Forums › Trading System Mentor Course Community › Trading System Brainstorming › Earn A Second Income Series

- This topic is empty.

-

AuthorPosts

-

January 24, 2016 at 5:57 am #101401

Nick Radge

Keymaster~~~

#1

‘Situational Irony’

~~~

New traders struggle to make a living from trading. I know because initially I did too and over the last 29 years I’ve watched hundreds of new traders struggle also.

It can be aggravating, frustrating and heart-wrenching. All at the same time.

So many people see the potential, yet do not know how to realize it.

For example I recently had a call from a guy who had never traded before. Here’s how the conversation went:

Nick: What are you trying to achieve?

Caller: By the end of the year I want to be a self-sustainable trader.

Nick: So you want to trade for a living?

Caller: Yes. I have $50,000 to start with.

Nick: Okay. What trading experience do you have?

Caller: None. I’ve never traded before.

Nick: Right. {thinking….}. Do you play golf?

Caller: What?

Nick: Do you play golf?

Caller: Yes {a little “WTF” inflection in his voice here}.

Nick: So, do you think you can join the US PGA tour by year-end and make living alongside Tiger?

Caller: No – of course not {brain ticking over…}.

Nick: Let me understand this. Even though you already play golf, you know you can’t make a living from it. Yet, at the same time, even though you’ve never traded before, you feel you can soon make a living from it?

Caller: Umm…

— End of call —

He can see the potential. He knows it’s there and many an expert will tell you there is money there. And to a large extent, those experts are right.

The money IS there. But there’s a catch and it’s a MAJOR one.

Let’s step back and agree that most want to trade for a living for the following reasons:

⇒ Work less / be your own boss / have free time to do what you want / retire early

⇒ Make loads of moneySo let’s talk about that catch. It’s called situational irony….

Situational irony is when actions have an effect that is opposite to what was intended, that is, the outcome is contrary to what was expected.

And trading for a living is full of them.

So, to help you build a foundation for trading success we need to discuss two such ironies before moving onto specific tactics.

January 24, 2016 at 5:58 am #102516Keymaster~~~

#2

‘Situational Irony – Working Less’

~~~

Above I stated that trading for a living is full of ironies, specifically one type known as situational irony.

To recap, situational irony is when actions have an effect that is opposite from what was intended, that is, the outcome is contrary to what was expected.

Today we’re going to talk about work ethic and the expectation that trading for a living will allow you to spend minimal time each day on the markets and spend the rest of your time swanning around on a beach or the golf course.

I have plenty of contacts that trade for a living, but many of these guys sprouted from the trading floor of the Sydney Futures Exchange where I spent several years. Their experience is beyond anything the average person in the street will be exposed to, so I phoned my friends at Aliom Trading Academy. Aliom is a proprietary trading company that offers a free 6-week trading incubator course; 2-weeks in a classroom followed by 4-weeks on the simulator using real time data.

If you’re a successful candidate you get to trade their money with no downside risk to yourself. The perfect trade!

But before you submit your resignation letter, consider this…

Aliom receives up to 1000 applications from individuals wanting to be part of the course and to ultimately become “Prop Traders”. Just 20 people are accepted. Of the 20, only a handful will go on to complete 12-months trading with the company’s money.

About a 1% success rate. Like any high performance pursuit, many are called, yet few are chosen.

But for the sake of this exercise let’s say you make that 1%.

What kind of personal attributes do Aliom look for?

Interestingly they look for entrepreneurial traits – dedication, deliberate practice, focus and persistence.

So let’s assume you have those traits – just like other small business owners.

Indeed that’s what Aliom hammers home – it’s a business just like any other.

Trading is no different to running a local bakery, for example. You need to be open as long as you can to take advantage of people walking past. You need to be up at the crack of dawn to bake the bread so it’s ready when those customers come through the door at 7am. You keep the shop open until customers stop, then you clean up, do the books and reordering then start again the next day.

The traders at Aliom start at 6.30am in their Sydney office (no, not at home or from the beach). The dealing room is dead quiet. All eyes on the screens. Watching numbers tick over. Tick. Tick. Tick. It reminds me of my years on the trading floor – the most exciting place to work when it was running fast, but like watching paint dry the other 90% of the day.

The Aliom traders finish at 6.30pm unless they decide to trade into the European session – which many will do.

The name of the game is being involved when the market is busy (like the bakery being open at peak times). A trader needs price movement in order to make profits, and some of the busiest periods are when US economic data is released. And you guessed it – the busy times for US data releases are usually between 11pm and 1am.

So you’ve done a 12-hour day which, more often than not was quiet, and now you’ve got to skip the pub with your mates to come back to the office at midnight to trade US volatility.

No beach. No pub. It really is like running any other business!

For those that do make it through, turning an average $60,000 wage kicks in at about 14-months. The term ‘wage’ needs to be used loosely – you only get paid if you make money. They make an investment in you – of about 12-months, but after that you need to consistently make a profit because your wage is a slice of that profit.

If markets are quiet, if volatility subsides, or you lose your feel of the market, then you’re expected to support yourself. Remember, no profit – no slice of the pie. As a result many candidates have a lower living threshold, i.e. still living at home with parents, or no dependents, a solid saving base to turn to or in some cases the traders have second jobs to keep them going during lean times.

Interestingly, of my many contacts that trade for a living, almost all of them have some kind of secondary business interest. They don’t necessarily work for someone else, but they run a side business that in many instances is not related to trading.

January 24, 2016 at 6:01 am #102517Keymaster~~~

#3

‘Situational Irony – Making More Money’

~~~

Today I’d like to discuss a classic example of situational irony, specifically whereby people tend to think there is more money to be made by electing to trade for a living.

But what do the numbers say?

To explore this we’ll run a basic experiment, however, in order to illustrate my point I have exaggerated the outcomes – so please don’t bombard me with emails pointing out the obvious.

Let’s look at the outcomes of three traders over a 10-year period. As you’ll see all three started with $100,000 in capital and have made excellent returns. I think it’s fair to say that any trader going +143%, +91%, +81%, +46%, +159% and +109% in their first 6-years has probably got ‘trading for a living’ tattooed across their forehead.

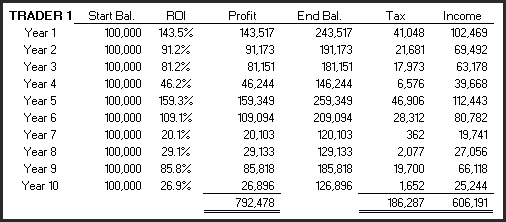

Trader 1

This trader typifies many I have come into contact with, specifically they remove all their profits for a year (or a month) and start again with the same balance. Unfortunately some of these also have a tendency to splurge during big winning years and fail to squirrel away funds for lean years. There is an argument for removing profits – so that losing years, or major drawdown periods, will be relatively congruent to winning years. For example, if I start with a capital base of $100,000 and make 50% in a year, keep profits as trading capital, and then have a 50% losing year, I’ll finish my second year of trading with $75,000, that is a negative year of 25%. Here’s how Trader 1 fares…

You can see in this example exactly why Aliom Trading Academy suggests having some savings in place for those lean years that come along – and they do come along for everyone at some stage. Even though this trader has had outstanding results, the annual salary is no better than the average wage. One wonders what the true hourly rate really is…

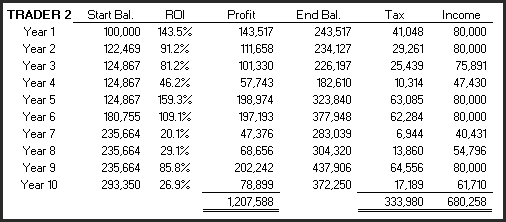

Trader 2

This trader takes a little bit more of a business approach deciding she can live on $80,000 but will also reinvest her excess profits back into the account to compound. Certainly sounds like a smart move. This has allowed some of the lower profit years to not be as lean as Trader 1 and over time she will certainly benefit from the ongoing compounding. Even so, for this 10-year period the annual salary is still just a little above the national average.

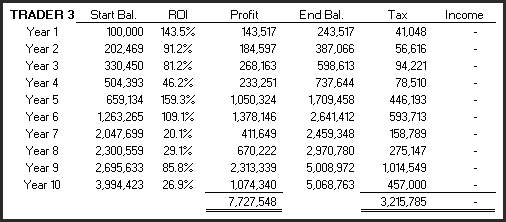

Trader 3

This trader is not caught up in the hype of trading for a living. Whilst he’s been able to generate solid returns using an end-of-day strategy he has been able to maintain his day job that he not only enjoys, but also offers a great social life as well. As he doesn’t need to live from his profits he duly reinvests them knowing that the compounding effect will be significant over time (and yes, liquidity/scale will limit the outcome).

Trader 3 has been able to create the same profit, yet in half the time – simply from the power of compounding. After an extended period, assuming one can scale to some degree – which we will cover later, Trader 3 has put himself not only into a very strong financial position, but has also done so with significantly less stress and worry. He hasn’t needed to dip into saving during lean years – his normal day job is his hedge.

The situational irony is that most people wanting to trade full time and for a living, tend to work long hours, potentially as long as a small business owner. And secondly, the need to withdraw profits, even after very successful periods of time, will dilute their absolute earning abilities. This example clearly shows that profits must not only cover expenses but also grow the account. Even Trader 2 operating under that principle, was still not making great leaps and bounds in financial gain.

In summary most aspiring to trade for a living do not have a capital base to be self-sustaining.

January 24, 2016 at 6:05 am #102518Keymaster~~~

#4

‘The Key To Consistency’

~~~

Most people prefer to take a small profit regularly than a lumpy profit sporadically. It’s not necessarily more profitable to do so, but it makes us feel better. It’s more comfortable.

There’s a big furore in the media at the moment about High Frequency Trading (HFT). It’s been stirred up by two events; the release of the Michael Lewis book, Flash Boys, and then the revelation by HFT firm Virtu that it’s had just 1 losing day in the last 1238.

The immediate and knee-jerk reaction is that Virtu is ripping the system off. The market is rigged to the benefit of the HFT firms. How is it remotely possible to just have a single losing day in five years?

Easy. It’s all in the mathematics, specifically the Law of Large Numbers.

Let’s first discuss the definition but then I’ll post some diagrams – that’s where the “aha!” moment will come.

By definition,

“The Law of Large Numbers “guarantees” stable long-term results for the averages of random events. For example, while a casino may lose money in a single spin of the roulette wheel, its earnings will tend towards a predictable percentage over a large number of spins. Any winning streak by a player will eventually be overcome by the parameters of the game. It is important to remember that it only applies (as the name indicates) when a large number of observations are considered.”

Most adults have been in a casino and had a winning hand or left the casino as a winner. However, as that only represents a single experience, it also represents a small and random sample. The Law of Large Numbers suggests the more often we went to the casino and the more we played, the more we’d start to lose.

The business of a casino is not really gambling. The name of the game (excuse the pun) is to entice people to play, after all, the more people play, the more the Law of Large Numbers works for the house. This is why many casinos offer big shows, cheap eats and, in many instances, allow free alcohol for punters.

This is now being pushed even further. In the Sydney casino, for example, many games are now run by computer – the croupier has been put out to pasture. Why? The croupier has to count money, distribute chips and be polite to patrons with chit chat. This all slows their dealing frequency which in turns slows the casino’s ability to exploit its edge. Less human intervention equals more money.

Let’s get back to trading, specifically how the Law of Large Numbers works with the HFT firms. It’s not a well known fact but many of these firms only have a trade win rate in the 50% – 60% range – really not much different to any other short term trader. But because they do so many trades, their number of winning days is extremely high – up around 90% for most, and for Virtus, almost 100%.

To really appreciate the simplicity of this, let’s do a simple exercise.

Trader 1

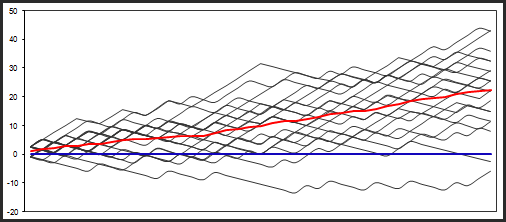

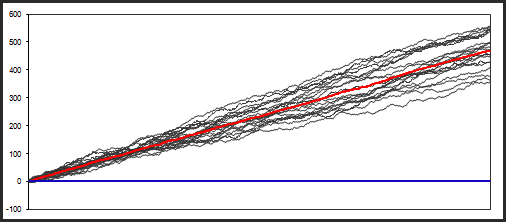

Let’s assume you’re a typical trend-following trader. Your winning percentage of trades is 45% and the win/loss ratio is 2.5. You therefore have a positive expectancy. As you follow trends that last 6 to 8 months you average 40 trades per year.The following chart is a random sample of 20 portfolios for the year – similar to a Monte Carlo simulation. The red line is the average of all 20 portfolios, and as you can see it finishes the year on average above the zero line (blue).

However, you can also see that 2 of the 20 portfolios finish below the zero line at years end. Due to the positive expectancy we know this strategy can’t fail over the longer term. However, in shorter timeframes, as shown above, there can be losing periods and there will be losing years. If you’re unlucky your account could spend an entire year below a prior equity peak. Take a look at almost all traditional fund managers, from Warren Buffet down, and you’ll see they not only have losing years but the ability to recover from a losing year can be slow and their equity can remain below a prior peak for some time.

Trader 2

This trader has the same trade statistics, that is, she has a 45% winning percentage of trades with the average win/loss of 2.5. The difference is that she makes 800 trades a year rather than the 40 that Trader 1 does. What impact does this added trade frequency have?

Even though the win rate is just 45%, it’s impossible for Trader 2 to have a losing year, indeed you can see that whilst losing months and moderate dips in equity do occur, those losses are recovered very quickly. Trader 2 has achieved a very high level of consistency simply through increasing trade frequency and taking advantage of the Law of Large Numbers – exactly the same as a casino and exactly the same as the HFT firms. Our very own adaptation of this theme, the US High Frequency Strategy¹, uses these exact principles.

Yet here’s the conundrum; Trader 2 needs to find 800 trades a year. You can’t do 800 trades if you hold a position for 6 to 8 months. You need to lower the holding time to a minimum. Professional day traders, or scalpers, for example will do 100+ trades a day but they sit there all day – which is not what we want to do. HFT firms will do thousands of trades a day yet they have access to advanced technology to do so.

Lowering the hold time presents a number of problems:

(1) It’s highly unlikely that the win/loss ratio of 2.5 can be maintained on such small intervals. This means the 45% win rate will actually generate a negative expectancy. So how do you skew the numbers back?

(2) How do you find 800 opportunities?

(3) 800 trades will dramatically increase commission drag. How do I overcome this?

(4) How does someone with a full time job manage so much trading?January 24, 2016 at 6:10 am #102519Keymaster~~~

#5

‘The Expectancy Curve’

~~~

A trend follower that holds for 6 – 8 months easily creates an edge simply because the winners will outweigh the losers by a considerable margin. In our prior example the win/loss ratio was 2.5, meaning the average win was 2.5x the average loss. However, we were shown that to gain a higher trade frequency (required to be consistent), we had to lower the holding period from 6 – 8 months right down to a much shorter period. With more trades being better than less, we’re talking holding periods in days, not weeks or months.

Yet here’s the dilemma; the lower the hold period the less distance the market can move and therefore the less profit that can be derived from each trade. A market can move a long way in 6 – 8 months, but rarely will it move the same distance in just a few days. If we only hold for a few days the win/loss ratio must also decline. Therefore if our winning percentage of trades is too low, we go from a positive expectancy (making money) to a negative expectancy (losing money).

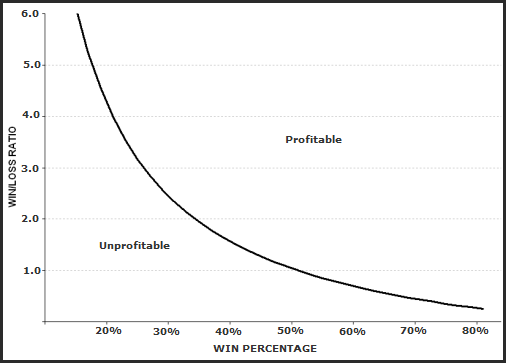

Expectancy is made up of two inputs; the winning percentage of trades and the win/loss ratio. The immutable law with expectancy is that the higher the winning percentage of trades, the lower the win/loss ratio, and the lower the winning percentage of trades, the higher the win/loss ratio. I created the expectancy curve diagram in 2005 to show this phenomenon:

As much as we want a strategy with a very high winning percentage of trades AND a high win/loss ratio, it simply doesn’t exist – at least not that I have seen without some significant amount of curve fitting or optimization. There are many examples of this phenomenon in trading literature. For example, in Unholy Grails, where we tested numerous different trend following systems, all of which offered a winning percentage of trades between 40% and 50% and a win/loss ratio anywhere from 2.0 through to 4.0. These are typical for longer term methods. Then, on the other end of the spectrum, Larry Williams wrote “Long Term Secrets To Short Term Trading”, showing numerous setups with very high winning percentages, some as high as 90%, but in every case, the win/loss ratio is less than 1.0, and in some instances as low as 0.50.

This validates the theory that the shorter the time you hold a trade, the less profit you can materially make. As such, you need to become more reliant on a higher winning percentage of trades to compensate and get you back over the expectancy curve.

Finding a high winning percentage strategy does not appear to be that difficult. The Willliams’ book lists numerous setups traded on the S&P 500 futures contracts with win rates exceeding 75%. Howard Bandy has released a book on Mean Reversion trading and discusses a specific strategy that has a winning rate of 80%.

Whilst both these look promising on the surface, there are two significant underlying issues. Firstly, neither generates enough trades to meet our higher frequency requirement, unless the strategies are traded on a broader and more extensive universe – which then leads to problem two. Both these authors have extensively data mined, curve fitted or optimised these systems in order to achieve these very high readings (high win rate systems sell more books). As such, neither are deemed robust enough and the logic will fail to transfer to any other instruments or symbols.

However, it’s not all bad news. Before you spend every day and night over the next 3 years trying to find a strategy with an 80% win rate, consider these two facts:

(1) The major games at casinos – poker, blackjack, bingo, baccarat, and sports book, all have an edge of less than 3% The billions banked by the Las Vegas casinos don’t get amassed in large tranches. They’re amassed by taking little nibbles around the clock. In a study (Manchanda & Mok Park) of a private gambling database exceeding 18,000 people showed a perfect example: Gambler #1357078, a 56yo Swiss man played for a 3-week period with an average bet of just $9. However, he made 1000 bets a day, losing on 84% of those days, and eventually lost $110,000 in his 3-week foray. Rather than one large plunge, it was the small edge taken by the casino coupled with the Law of Large Numbers that did the damage.

(2) Also consider Tradeworx, a mid-tier High Frequency Trading firm in the US that accounts for 1% of the daily volume on the New York Stock Exchange. In a recent interview, Manoj Narang, the firm’s founder, explained, “…because we make many trades in a day, our winning percentage of days is around 86% and winning weeks is over 99%. However, our winning percentage, on a per-trade basis, is in the low 50’s, in other words, barely better than a coin flip”.

Now that’s a startling comment.

Both these examples show that rather than spending your time looking for the absolute highest winning percentage strategy, instead, look for one in the 50% to 60% range, then ensure you do a lot of trading to get the large numbers working for you.

How?

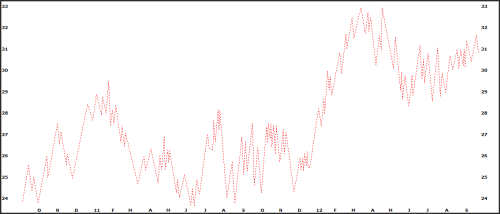

Markets tend to oscillate more than they trend – the following chart of $MSFT highlights this quite well. The stock does show a decent trend for 3-months from $25 to $33, but for the other 21-months it gyrates in choppy sideways ranges. What we want to do is try and ride these small ranges up and down as many times as we can as these offer more opportunity than trying to catch one single trend.

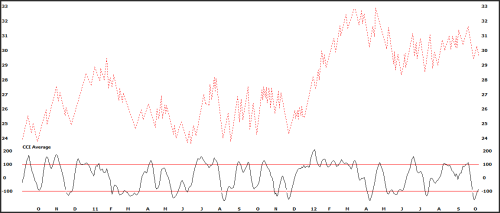

Therefore, using an oscillator, such as an Relative Strength Index (RSI) as Bandy did in the above test, or a Commodity Channel Index (CCI) or some other type, we can better view those back and forth ranges. Ensure you set the look back period to about 5 days to match our wanted shorter time frame. Here’s the same $MSFT chart with a 5-day CCI added. This tends to take much of the smaller noise out of the picture. It also shows over extension points that, just like an over-extended rubber band, may reverse back the opposite way. We want to try and buy and sell around these over extensions.

Here’s some recent trades I made within our very own High Frequency Strategy¹.

All these trades are quick bites of the cherry. Small nibbles. In and out. Recycling capital, reducing exposure and allowing a new trade to be taken.

January 24, 2016 at 6:19 am #102520Keymaster~~~

#6

‘More on Entries & Exits’

~~~

Here are a few more ideas that you can pursue…

1. Find overbought/oversold points using technical oscillators, such as the RSI or CCI

2. Find overbought/oversold levels using Bollinger/Keltner Bands

3. Find extended price moves using sequential up/down days, i.e. how likely is it for price to reverse after 5 consecutive up/down closes

4. Find extended price moves using daily percentage moves, i.e. if the close is 2% higher than the day’s open, how likely is it that price will reverse the following day

5. Find extended price moves using volatility, specifically average true ranges

6. Find extended price moves using gaps, specifically from high/low to the next openAs you can see there are many ways to investigate price areas that have been potentially over-extended in the short term and tending toward some kind of reversal. Unlike much found on the internet, our experience and modelling shows that rather than using a single measure, combining two technical leads in confluence, tends to help the risk adjusted returns. For example:

1. If the close is higher on 5 consecutive days AND on day 5 it gaps higher, then what are the chances of it reversing?

2. If the close is less than a Bollinger band AND the RSI is at an extremely oversold point, what are the chances of prices reversing higher?

3. If prices rise 2% from days open to close AND gap up the next day, what are the chances of prices reversing lower?

4. If price makes its highest high point in 10 days AND the CCI is at extreme levels, what are the chances of it reversing?Many professional scalpers tend to focus on the exit, not so much because of the exit itself, but more to lock in a small profit at every opportunity. This does a number of things; it enables capital to be turned over quicker and it also reduces market exposure. When a quick profit is not an option they’ll tend to try and ‘scratch’ the trade, meaning they try and sell at the same price at which they bought to create a breakeven trade. They do everything not to have a loss. As a result they tend to have many scratch trades (up to 50%) during the day, minimal losing trades and some winners to get ahead. This takes a lot of work and screen time – something we can’t do being end of day traders.

As a result we tend not to have many scratch trades. Rather, we get mostly winners and losers. This means that the exit becomes quite important. One of the most influential exit techniques I have come across, and one that works extremely well, is the Larry Williams “first profitable open” method. It basically exits any position as soon as an open print makes the position profitable. This may be effective, but it still means you have to be screen watching to implement it.

Here are some ideas to quickly exit a trade:

– Time based, i.e. exit the position after 1 or 2 days regardless of P&L

– Sequential, i.e. exit the position after 1 or 2 closes in the desired direction regardless of P&L

– Objective, i.e. use a tight price target

– Reversion, i.e. prices return to a median level such as a moving averageOur experience and simulations suggest all of these are extremely useful but we lean towards the Time Based and Sequential methods.

January 24, 2016 at 6:23 am #102521Keymaster~~~

#7

‘Selecting A Universe To Trade’

~~~

If having a high trade frequency is key, then the next step is finding opportunities to trade. When researching mean reversion systems on the web, or higher winning systems, you’ll find most examples focus on a single symbol, such as a big futures contract, e.g. Larry Williams (S&P 500) or a large ETF, e.g. Howard Bandy ($SPY). Even if we assume the patterns can transfer across to other like-for-like symbols, there will still be a lack of opportunities. There are only about 50 futures contracts and many ETF’s are illiquid.

We need to go bigger. We need to trade a large universe of individual stocks.

If you’re thinking about the Australian stock market, then I’ll make you aware of something right now; this style of trading will make your broker a lot more money than you’ll make, or at the least a very disproportionate amount.

One of the key reasons why High Frequency traders are able to do so much trading is that they pay extremely low commissions and get some nice volume rebates back from the exchanges. Even the traders that become successful at the Aliom Trading Academy get refunded some of their trading expenses (by the exchange) depending on the quantity of trading done.

Trading the Australian stock market is very expensive, both in terms of commissions and slippage.

Most will charge $10 per transaction. Doing 800 completed trades (buy and sell) a year will cost $16,000 in commissions.

Now compare this to the US market where commission is $1 per trade or $0.005 per share (I use Interactive Brokers). The same amount of transactions will cost just $1,600. Not only is this a direct cost saving, it also lowers the barrier to entry. A trader with a starting capital of $100,000 will need to make 16% just to breakeven if trading the Australian market, whereas doing the same in the US market requires just a 1.6% gain to breakeven. So trading in the US market at $1 per trade will allow a $30,000 account to get up and running without being overly concerned about drag working against them.

Who do you think will have the most success?

It doesn’t stop there. Slippage is defined as the distance between where you want to buy/sell and where you actually buy/sell in the market. This is also deemed a cost, more so for shorter term traders, indeed, the shorter your time frame the higher the cost of slippage (remember that the market can only move so far in smaller time frames).

The US markets are substantially more liquid than Australia and the greater the liquidity the less the slippage. I recently reconstructed 3-years worth of my own trading here in Australia and found slippage was costing me $92 per trade and that this was evenly spaced out over the 3-year period. So not only was I paying a higher commission, I was also paying away profits because liquidity never allowed me to buy and sell at my wanted prices. I use LIMIT prices on entry to minimise slippage as much as I can.

Lastly – opportunity. There are significantly more liquid stocks in the US market than there are in Australia. I personally only trade the S&P 500 constituents which contain some of the largest and most heavily traded companies in the world. If I ran our High Frequency strategy on a larger universe, such as the Russell 1000, returns increase simply because of greater opportunity.

Opportunity = Frequency = Profits.

Whilst this makes intuitive sense it’s a hard transition to make for many traders used to trading one market, such as Australia. It’s both a comfort and laziness issue (similar to people who can’t be bothered moving their mortgage to a cheaper bank – even though the short term pain of some paperwork will make huge cost savings over the longer term). Regarding comfort – at the end of the day we’re not worried about what the company does, where it’s located or whether or not they’re domiciled in our own country. We’re just playing a numbers game. We don’t have to sit up and watch the market through the night. Technology allows us to make life, and trading, much simpler.

January 24, 2016 at 6:29 am #102522Keymaster~~~

#8

‘Setting A Benchmark’

~~~

.Let’s put all the pieces together now and set a benchmark from which you can work from. We’ll take some of the entry and exit ideas from tutorial #6, incorporate our wanted trade frequency, a larger universe of stocks and the lower commission rates. Here’s an example strategy:

Long Entry

Close > 100-day moving average [ensure long term up trend is in place]

Close < 5-day moving average [ensure short term weakness is in place]

3 consecutive lower lows [sequential weakness confirmed]Set a limit buy order for the next day if price falls another 0.5 x 10-day average true range.

Long Exit

If the close is greater than the prior close, then exit the position on the next day’s open.Short Entry

Close < 100-day moving average [ensure long term down trend is in place]

Close > 5-day moving average [ensure short term strength is in place]

3 consecutive higher highs [sequential strength confirmed]Set a limit sell order for the next day if price rises another 0.5 x 10-day average true range.

Short Exit

If the close is less than the prior close, then exit the position on the next day’s open.In summary this strategy looks to buy a 3-day dip below a 5-day moving average if the longer term trend is up, or, looks to sell a 3-day rally above a 5-day moving average if the longer term trend is down. You can see that we’ve used quite generic inputs, i.e. we haven’t optimised, data mined or curve fitted. Every stock is traded the exact same way, as are entries on the long side being the same as entries on the short side. Are there more optimal parameters? Quite possibly, but that’s beyond the scope of this email series.

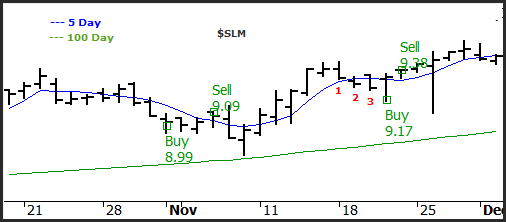

The following chart of SLM Corp ($SLM) shows several buy signals based on these rules. Three lower lows take price below the 5-day moving average, but remain above the 100-day. The following day any further weakness will trigger a buy level. An exit will occur on the open following the first positive close. As you can see in both these examples, we’re holding for 2 to 4 days.

Let’s now put the strategy to the test using the following variables:

Start Balance: $100,000

Start Date: January 1995

Universe: Russell 1000 (inclusive of all historical and delisted securities to alleviate survivorship bias)

Minimum Daily Volume: 500,000 shares

# Positions: 20

Allocation per position: 10% of capital

Leverage: 50%

Commission: Interactive Brokers standard

Over the last 19 years this basic strategy has had no losing years and shown 68% winning months. This is a little on the low side for my liking and some months have been quite volatile – a little stomach churning for the average trader. Other stats:

CAGR: 50.3%

Trades: 20,576 (11,166 long trades / 9,410 short trades)

Win%: 61.1%

W/L: 0.83

MaxDD: -30.8%In my experience I’d suggest not many people would be able to trade a strategy with a 30% drawdown, regardless of the upside returns. Secondly, one picture not shown here is the inconsistency of the short side trades. Removing 2008 from the data portends trading on the short side has not really been worth the effort, but 2008 itself was a bumper year, albeit an aberration.

Can this basic strategy be improved? Some suggestions for you:

(1) Use an Index Filter (as described in Unholy Grails) so you align your entries with the broader market trend.

(2) Trade ‘long only’. The contribution from the short side in this system is not worthy of a standalone system – so leave it out.

(3) Add in volatility parameters.

(4) Add additional ‘stretch’ to the entry. -

AuthorPosts

- You must be logged in to reply to this topic.