Home › Forums › Trading System Mentor Course Community › Real Test Software › Introduction

- This topic is empty.

-

AuthorPosts

-

October 2, 2020 at 9:40 am #102054

Nick Radge

KeymasterWhilst our software of choice is Amibroker, Real Trade is very easy to use and offers some interesting features that Amibroker doesn’t.

I’d like to thank Len for putting me onto Marsten Parker and I believe a few others have also taken a look.

At this stage the software is available for free but as Marsten is about to become a very public figure (he’s in the new Jack Schwager book – “Unknown Market Wizards”) I would suggest he’ll monetize is in the coming months.

I’ve only touched the surface of the software and it does bring back fond memories of coding with TradeStation.

It integrates with Norgate Data easily and I think (at this early stage) one of its potent features is the ability to code different strategies within a single file then weight them for the optimum results.

I have partly coded one of my rotational strategies that uses both weekly and monthly signals.

I’m looking forward to discussing and sharing.

October 2, 2020 at 10:13 am #112241GlenPeake

ParticipantThanks for the update/feedback Nick.

October 3, 2020 at 12:05 am #112242JulianCohen

ParticipantOK well that’s the next few weeks sorted out for me then

October 3, 2020 at 9:16 am #112246ParticipantHas anyone figured out worst rank or the gap filter yet?

October 3, 2020 at 12:06 pm #112248ParticipantJulian Cohen wrote:Has anyone figured out worst rank or the gap filter yet?Re: GAP

Not sure if this is will do the trick???

-

This reply was modified 1 week, 1 day ago by

RossDawson.

October 3, 2020 at 9:49 pm #112249ParticipantThanks Glen

I asked Marsten and he sent me the following:

See my ndx_rotation.rts example script. I do it by calculating the rank factor in the data section and then referring to it in the entry setup and exit rule.

For mean reversion strategies, see MaxSetups / SetupScore (as used in mr_sample.rts), and also MaxEntries / EntryScore. These replace the CBT code that is often required in AB if you want to only place a specific number of limit orders each day, and/or model taking the first 10 that fill from 40 candidates or something like that.

I’m not quite sure I follow that and having rethought what Len said, I might try and code up MR systems first. I believe Len said he uses Amibroker for rotation systems.

October 5, 2020 at 4:24 am #112250KeymasterHad a good chat with Marsten today and have read his chapter for the new boo (due Nov 1).

He’s set up his own forum and he’s very willing to answer questions.

October 5, 2020 at 5:33 am #112260TrentRothall

ParticipantI’ve coded up some test MR/ MOC systems on it and i think it’s great. [strike]Simple[/strike] relatively simple yet very powerful. Happy to discuss and looking fwd to it!

October 5, 2020 at 5:39 am #112261ParticipantTrent, is there any chance you could post up a template of an MR/MOC system without the magic sauce of course.

I’ve been trying to apply Marsten’s but he is trading in a very different way to us.

We have say 3 systems and run them independently but his code all seems to have all the systems in one portfolio and the candidate entries from each system go into a pool which is then ranked. So where as we might have 3 systems running at 20 position and 10% per system which would give 60 entries, he would only have 20 entries from the one portfolio.

Sorry hope that is clear.

I’m not sure which is a better way to go….do you want more trades or less?

October 5, 2020 at 6:17 am #112262Participant** i’m no expert clearly but i think this is correct

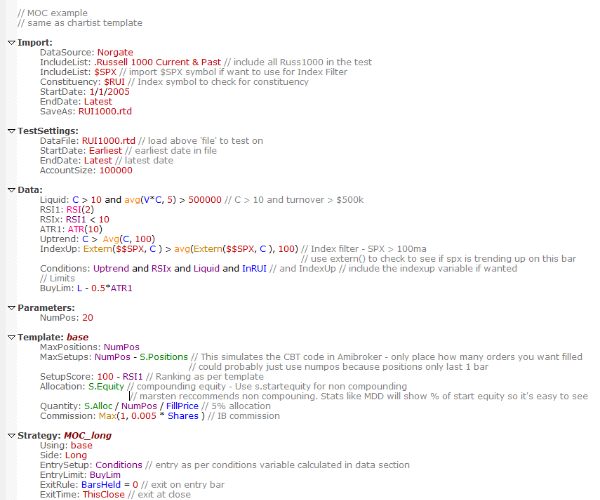

This is the same as the MOC template in the course.

This is just a single system with 20 positions, max setups per day is 20.

October 5, 2020 at 6:24 am #112263ParticipantI want more trades. One of the issues I have had with the MOC CBT code is that it was limited to the number of setups (orders) == positions, I probably should have tried harder to change it but I didn’t get around to it! I know that removes all the selection bias but I just struggled to limit my possible entries. I would rather have the API do its work I think, with his program it is easy to set the maximum setups to say 40 and entries to 20. So if there is 500 possible entries for the day you will rank the top 40 and place them into the market.

October 5, 2020 at 6:38 am #112264ParticipantBecause it’s a single system you don’t need to use the “Base” template. you could just have all the ‘Strategy’ parameters under

Strategy: MOC_long“Template: base” is more for common strategy elements

October 5, 2020 at 8:23 am #112243ParticipantThanks for that Trent.

I’ll have another play tomorrow

Not sure I follow what you are saying about the CBT code though….why were you struggling with limiting the entries?

October 5, 2020 at 8:45 am #112266ParticipantNot the entries but the setups. I (think) am happy sending say 30 orders with max entries of 20. So there is still a degree of selection bias but restricting the setups would help with variation in tests i think. Does that make sense

October 5, 2020 at 11:01 pm #112267ParticipantWell I guess. That means in effect that you are looking at the CBT code as a mild form of curve fitting, which is a valid argument.

-

This reply was modified 1 week, 1 day ago by

-

AuthorPosts

- You must be logged in to reply to this topic.