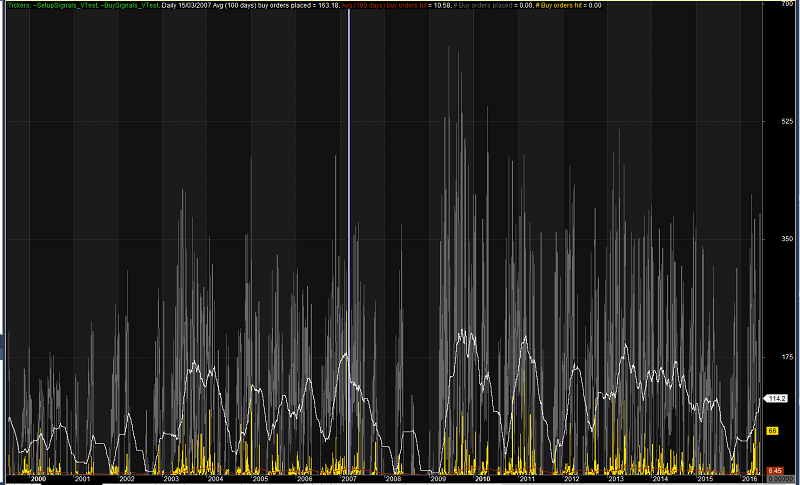

Code:// calculate the number of buy limit orders and potential buy orders we will be making

AddToComposite(longEntrySetup == 1,”~SetupSignals”,”X”,atcFlagDeleteValues|atcFlagEnableInBacktest);then do this from somewhere:

Code:Graph0 = Foreign(“~SetupSignals”,”C”);it works for me!

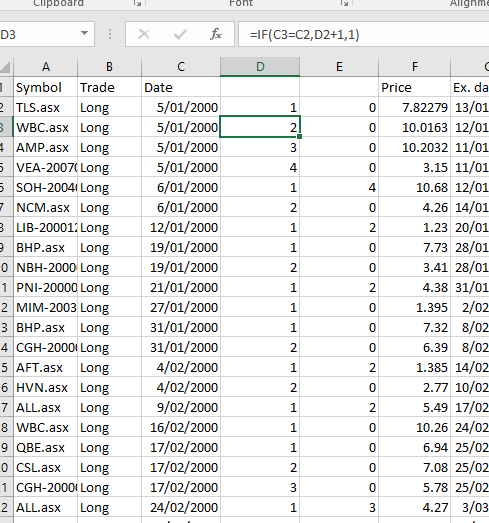

June 15, 2016 at 11:08 am #103765Participantrun a backtest like i mentioned then sort by entry date. copy everything then paste in excel.

then i insert some blank columns after the entry date in excel.

use the formula in the following clip to count entries on a certain day. You will need to put a 1 in cell D2 first to start the tally

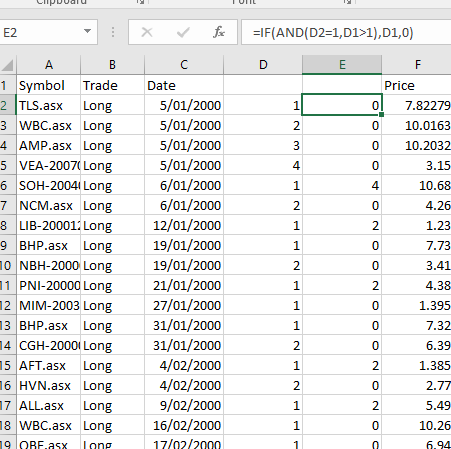

you can graph that but i add the next formula 9n another column to make the chart cleaner.

Hope that helps

June 15, 2016 at 11:11 am #103766ParticipantThanks Darryl…I read that post and thats probably what made me think of it….its simply changing it from looking at the LE/potential setups to the number of actual buy orders.

I will try it now.

June 15, 2016 at 11:13 am #103767ParticipantThanks Trent…that looks the goods too

June 15, 2016 at 11:13 am #104360ParticipantDarryl Vink wrote:Scott McNab wrote:Trents comment on potential selection bias has me thinking if there is there a way to automate/code the number of new positions entered per day for a system like this one over a (eg) 10 year period.?..maybe making an exploration with only a “buy” filter and then sorting the results according to date, copying into an excel file….and then I’m lost….is there some way excel can then look through the date column and somehow tally/count the number of entries for each date? Anyone out there with some excel knowledge point me in right direction pleaseMight be simple ….will go and ask google…some of you may be doing this already ?

hi scott. i made a post here the other day regarding that:

https://edu.thechartist.com.au/Forum/amibroker-coding-and-afl/121-generating-signal-order-plots.htmlits prettty simple.

place this code in your mcs script (somewhere after your LE or in my case i call it longEntrySetup. change it to match yours)

Code:// calculate the number of buy limit orders and potential buy orders we will be making

AddToComposite(longEntrySetup == 1,”~SetupSignals”,”X”,atcFlagDeleteValues|atcFlagEnableInBacktest);then do this from somewhere:

Code:Graph0 = Foreign(“~SetupSignals”,”C”);it works for me!

This is real good i reckon! A good visual!

June 15, 2016 at 11:23 am #104361Inactiveyep. you can also plot it against the potential trades taken (depending on maxpositions) with this

Code:AddToComposite(buy == 1,”~BuySignals”,”X”,atcFlagDeleteValues|atcFlagEnableInBacktest);June 15, 2016 at 11:59 am #104362Inactive

it looks like a lot of orders would need to be placed!

June 15, 2016 at 12:39 pm #104355InactiveTrent Rothall wrote:Yeah i thougt that if we made the setup conditions tighter, it may reduce some signls.

Will test tomorrowadding these settings/changes help a little by reducing the number of signals and still keep the system profitable:

Code:cond4 = RSI(2) < 40; cond5 = ADX(8) > 30;buyLimit = LinearReg(C,20) – 2*ATR(20)

-

AuthorPosts

- You must be logged in to reply to this topic.