Home › Forums › Trading System Mentor Course Community › Progress Journal › Dustin’s Journal

- This topic is empty.

-

AuthorPosts

-

December 4, 2019 at 8:31 am #110660

SaidBitar

MemberI didn’t use index constituents for the Intra-day testing it was more like validating an idea, i know it is not accurate but since it was day trading system i didn’t care much.

regarding machine learning i never tested or even thought about using it since i feel it is leaning towards curve fitting.June 6, 2020 at 10:34 am #109459Anonymous

InactiveHi guys,

I wanted to write a question to Matthew O’Keefe but I don’t think he has his own progress journal.

Matthew, I notice your post on twitter regarding your short strategy performance yesterday. It seems like you are running an MOC strategy using lots of potential entry trades?

Would you be willing to share the longer term trade stats for your strategy? I have really tried to develop a short strategy along these lines and have basically given up. You seem to have found something that works though so it isn’t impossible! Would love to see how this has performed longer term.

Thanks!

Dustin

June 7, 2020 at 2:06 am #111598InactiveHi Dustin,

Thanks for seeking out my comment on my twitter post. I am humbled that you would want my advice/info.

Also just let me apologise for not running a Progress Journal here on the forum. As I started my trading journey a few years ago and as I grow and learn with my trading I have felt it a good idea to hone my skills first before running a journal that shares with others about my experience or give advice. I guess you could say I wanted to become something of a good performer before I go to the olympics and show the world my skills on the open stage.

I know the journal is a tool to help me no matter how good I am, learner or professional, however my personal traits are that sometimes I don’t do well with criticism or that I get demotivated easily if shot down too many times. So for this reason I have been holding back on creating my journal thinking that I’m “not good enough” to be sharing garbage opinions or performance. The good news though is that I think I am breaking through some of my old habits/traits and think I am starting to get somewhere as a trader. All I can say in this regard is that it is totally true when experienced traders say “the early years are for learning, you won’t make any money” and probably even lose money in these early years. I was naive to think I could do the mentor course and instantly become a gun trader. I completed the course around two years ago and only now do I think I am making breakthroughs in my trading to the point that I would proudly call myself a “trader”. So the future is nigh on my journal.

OK about my MOC system….

Yes I do run the MOC system in both long and short modes. I split each side into two portions for different constituents, so its:

RUI Long 80 Positions

RUT Long 160 Positions

RUI Short 50 Positions

RUT Short 80 PositionsWhy these number of positions? I am using leverage on this system. If you aren’t using leverage I would say that you would need less positions than this because too many positions on no leverage isn’t going to produce good results. So you need to find the right balance. I would probably say on the RUI long at 80 positions on leverage it would probably run well at say 20 positions well without leverage, however that is just a guess. Don’t get too lost on exactly how many positions. 8 positions versus 9 positions isn’t going to make a pinch of difference, so just get it somewhere in the correct ballpark and that will be good enough. I found my positions numbers through the backtesting/optimisation process. More positions the returns/dd would slowly drop off. Any less positions and 15 year monte carlo showed getting too close to ruin. Could I use 70 positions instead of 80 on my RUI Long? Sure, even 60 would work, but the chance of ruin gets close to 1% o 5% and that is too much possibility for me. The lesson here is about risk management and finding the right balance between returns and no chance of heavy drawdown or ruin over the long term. If you are using 4x leverage and have 60 positions that is the same as 15 positions for each 100% of your capital, or 6.66% per position. If you assume a potential 15% worst drawdown on any single position that is about 1% risk (or 1R risk). That is about the limit of what you should be doing for long term sustainability in my opinion. If you want to know more about risk, read Van Tharpe “Trade your way to financial freedom”.

Given I am running the four systems with a maximum of 370 positions across all four, it is no wonder that sometimes I can get a lot of fills on some of the heavily ranging days. And because I am running on both a long and short method, it also generally means that one of the directions is where I get the most fills for the day given the market mostly moves in one direction for the day most of the time. Maybe today is good for the short side, maybe it is good for the long side, however having both systems running at the same time gives me peace of mind that if I’m wrong on one direction I might be right on the other. I usually do get fills in both directions, but generally speaking usually more fills in one direction than the other. On the slow days overall across all strategies I might get 5 to 10 fills. On regular days about 15 to 30 fills. Heavy days about 50 fills and on the “load the boat” days perhaps 100 to 150 fills.

For example on yesterday’s fun day, I had a full load of 130 short orders sitting in the API and I got 105 fills. That is a record fill rate for me on the short side. I also had a full load of long orders in the API but only got 5 fills for the day. The market yesterday actually opened with a gap up and then trickled down to a close which was lower than the open. That is truly the perfect scenario for this type of system on the short side. Alternatively, you could imagine the same but opposite to be true when running it long, with a gap down on the open which would slowly trickle up to a close higher than the open for the day. A gap on the open combined with a move in my favour, a v shape, a Nike swoosh shape or whatever you want to call it (plus these shapes then flipped upside down for the short side) is what works for this system.

For how the strategy works/operates, I would like to keep some of my secret sauce to myself, however it is not excessively complicated. It does use the custom backtester code that Julian was so generous to share with all of us, however I have modified it to work on the short side (out of the box it only worked on the long side because it had code such as is.entry when in fact it is required in my situation to use is.long or is.short to ensure the code is trapping the correct symbols to exclude for long/short trading). If you do a little work on modifying the code to have it run short you will eventually find it works well on the short side. Don’t panic, there are only a few things to change in the code to make it work short.

For the general parameters or how it works, it is no real black magic to report. It is using a very minimal number of hurdles to jump. I’m talking very basic things too, like moving averages or ATR or simple things like this. Don’t get lost in trying to layer an ADX14 below 20 with an RSI cross above 30 and confirmed by the MACD. If you start layering all manner of garbage like this you will end up with no signals and something too finely tuned to the point of never working in the future. Keeping it very basic is an important feature of the success of systems like this to ensure a large number of trades over a period of time so your edge can play out with the law of large numbers. I cannot emphasize enough the importance of understanding expectancy, probability etc.

In developing this system you should also know that it is also not perfect and has come with a fair load of stress with it. Prior to the Feb/March rout I actually stopped trading it in the middle of Feb because it was too stressful thinking I was putting in short side orders when it seemed the market was going nowhere but up.

During March/April I decided to take a time out from trading it and use the downtime to hone my skills, improve myself, the system etc. In this time I read over ten books, did plenty of backtesting and trying new ideas. I am lucky enough that I could literally spend all day every day for these months trying to improve myself and the system. Only through this process did I have a few breakthrough moments in my ideas on how to attack this system. I got to the point where I realised I had to drop the complexity on the entry conditions with indicators and get back to basics on how price moves each day in the market and trying to identify reversals. Some would call these Mean Reversion strategies and I guess you can call it this, however I personally think this is a bit of misnomer because ultimately I am not really interested in seeing a reversion from the mean, all I am really interested in is being able to identify how a price might move within one trading day outside of a usual range. Whether it is with the trend or against the trend I don’t really care about. I am interested in finding price behaviour that tells me how a price move today (or recently) might play out tomorrow only, given what has happened today or last few days. Sometimes that is a continuation of the same trend tomorrow given the small hiccup in the trend today, or perhaps it is a reversal of the trend tomorrow given the small hiccup in the trend today. So scrub up on your reversal patterns, multiple days with higher highs or lower lows, up closes, down closes, heavily ranging days, lightly ranging days. How a weird/strange movement yesterday did to a movement today.

Another feature I added for peace of mind is a very mild index volatility filter. One which only in the very extreme situations like in late Feb and March would it tell me to stop trading. Whilst systems like this thrive on volatility, they also can be really quite damaging and stressful during super deep volatility, so for this reason I added the filter to help me be able to deal with it psychologically at such times. Yes, sure, I know I will be giving away some profits during these heavily volatile periods, but that is fine by me for peace of mind. In the end the small halt in trading during such heavy periods only damaged my CAR by less than two percent but helped me to really improve by drawdowns by more than 5 percent over the long term.

I want to make a note about backtesting. Don’t get lost in setting up a CMA-ES optimisation across 7 parameters on 4 indicators and then letting it run for three days and hoping to come back and see 20,000 tests now showing you some good results to choose from. Firstly, seven is just too many. Have three (or not too many more). And keep them basic like I said above with a MA or a HHV or LLV. Then when you run a CMA-ES optimisation, what can you see in the first 20 or 30 runs? In the first 100 to 200 runs? Within the first 20 to 30 runs you will no doubt get some zeros or low CAR % and crap DD with some really whacky/stupid mindless potential settings for the parameters (like you have a MA with a 2 to 300 range and it shows a result if you had set the MA at 2, which you would never do in real trade. but hey, the optimisation process is learning), but you should already be seeing positive CAR numbers in these first 20 or 30 runs. You might even be lucky enough to see not one single negative CAR in the first 20 to 30 runs. Then after 1 or 200 runs (which any PC running Amibroker, even with custom backtester enabled should do within just one or two hours) you must absolutely already be seeing a trend forming in the numbers. Also almost all the numbers need to be reasonably tradeable. I’m talking from say the 30th optimisation through to the 100th optimisation all punching out a good 10 to 20% CAR or more and a DD of no more than about 30% or less. If just this first initial burst of results generated in the first hour or two is not going in the right direction with these sorts of numbers or better then you aren’t going in the right direction and can stop the test and need to go back to the drawing board. Either you’ve got too many parameters, or your concept of what you are trying to prove is not correct. You want systems that even with the dumbest of the dumb, dartboard, blind Freddy settings are still going to produce profit right across the range. Sure, in time as you develop the system more you will be looking for settings that give you good CAR and DD and profit factor and sharpe, but that comes later. If you have a system that over a 10 year backtest or more that the most stupid numbskull settings are still going to see you make at least 10% profit then this is a very comforting place to be. Sure those stupid settings may still see you having to face a 30 or 40% drawdown, but isn’t it nice to know that as dumb as you may prove yourself to be in time that you are still going to make 10 % at minimum that you might be onto a good thing? As you develop the system yes you might find that 2 or 300 on the MA still produces profit, and there is a nice juicy band between 80 and 150 so sure, you will target this 80 to 150 area in your final settings when you get to the pointy end of your settings, but in the initial testing/optimisation don’t waste a long time. An hour or two, 1 or 200 tests is more than enough for Amibroker to tell you if you are onto something good/robust. Either it moves in the right direction immediately in this amount of time, or stop and reevaluate.

So since my re-work in the last few months I have been trading this since May and has generally been performing as expected when compared to backtest each day. Therefore I don’t have any great long term performance stats to share with you unfortunately. The backtested stats are roughly around 22% CAR and 10% DD over 15 years. Win/Loss is 55/45. Payoff ratio 1.85 . No, not really a “load the boat” kind of performance however I am not seeking that kind of performance for this system. This system for me is something I can easily drive along in the background with little stress and hopefully make some income over time. I am fortunate that I can put enough capital towards it that with these kind of returns over time it will be a nice income for me.

Also remember these numbers are only working for me whilst using leverage. If I don’t use leverage and still keep these high numbers of positions the numbers drop off to 8% CAR on 4% drawdown. I would need to do some work on what a good number of positions would be if not using leverage, but I would guess perhaps a quarter of the number of positions I am using. The problem in doing this though is that the number of signals and trades you would get would also drop off accordingly. This is a problem for systems like this as you really want a large number of trades (thousands) to be flowing through in order to see your edge play out over time.

Therefore I think I would conclude by saying that I really have only seen success in this method (both Long and Short) where I can use leverage and have a large number of positions and trades. If you don’t have access to leverage on stocks, or you have say 50K USD in total to throw at trading this type of system then I would say this type of system isn’t going to work for you. Having leverage and about 70 or 80k USD for each of the four separate systems (so a good 250 to 300K USD shared across all four systems) is probably a minimum starting point that I have experienced which works.

Also do keep in mind that when I make a tweet like I did yesterday this is me beating my chest, saying look at me I’m awesome. This is an irregular day and not in line with the long term performance of the system. It is of course very easy to be attracted to the stats I posted, but it is not normal. And I don’t feel guilty about doing that. Part of my “rediscovery” work I have been doing through reading in the last few months has also taught me there is nothing wrong with celebrating my wins when I have them. Sure, not to the point of fixation where winning is my only goal, but take the stage and enjoy the limelight when it does happen. For example last week on the four trading days of the week after the holiday every single day was green. A few hundred dollars here. One day was over $1000. Another day was about $5000. This week, I have had three red days in a row, each of them pretty small at a few hundred dollars loss each day. Thursday was a green day at 2K profit and then Friday was a juicy one with well into a 5 figure USD profit, thus my excitement in making my “look at me” twitter post. Normal distribution though is probably 1.5 to 2% profit a month.

If you do have say 50K USD in funds or less or the broker is not really playing ball with giving leverage, if you are looking for more juicy profits and not really interested in a slow and steady 20% CAR over the long term from a nice pool of funds like I am, then I would probably suggest looking at learning how to trade options. Options trading doesn’t have to be complex (especially if you just trade Index options) and it could lead to a good 50% profit or more in a year. Some options traders can also make 10% a month. And I’m not preaching one thing and doing another here, I myself am right now doing a training in a course how to trade options because I’ve never really done it (or done it well). I am hoping to add some simple options trades to my portfolio in the coming months. I am hoping to share this experience in my future journal at some point, but like other things, I will probably see if I am actually any good at it first before saying “look at me” in this project.

Or the other angle is day trading/scalping. If you want to be impressed by what an arse kicking effort at scalping/day trading can get you then just follow Nick Fabrio. Smart young guy in Melbourne, using 100K a month to make 100K a month. That’s right, 100% return a month. He is an absolute beast, but something I would never be able to do because of the stress and I don’t want to sit in front of the screens all day. I don’t think I will ever go down that line.

I hope I’ve helped!

June 8, 2020 at 8:21 am #111602InactiveHi Matthew,

Wow, thank you for the detailed and thoughtful response. Your comments and thoughts are very helpful!!

Regarding the system performance and you “beating your chest”, I completely understand and certainly wouldn’t not expect a system to perform like that every day!! It is important to celebrate the successes. The bad days can be so frustrating that you have to enjoy the good days to compensate.

I actually had reworked to MOC CBT code to work for short trades but just didn’t find anything that I really wanted to trade. I never was able to find a system that achieved the type of performance metrics that you mention so it looks like I need to go back to the drawing board and test some new ideas.

I currently do trade a short system but it is not MOC. I typically hold for 3-15 days. However, I do really like the idea of running a MOC short system to (hopefully) offset some volatility on the MOC long system I am running.

One quick administrative question, how do you track your short MOC system using STT? I am not able to automatically upload short trades that are exported from TWS, like you are able to for long trades. Its quite painful uploading short trades into STT because I am doing it manually in the upload tab. If you are generating up to 100 trades, this must be a nightmare to do manually??

Thanks again and I will keep you posted if I get to a result that I start trading!!

Best,

DustinJune 8, 2020 at 8:46 am #111606InactiveDustin,

Unfortunately I only use Share Trade Tracker to track performance and as trades in the IB trade log tag a short sale as the usual BOT and SLD labels, STT simply puts all the short trades into the trades worksheets as closed long trades.

This is of course unfortunate and something I wish was different in STT, but not too much I can do about.

That said I have two workarounds I usually use in monitoring the performance of the short system.

First thing is that I have a blank/dummy version of the STT spreadsheet on my desktop which I use only for the trades of that day. By uploading just the trades of that day it allows me to see the performance stats for just that one day of trade only. It also helps me to see that STT does accept the uploaded trades correctly. Every now and then the upload doesn’t work in terms of correctly matching all the trades. I simply close the sheet without saving and try uploading again and it usually works. This is also in an effort to make sure it is good so that when I do open my master long term STT and upload the day’s trades I can be confident it will do it well. Sometimes when it hasn’t I have to go and manually delete those trades and try again. I don’t really like doing that in my master STT, so anything I can do as a test to make sure it will work before doing it in my final, master sheet is a good thing. Once I have enjoyed seeing/confirming the data in STT for just that day of trade I simply delete all the trades and close it as a blank STT. I then go to master STT and upload the trades there for safe keeping for ever and ever amen.

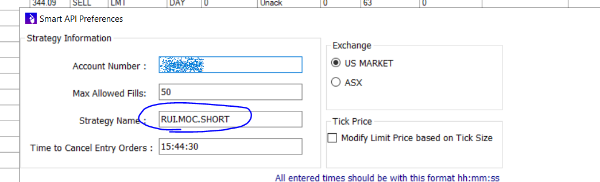

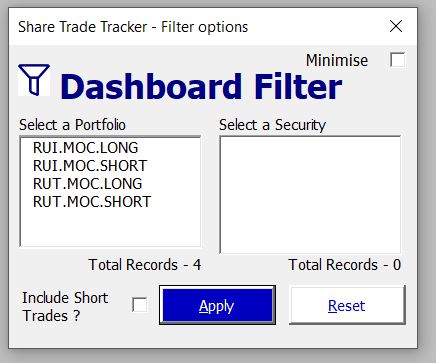

The second thing I do is just make sure my short strategies are exactly named in the settings field in the API and also as strategies in share trade tracker so that when orders execute the strategy name will be on each line of the trade log. STT then knows which trades are for which strategy. Then inside STT if I wish to see the stats for the short trades only I can just do a filter on the dashboard.

Even if you aren’t using the API to perform short trades, you could still always make sure the Order Ref. on any order you make in TWS is the same as how you have named them in STT so you can still do the STT Dashboard filtering trick at any time.Regards,

MattJune 9, 2020 at 8:16 pm #111607InactiveThanks again Matthew. This makes sense… as long as you trade a MOC system then this should work for STT. Also a good idea to have the dummy STT just to first check the upload.

I really appreciate you sharing your experience and thoughts!

June 11, 2020 at 2:21 pm #111617InactiveQuote:I cannot emphasize enough the importance of understanding expectancy, probability etc.!!!

Hey Matthew – do you have any overlap with your equity pools for these strategies to maximize exposure? Like, do you “double dip” at all assuming that you would not actually fill all of the longs and the shorts at the same time? I have a feeling like that is a bit too risky since you could get a margin call, but I’m curious if you have thought about it.

I say this as today I literally filled all 40 positions of mine at the open (I was watching and I saw my good friend the “REG T popup”) and was -117 in excess liquidity…. I just closed the RDP and buried my head in the sand.

June 11, 2020 at 5:06 pm #109462OmarAouane

ParticipantHi Justin,

about to start my journal after 1 month into the course and only in the system development part.

Ready through the forum, I am impressed by the returns of the various MOC systems while my first TF system is hardly beating the S&P 500 on my testting period (2006-2016).

To keep going your discussion about which system to use, I am convinced that the lower CAGR of trend following systems is the price for much greater robustness going forward. On a long enough period, there must be up trends on the stock market, in a similar way that economic GDP is mostly trending up. Not qualified yet to comment on MOC systems

Just my 2 cents…June 11, 2020 at 7:44 pm #110661ParticipantHi Scott,

I am using this path of thinking to hedge Amibroker systems using futures systems on TradeStation. I have coded many futures systems using Easylanguage. If you know which set up to play a breakdown you want to code. I will be happy to try to code it and sent it out

Let me knowJune 11, 2020 at 11:44 pm #111623ScottMcNab

ParticipantThat is generous of you Omar. I really should look back into that. I have a funded Tradestation futures account sitting idle. I keep getting drawn back into my Amibroker stock systems. I was experimenting with TS with an intra-day breakout system on index to the downside but have not touched it for many months. I find coding so inherently difficult that the thought of learning a new language leads me to other more urgent tasks…like sanding and repainting the window frames.

To get the maximum value from your mentor course it may be best to focus solely on it for the next six months. I would be grateful for your recommendations regarding Easylanguage after that time but it would be wrong of me to distract you for now.

CheersJune 12, 2020 at 9:50 am #111622InactiveSeth,

I make sure I keep enough cash for each of the four MOC strategies separately. I don’t assume some fills on one system and no fills on another system. I assume that in any one session any one system could meet it’s full order sheet entirely. I know that in some ways this could be considered inefficient as why would I get a full complement of fills on the short side systems within the same session as getting a full complement of fills on the long side systems, however I have not bothered to over think it too much in this regard. I guess if I really wanted to I could analyse the history of it and “over allocate” my cash across the four systems to reflect this idea but I’ve never gone to that complexity.

Also the cash allocated to these systems I like to keep separate from other strategies to again not run into any leverage issues.

So just for example, let’s say I had 1m in cash, I allocate like this:

10% Cash

20% Discretionary Systems

30% Options Systems

40% Day trade/MOC SystemsSo for the 400K I have allocated for the MOC systems I then might break it into something like this:

110K RUI Long

90K RUT Long

120K RUI Short

80K RUT ShortWhen doing my daily explorations these cash amounts allocated for each strategy separately is what I pump into Amibroker for each system exploration. The correct setting for leverage is set in each system.

I allocate the different amounts to each of the four MOC systems by the long term 15 year Sharpe ratio. This, to me, is the best way of ensuring I allocate risk/return correctly. Still, the numbers don’t differ greatly. It is not like I am allocating 300k to one of the MOC systems and then 20K to another because of a wildly different Sharpe. They are all within a ballpark so I could probably just allocate 100K each to all four of them and forget about it. It probably makes only a little difference allocating in the Sharpe way but I am little bit OCD in some ways.

Also don’t forget that a large part of how much you allocate to each system is going to be a function of how much drawdown you can tolerate overall over a period of time and and also in one day of trade. What I mean here is how much could you wake up to and see in one day as a red result and still think “Gee that sucks, oh well, I’ll do better tonight” versus smashing all the furniture in the room and not being able to trade tonight. That is only going to come in time as you see the really heavy days versus the good ones. For example today 11th June session was also a heavy red one for me, however the scale of it, even on a really heavy red day like today (whilst annoying and I have been grumbling to myself today) is not a level that will stop me from trading tonight. Therefore this tells me that the capital I am allocating to this system is probably around the right size for me and my comfort levels. Sure, it will still work if I double the size I have allocated and it will also work if I halve the allocation, but considering I am relatively at my comfort levels of the very extreme red numbers I could potentially see each day then I am probably in the right zone for the amount of money I have allocated to trade with this style right now. I am sure the same comfort finding mission will happen with you in time as you see the flows each day.

When I was originally trading these style of systems right in the beginning when I was learning and trying to take everything to an extreme with efficiency and allocation I was trading about four times larger allocation of what I am now and there where a number of times on the worst of the worst red days that the number I saw as loss each morning was really crippling to me and I could not trade the next session. Lo and behold the next session was a nice juicy green day (or would have been should I have traded it) and so the next day I was kicking myself even more. To lose, then not trade and miss out on profits is even worse than losing in itself. So don’t get too lost in trying to squeeze out the efficiency/maximisation of your capital each day. Think about and get the balance right on your what allocation feels right and works well for you in the numbers you may see each day on the screen, especially when they are red as those will be times you get sidetracked into doing stupid things.

July 2, 2020 at 9:02 am #111624InactiveHi guys, thanks again for the discussion. First, Seth, I actually do exactly what you are proposing by “double-dipping” with exposure. I am definitely not advocating that this is the best idea but I wanted to try to use cash more efficiently as the large majority of days I am with significant cash in my account. I trade 5 strategies, 1 of which is discretionary, so I have allocated capital such that if everything were fully deployed I would be about 130% of my account value. Practically, I think its very unlikely that I ever get to that but I am aiming to use cash more efficiently. I would also note, that my MOC strategies have quite long stretches and relatively low exposure/low drawdown, so if you are running MOC systems with higher exposure (usually higher return and higher drawdown as well), I would be more cautious with this approach.

Second, another follow-up for Matthew regarding your short MOC system, if you would be willing to share (if you do not want to share further specifics on your systems, no problem at all). Can you give me some guidance on how you rank the signals? Do you use something highly complex? I have tried absolutely everything I can think of as a ranking metric and the best I have arrived at is a longer term RSI, like 25 day RSI. However, the initial performance is still miles away from anything I would consider trading.

Also, regarding the significant number of positions both on your long and short MOC systems, do you mind me asking what your CAR/MDD is generally for your systems. When I look at my long MOC systems, the performance really drops off when I dramatically increase the number of positions. I am currently trading my long S&P500 MOC with 8 positions and have a 2.1 CAR/MDD (12 positions for my R1000 system)… as I increase to 50 positions the CAR/MDD declines gradually to 1.0. What I have found is that max drawdown doesn’t really increase with fewer positions but return definitely increases. i.e. the signals that I have defined really may be targeting the best risk/reward opportunity so adding more diversification actually isn’t attractive. Of course, this could just be over-optimized but the system is pretty simple so I’m not too worried about that.

Lastly, if you wouldn’t mind, can I send you my attempt to rework the CBT code? It seems to be working well but it would be great to compare given the CBT code isn’t so intuitive. If so, please message me at [email protected].

Thanks again.

Best,

DustinJuly 2, 2020 at 11:17 pm #111751InactiveDustin, I will send you an email. BUT, just keep in mind that I am also a learner, trying to find my way in this game just like you. Please don’t assume that I am some kind of authority or expert on these things. So I am happy to help where I can, but please don’t assume that you are going to get perfect advice/ideas from me!

For ranking my short system, I do it exactly the same as my long system. And it is super basic. It is not anything magical, just today’s range divided by long term ATR. That’s it. My theory is that a big move today, compared to what the ATR is over a year, shows if a move is strong or not.

However keep in mind that this is just the ranking metric. This is only one piece of the puzzle. Don’t assume that a ‘perfect’ ranking measure is the answer to the problem. You need to ensure that whatever methods you are using for identifying the symbols you are going to trade in the first place (your entry conditions, apart from the ranking) is a sound theory/method.

As per my posts in my journal, you can see what the CAR/MDD is for the short side systems. On the long side it is RUI 18.93/17.39 and RUT 23.52/10.20. Unfortunately on the RUI system the DD over the long term shows as 17.39 however over the long term it is closer to 12%. There was one single day in 2008 where it popped down to 17% so that is destroying the DD stat overall.

The problem I have found with increasing the number of positions is that it makes for better looking returns on those systems that have intermittent peaks or pops of profit. That is, steady growth over a number of years, and then a big hit of trades in one week. If you have more positions available, you likely have the chance of catching more stocks moving in the same fashion on those heavy trading days. For example maybe you had 50 positions and those heavy days 20 out of the 50 were really big movers (less than half). However if you had 100 positions maybe 70 positions out of 100 (more than half) were the big movers on that same day. Similarly if you have more positions then on the quiet periods that will make those quiet periods look worse as more positions with less equity per position then erodes returns.

So my advice on this part is that don’t get too lost/fixated on just the stats/numbers alone. You should always look at the charts in the second page of the report and see if the equity curve is something you are happy to work with, particularly with how it is going to work in conjunction with your other systems that will be running at the same time. It is ok to have something if it looks a bit bumpy, imperfect, if those lumps and imperfections are not very correlated to the same periods of time as your other systems you are trading. All of them working together to smooth out the ride is a good thing.

On universe, I have generally not found the S&P500 to work well with me on this style of trading. I have generally found only RUI and RUT work for me. My understanding is that this is because of the greater volatility of the symbols in these universe.

On positions, I am surprised to see you have 8 and 12 positions. Can I assume you are not using any leverage?

July 3, 2020 at 8:47 am #111764InactiveHi Matthew, first, thanks again. I must say I am impressed – from the time I initially asked you a question on here, you started your own journal and have 3 pages of entries. I have 2 pages over the course of 1.5 years

")

I have read through your journal so thanks again for sharing all of your learnings.

Regarding your question on the number of positions, you will be horrified to know that I am using 4x leverage. However, I have very strict index and volatility filters so that my stretches move out significantly (or are blacked out completely) at the first sign of volatility. Its pretty simple actually but the idea is to trade the system only in low volatility, up trending markets. For example, my MOC systems shut off on Feb. 24th and haven’t traded since (since the VIX has remained so high).

Of course, I am feeling some FOMO on this recovery but interestingly I have tested relaxing my filters through the recent rally and the system hasn’t performed great since the majority of the gains have been in the overnight market and then the down days have been quite vicious.

I clearly need to do some more Monty Carlo testing though as per the discussion on your journal. And I do need to consider more your point about unrealistic gains over short periods of time due to concentration. It may just be unrealistic.

July 3, 2020 at 9:03 am #111771InactiveDustin,

Wow 8 and 12 positions on 4x leverage is a massive amount of risk. So much so that it will not take long for these systems to hit ruin, statistically speaking.

At 8 positions on 4x leverage that means each position is taking up 50% of your equity. That is super risky. Or to put it another way, if there we no leverage the same as running two positions.

For me, at 4x leverage, I would not be taking any less than about 30 positions to help combat this issue of risking too much capital per position. It is very easy to get tempted, through the optimisation process, to see the results improving on just a small number of positions and from my tests a lower number of positions always ends up in higher profits.

Also keep in mind that a small number of positions means needing higher position sizes, and depending on your minimum price limit might mean you need to be submitting orders for 5,000 or 10,000 or 15,000 quantity which may in fact be only a small percentage of the daily volume of that symbol, however it just isn’t going to get filled in a quick millisecond that you need it to, by the broker. So you will probably be littered with partial fills and real time trading never matching backtests.

Good work on the volatility stretch idea, however that still does not prevent issues like gaps putting you in trouble.

-

AuthorPosts

- You must be logged in to reply to this topic.