Home › Forums › Trading System Mentor Course Community › Trading System Brainstorming › ASX Rotational

- This topic is empty.

-

AuthorPosts

-

March 9, 2019 at 10:48 pm #101905

Nick Radge

KeymasterSunday morning thoughts…

A number of students have mentioned they struggle with systems or that ‘certain’ systems don’t work on certain markets.

Maybe the real answer is you’ve yet to do enough research to objectively make that statement?

Example, a rotational system on the ASX.

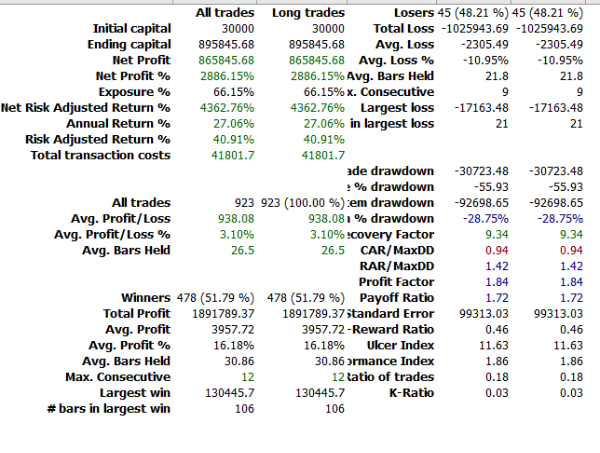

Alan Clement from Helix Trader seems to have developed a strong rotational system for the ASX. Here’s a good discussion paper on it, including position sizing etc, and a list of trades. Worthy of re-engineering…

March 10, 2019 at 3:42 am #109784GlenPeake

ParticipantThanks Nick.

Nice numbers.

Besides the very nice additional charts in the backtest report….

The following stood out…

Sector Maximum Holding

A maximum of 3 stocks can be held from any single sector. This reduces sector specific risk, by avoiding a high concentration of the portfolio in any one area.I understand the logic, diversify sector selection and don’t ‘load up’ in one specific sector in case it tanks… but on the surface it seems like it might also be restrictive…. what if 1 sector is ‘hot’ in a given period i.e. what if gold stocks are the flavour of the month(s) or technology stocks or uranium stocks…. you might be restricting yourself if one of these sectors is strong and there could potentially be 5 or 6 stocks (in the same sector) in the top 14 momentum list.

I get how having a max of 3 per sector could ‘smooth’ out the ride a bit… but might also ‘hold back returns’ as well…..an idea to try out in the future.

I guess like everything test it, test it etc….

March 10, 2019 at 3:44 am #109785WENKIT LUI

ParticipantHi Nick

Thanks for sharing this.

My personal experience is that A rotational system on the ASX does work. I am trading a monthly version on the ASX All Ords universe.

For me it would be interesting to re-engineer this weekly system and check the correlation of the system performance with my monthly version.

Cheers

KitMarch 10, 2019 at 5:32 am #109786MichaelRodwell

MemberFrom the forums it appears that most people are trading monthly rotational systems. I’ve heard Alan comment a number of times that weekly has been the sweet spot that he’s found. Might be one of the variables that makes the difference in the ASX.

March 10, 2019 at 5:42 am #109789MemberQuote:Thanks Nick.Nice numbers.

Besides the very nice additional charts in the backtest report….

The following stood out…

Sector Maximum Holding

A maximum of 3 stocks can be held from any single sector. This reduces sector specific risk, by avoiding a high concentration of the portfolio in any one area.I understand the logic, diversify sector selection and don’t ‘load up’ in one specific sector in case it tanks… but on the surface it seems like it might also be restrictive…. what if 1 sector is ‘hot’ in a given period i.e. what if gold stocks are the flavour of the month(s) or technology stocks or uranium stocks…. you might be restricting yourself if one of these sectors is strong and there could potentially be 5 or 6 stocks (in the same sector) in the top 14 momentum list.

I get how having a max of 3 per sector could ‘smooth’ out the ride a bit… but might also ‘hold back returns’ as well…..an idea to try out in the future.

I guess like everything test it, test it etc….

I came across this post from JBMarwood today that is somewhat related:

https://jbmarwood.com/simple-breakout-system-sector-filter/

He adds a sector filter to the buy criteria as follows:

“sector that stock belongs to has a 3-month RSI reading above 50”

Might be another way to approach the sector question… (yes, I will test… easy does it though… still trying to figure out the index filter)

March 10, 2019 at 5:49 am #109792KeymasterI’m very cautious of using sectors in the ASX. Many have single stocks that make up a huge percentage of the sector itself.

March 10, 2019 at 7:40 am #109787ScottMcNab

ParticipantCouple of things I noted.

The exposure at 56% caught my eye..and only 34 trades a year…lower than the rotational systems I have been trading (and allows up to 14 stocks)..win rate is good too…will explore this more as taken together indicating system is very selective in trades entering

No detail as to what actual liquidity filters are unfortunately…would have loved to see this (I might work through the trade list stock by stock when get time to try and gather more insight).

With system I am currently testing on XAO over these dates (previous live results been on XTO) then get (cagr/maxDD):

price $1 and turnover 100K: 24/-27

price $1 and turnover 200k: 22/-27

price $1 and turnover 300k: 21/-27

cagr drops further still for me (into high teens) if include MA(volume,20) filterother stats for Helix Trader system (cagr/maxDD, profit factor and payoff ratio) all good….like really, really good

March 10, 2019 at 9:43 am #109788ParticipantWent through some of the trades and read post in detail several times

Early days as only worked on the idea for an hour or so

Results are for filters set to price> $1, 500k min turnover and volume and with MA(volume,20)>500k

Looks promising. Thank you for posting Nick

March 18, 2019 at 10:03 am #109793

March 18, 2019 at 10:03 am #109793RobGiles

MemberThanks Scott, How are they calculating momentum?

March 18, 2019 at 8:56 pm #109817ParticipantHi Rob, I can’t get my stats to look as good as HelixTrader indicating I am not doing the same thing but the key takeaway for me was using historical volatility …previously I had been trying to select stocks that were not volatile …

for momentum I just used ROC…

the system I posted above did not do so well in 2000/2001 (massive DD)….my current version has cagr/maxDD of approx 25/-26 for 2005-present on XAO using same price and volume filters…not sure how your AUS rotn systems going but for me embracing volatility has been a sig improvement

March 18, 2019 at 9:29 pm #109818ParticipantDitto Scott. The HelixTrader results do appear too good to be true after I ran some quick tests myself.

Personally a weekly rotational system that is not superior to a monthly system.is “too much work” for my liking

I suspect that restricting the system to 3 companies per sector is something that HelixTrader have done to improve the system but I haven’t tested thisMarch 20, 2019 at 12:31 am #109819MemberScott McNab wrote:Hi Rob, I can’t get my stats to look as good as HelixTrader indicating I am not doing the same thing but the key takeaway for me was using historical volatility …previously I had been trying to select stocks that were not volatile …for momentum I just used ROC…

the system I posted above did not do so well in 2000/2001 (massive DD)….my current version has cagr/maxDD of approx 25/-26 for 2005-present on XAO using same price and volume filters…not sure how your AUS rotn systems going but for me embracing volatility has been a sig improvement

Thanks Scott

That’s interesting as I’ve been looking at Trend Following systems that include a Historic Vol Filter. What lookback are you using? I’m looking at 100 days. and we’re wanting stocks that are equal to or above the ave HV of the Index (which for the S&P I think is 100 days). I’ve put the ASX on ice as I couldn’t get anything I liked and how much time do you write off doing research? I figure the US markets have much more liquidity and opportunity.March 20, 2019 at 4:34 am #109829ParticipantI used HV100 too Rob

-

AuthorPosts

- You must be logged in to reply to this topic.