Home › Forums › Trading System Mentor Course Community › Progress Journal › Matthew O’Keefe’s Journal

- This topic is empty.

-

AuthorPosts

-

June 12, 2020 at 9:58 am #102033

Anonymous

InactiveThought I better get my bum into gear and start my Journal. It seems I’ve been a bit more active of late on the forum with feedback etc and I’ve been hijacking other users’ journals which isn’t good.

So, here we go!…

June 12, 2020 at 10:15 am #111625JulianCohen

ParticipantTip Top!

So…short MOCs….Do you have any practical issues with shorting stocks in the RUT?

June 12, 2020 at 10:30 am #111626InactiveJulian,

You asked me about shorting the MOC system in your Journal. I am taking the initiative to start my own Journal at your advice. Sorry it has taken until now….

Generally speaking I have not found much of an issue so far in shorting my MOC system.

I say generally speaking because of the 130 orders I enter each night (50 on RUI Short and 80 on RUT short) I can easily go for days or even a whole week without any one single order (upon Sending the orders from API to TWS) being stopped/flagged as not available for short sale. Or maybe on one day I might get flagged for one. Or maybe two. The order will otherwise be rejected by TWS. However I would say that in every 1000 orders this would probably only happen perhaps 20 or 30 times.

I often find that they are only very random, like a pharmaceutical stock where they’ve applied for no short sale status in advance of the session.

The other thing that sometimes happens is that the order will still stay active, but I will get a “Order being held while we locate securities” or something like this. Usually by the time the session open comes around the order will be live and it can still be shorted.

Between these two situations, I deal with it in the following ways:

Firstly it is likely that my daily exploration gave me more than 50 potential orders for the day anyhow. Maybe one order got the no short sale flag when sent from API to TWS, so I’m down to 49 potential orders for the day. If I could really be bothered, I will cancel all 49 of the other orders, close the API, open the spreadsheet with my daily orders and re-paste the exploration from Amibroker with the top 51 orders, delete the one I know is going to fail, still have 50 orders in total, save sheet, re-load API, send orders again to TWS. This way I still have 50 orders for the day. This, of course, is if I could be bothered. Sometimes I just think “Bah who cares it is only one order” and then do nothing and just stick with 49 orders for the day.

The second thing I do is simply look at how the stock traded through the session during my post close analysis each morning. 9 times out of 10 usually the stock that initially got rejected got nowhere near my limit order price for the session anyhow, so I wouldn’t have even gotten a fill on it. So this further gives me peace of mind I am not missing out and shouldn’t panic too much when this happens.

Also keep in mind how we are targeting the trades and how it would work from the short side of the trade in this MOC style system. Yesterday’s close was $90. My limit sell order to go short is for a stretch at $95. Whether it gaps up on open or finds its way to 95 during the regular session, it is only after I get my fill at 95 that (I’m hoping) the stock then plummets down for the day and the short sale restriction gets automatically triggered at some point. This is quite entertaining in a way, because I will often wake up to a session where I have made some good profits on short sales and yet here I see the Sx short sale restriction flag sitting on the stock. Short sale restriction exists, yet I still shorted it and made money for the day because I got in before the restriction was placed. Closing the order at the end of the day with a buy MOC still happens. So I generally find the short sale restriction status only pops up during a volatile session in which the stock is dropping in price. Either I got a fill before the carnage in my favour, or I didn’t get a fill to begin with. Either way the short sale restriction is irrelevant in this case.

The number of very small handful of pre-planned short sale restricted stocks that I cannot place at the time of order entry would be far less than the number of trades I miss out on because the “After 3.45pm” thing. For every 10 stocks in a week that Amibroker thinks it got filled but I didn’t really get because it was after 3.45pm, then I might get one or two of these short sale restriction issues. To me, I don’t lose sleep over these quantities of ‘missed opportunities’ on a system that I am getting an edge by large trade volumes.

June 12, 2020 at 10:42 am #111627InactiveIn case you don’t follow me on Twitter, I had a crap MOC day today.

Behold the magnificence of a sea of red….

I only had two shorts filled for the day, at least both were profitable. The remaining 165 trades were all the longs which is a record of Long fills for me.

The other good piece of news is that the total loss in dollars represented a good or “comfortable” amount of loss for a single day that I think I am comfortable with, telling me that the amounts I am allocating to these strategies is probably a good balance in terms of all strategies in my account. If the number I faced today is the deepest that it gets red, I’m happy with that.

June 12, 2020 at 10:03 pm #111628InactiveWas going as an ok week until the Thursday session.

Then today’s session was also interesting as I had no fills whatsoever, neither long nor short.

Reason why was the volatility filter I have included to ensure I don’t trade when things are wild. The Thursday session caused this filter to trigger for my RUT Long, RUI Short and RUT Short systems. Interestingly, it did not trigger for my RUI Long, so I did still load orders on that system. Alas there were no fills whatsoever on that one system.

So the week closes down, but still up for the month so far. Would have been up about 7.3% for the month until Thursday. Now down to 3.6% up for the month thanks to the Thursday session. Still, I need to be happy because 3.6% for the month is still ahead of the game in terms of long term expectancy. Let’s hope I can hold the 3.6 for the rest of the month, or maybe even add to it, however I do have to be realistic that I should only be bagging around a 2% per month profit over the long term on this system.

One thing I noticed in today’s session is that the shape of the RUI and RUT was probably good for the short system. I haven’t done so yet, but it will be interesting to see if I turn off my volatility filter on the short systems and backtest them what the result would have been today. I get the feeling it would have been a good day on the shorts as the day had a pop up on the open and then a slow trickle downwards to the close which is perfect for the short system. This gets me to thinking that perhaps I shouldn’t use the same volatility filter on both my long and short systems (which is what I currently do). Perhaps I can come up with a way to restrict trading on the long systems if there is a great deal of downside volatilty (yet allow the short systems greater leeway to still perhaps trade in this instance) and vice versa for the volatility filter used in the short side system. More like a directional volatility idea, not just an “overall volatility” method like I currently use on both systems.

June 13, 2020 at 9:10 am #111639ParticipantThanks Matthew. I had a shocking day on Thursday so you’re not alone. How do you use the Sharpe Ratio to allocate the position size?

June 13, 2020 at 10:05 am #111643InactiveJust add them all up then divide by the total.

For example across the four strategies the Sharpe’s might be:

RUI Long: 2.19

RUT Long: 1.89

RUI Short: 2.29

RUT Short: 1.95

Add all four together: 8.32Then just divide the Sharpe for each strategy by 8.32. So:

RUI Long: 2.19 / 8.32 = 26.32%

RUT Long: 1.89 / 8.32 = 22.72%

RUI Short: 2.29 / 8.32 = 27.52%

RUT Short: 1.95 / 8.32 = 23.44%

Total: 100%So these percentages are what I then allocate to the cash to use for this type of trading. Let’s say I have $1m cash in my account, and perhaps I decide I am going to allocate 40% of my funds to this MOC style of strategies, then 400K would be broken up in the split I listed above.

RUI Long: 2.19 / 8.32 = 26.32% = 105,280 USD

RUT Long: 1.89 / 8.32 = 22.72% = 90,880 USD

RUI Short: 2.29 / 8.32 = 27.52% = 110,080 USD

RUT Short: 1.95 / 8.32 = 23.44% = 93,760 USD

Total = 400,000 USDProbably makes no difference at all over time, however I do it this way just in case the Sharpe’s are somewhat different across the strategies. I only listed example numbers here, these are not my real Sharpe’s or allocations across the four strategies. I just have a small simple table in excel which I populate with my updated total balance of my account at IB each day. It then shows me these numbers to use for my exploration each day. I don’t change my allocations around too much. Maybe once every few months I might have a change of heart about how to allocate across multiple strategies and might dial the MOC down to 30% or up to 50% or however I’m feeling depending on market conditions etc. However within the MOC systems once I’ve decided I’m going to use 40% of my overall funds on that type of trading then yes, I use the Sharpe method to help take any further decision making out of it for each days’ exploration.

Again one of the things I’m probably being too silly/overthinking about, but I like to do small things like this to ensure I am “doing the right thing” in putting my money in the best risk/reward systems.

Seth’s question on this topic is a good one. If it is highly unlikely that I would ever get a full load of fills on both the long and the short systems, then I could perhaps “over allocate” funds to these strategies and still not likely run into any leverage limits even I get full fills on one side. Still, as per my comments on this topic, I am at a good comfort level right now with what I have allocated to these systems and the worst potential red days that hit me in the face every now and then. As (hopefully) profits grow and compound on these systems over time, I am probably going to withdraw funds or use profits in other trading methods/systems and keep my general ballpark of capital allocated to these systems close to the region it is currently sitting.

June 13, 2020 at 1:19 pm #111644TimothyStrickland

MemberGood info Matthew,

I have yet to make my first MOC at all but will be working on it soon. Hopefully, I can use this info when the time comes.

June 14, 2020 at 4:29 pm #111645LEONARDZIR

ParticipantI had an interesting week as well. On Thursday my MOC take an 11.5% hit which was a function of volatility and 4x leverage. On the other hand my MR system which does not use leverage came into Thursday mostly short so nice profit. I am finding though stressful my MR systems (long and short) thrive with the volatility.

I am rethinking using an MOC with leverage. I am ok with a small account but doubt I could handle a large account with 4x leverage especially with persistently high Vix levels.

June 15, 2020 at 2:43 am #111646InactiveLen,

If you are thinking about this issue of how much to allocate in terms of both cash and also your leverage levels, have a think about this method to help you with decision making. This is something that helps give me peace of mind that such things are set at levels within a range that work well as far as the system is concerned. No, this method doesn’t really help with your general comfort levels in what you have to see each day in terms of red on bad days, only you can set those levels with your gut in time, but it does help give you peace of mind that your system is using levels of cash and leverage that are working well for the design of your system. If this process helps you always ensure you are using good cash and leverage levels, then that is one less dimension to worry about.

In Amibroker, note the setting in the Analysis Settings, Portfolio Tab, “Limit trade size as % of entry bar volume:”. When I am building my systems I always keep this set as 0 in the first stages of my builds/tests/optimisations. Some may see this as totally wrong/stupid, but I do have my reasons…..

Firstly, I only do this method if in my code I have an average daily volume filter set. In my case I set it to 100,000 units daily volume. I am comfortable with this level because I also have my price minimum set to $10 and I know that in my system I am generally going to be trading no more than about 1,000 units volume a day, maybe 2,000 on the very low $10 stocks. Therefore I know I am not going to be trading an excessive amount of volume compared to the total daily volume for that symbol. Also I am trading RUI and RUT which need to have lower volume hurdles otherwise many of the symbols would be excluded as sometimes volume can get below 100K per day on the lower capitalised stocks.

When I am building/designing/optimising in the initial stages of a system I always want to know over the long term (say 10 to 15 years or more) if my system holds water in terms of its entry/exit rules, whether the concept overall is a good one etc. The last thing I want to know about at this early point in the process is “Are my orders getting too large in year 5, too large in year 10 to the point that my trade size is starting to exceed 10% or 50% or some other percent of daily bar volume”. This is largely irrelevant at this initial stage. You want to be knowing whether your entries/exits work well, if your concept is right, are explorations matching your backtests, if what you are trying to prove to yourself actually works as an idea overall, over the long term, over 10 or 15 years. It’s like saying “work out if you are a good soccer player first instead of worrying (right now) about whether or not you are going to be able to play 10 games a day for 3 different clubs in two different countries in ten years time when you are going to be the best soccer player in the world because that is how you are going to get more contracts and make more money when you eventually get there in 10 years time”. Who cares about 10 year practical/logical limitations like this right now? What you need to be working out right now is if you are a good soccer player or not. If you set any number other than 0 in this setting, then this is the kind of limitation to your system backtesting you are going to be introducing, right from the outset.

If you do a 15 year backtest and start at say $100,000 cash (forget leverage for now) across 20 positions, that’s $5,000 per position. Let’s say your price minimum filter is set to $10. So you will be buying 500 units on the $10 symbols right from the first day of the backtest. If your system is totally awesome and makes money every year, maybe in year 10 your pool of cash is up to $2 Mil. At 20 positions you are now placing $100,000 positions. At your $10 min you need to buy 10,000 units per order, at that time. However if you are trading in stocks that are doing just 100,000 daily volume, 10,000 units to buy and sell is really starting to get beyond a limit where you may start affecting the market price. Or you won’t be able to get your fills instantly because there isn’t enough volume trading at the split second you need it. So the argument is then “well I can combat this by using this setting in Amibroker to limit my trade size to 5% of trade size as entry bar volume, so I will set it at 5”. Well, at this point in ten years time with your $2m account balance, this means your order which should have been a 10,000 unit order is now going to be limited by Amibroker to just a 5,000 unit order to honour this setting. This means that as your account size grows to large amounts in time, your system of how you intend to trade is going to be affected by trade size. Perhaps then as you run the backtests the result in year 5, year 10, year 15 always “seem to go flat or drop off and I don’t know why”.

Another argument is “I’ll just set my daily volume limit to 500K units”. Ok, but how long is a piece of string? If you keep raising such limits to avoid such pitfalls in the long term future you are going to continually “size” yourself out of potential trades and then you are going to say “I’m not getting enough signals”. Particularly on these MOC style systems, you want volatility, you want some bumpiness. This is why we are playing in RUI and RUT land, because we want the somewhat levels of volatility and the lower cap stocks, the ones with lower daily traded volumes, provide this.

Therefore in the early stages of developing my systems I always keep this setting at 0 so I can see, in time, if my system holds water over the long term from a concept point of view, not a “how large do my orders need to be in 10 years time” kind of view. The size of your orders in 10 years time is irrelevant at this early stage. Who cares if in your backtest in year 15 your orders are showing as 300% of the daily volume. Sure, I know that is completely impractical, and I do get to this point below, however at this early stage of “Does it work?” this setting is irrelevant and I set it to 0.

So, I put my setting at 0, I do my building/testing/optimisations, see if my concept is working etc. So after all that process with my setting at 0 I think I am onto something. My long term backtests are looking sweet. All the stats are good and all the plots in the report are acceptable even after 10 or 15 years. I think I am ready to trade this system. Now is the time I start to play with this daily limit setting to something other than 0.

With the setting kept at zero, I set my parameter for Capital “Initial Equity” to something small like $5,000. Total number of positions and your leverage are not relevant at this stage, just keep them at the desired settings of your system. I set the optimisation range from 5,000 to 1,000,000 with increments of 5,000. I set this parameter as an optimisation item, not a PARAM.

Then I run an exhaustive optimisation on just this one parameter for the most recent three years. As the test runs, line by line I will see the stats flowing. I’ll look at things like CAR, CAR/MDD, Max Sys % Drawdown, Sharpe, RRR, Ulcer performance index, number of trades. I’ll see across all these stats that as the pool of initial equity grows, 5,000 10,000 15,000 20,000 etc that these stats will often change and then at some magic point you will start to see these stats flattening out with little change from one test to the next. The total number of trades was 5,374 on the first test and then 5,765 and then 6,290 and then 6,312 and then 6,333 and then 6,335 and then 6,335 and 6,335 and 6,335. And hey presto, at roughly the same line/test the Sharpe is flattening out and not changing any more, same for CAR/MDD. And this is all around the 50, 55, 60,000 mark initial equity. This then tells me, roughly speaking, that at my positions and leverage probably $60,000 is the absolute minimum amount of equity I should be using on this system. I don’t wait for the optimisation to go all the way through to 1Mil initial capital because I can already see where the flatline has started, so I just stop it early.

I will do this process again, however with 2x leverage, 3x leverage, 4x leverage. All in separate runs. After doing it across the various leverage levels this helps me see where, in each case, my stats are “levelling out”. This is important because there is no point trading this system with 50,000 capital at 4x leverage if you discover through this process that your system only has flatiline stats starting around 120,000 Initial Equity at 4x leverage.

You might find through this process that if you reduce your leverage, maybe the limit is lower (or higher!). Also it is dependant on how long you do the backtest. There is no point doing this method on a 15 year backtest because this will assume that at your starting capital, plus all those years of growth, that each and every year, right up to the last one with massive profits and massive position sizes, can still produce a backtest with flatline results compared to the previous year. Therefore I only ever use three years on this method. I use this time frame because honestly there is no way in hell that I am ever going to run a system where right from the beginning, to right at the end of three years I have NEVER taken some profits out, or reallocated some in, or changed the rules of the system, or re-optimised it at the end of the year should I feel market conditions are changing. I think probably none of us here on the forum would engage a system that remains EXACTLY the same and untouched in three years time, with every single order placed perfectly as per what would be reflected in a backtest, with no capital added or withdrawn.

Ok so this is the “finding the minimums” process.

The next step is finding the maximums.

In my parameter for Initial Equity I now set it to 100,000 and 100,000 starting, 10,000,000 ending and 100,000 increments. However before I run the optimisation now I go into the Analysis Settings, Portfolio Tab, “Limit trade size as % of entry bar volume” and set it to 5 (5%). I run a three year backtest again (most recent three years). This time it is like the opposite of what I saw in the first process. It starts with all stats in the first runs of the test looking flat. Nothing seems to change, it keeps rolling along, then, suddenly, at 1.1m and then 1.2m and 1.3m the Sharpe is dropping off, and the CAR/MDD starts dropping off. Many of the stats start falling off. So this would tell me the most capital I can allocate to this strategy is around $1.1m. I would probably limit myself to 1m in this case just to make sure I’m within upper limits. Like the first process, this is important in knowing where the strategy is going to be limited to how much capital you can expect to use in the future when the account grows. This strategy is obviously not infinitely scalable because you will, in time, run into this limitation of daily trade size.

However (and this is the important part) why worry about this upper limit right from the outset when designing your system and proving a concept you are thinking of works or not? If you keep trade size volume set to 5 or 10% at all times whilst building all you are going to do is depress yourself into thinking your system or concept “doesn’t work” because it just so happens that you have this trade size limit set to 5% and just for laughs you set your initial capital in backtests to 1,000,000 because this is a nice round number for you to think of and then all your backtest over 15 years produce rubbish results/plots/returns because pretty much right from the outset you are already hitting a 5% trade size limit. You start doubting yourself and saying “Bah that concept doesn’t work”. Who knows? Perhaps it does actually work when using just 50,000 initial capital?

On the other end of the spectrum maybe you were lucky and set your initial capital to 100,000 which works well as a starting point, but then your system looks totally awesome and returns 30% year on year until about year 7 where the plots start to look like they drop off and then for your 15 year backtest you are saying to yourself “seems to work well in the early years, but the later years it is not working, oh well that method of trading mustn’t be working any more”. In reality, you are never going to start the system with 100K and then never touch any profits or still be trading in exactly the same way with the same system and same pool of capital as what you did ten years ago, so back to the soccer analogy, why worry about what is going to be “possible” in ten years, and the limitations that may come from that possibility in ten years when that event is not likely to ever happen anyway? Worry about what happens in ten years with overallocation and trade size limits in ten years from now. Worry about now and just the next few years only. Over-worrying about things that are never going to happen in ten years is just going to make you throw good systems in the bin because you think they don’t work long term and perhaps this is the problem causing the system look crap in the long term?

So that is the process I do. I always keep my “Limit trade size as % of entry bar volume” set to zero at all times in the building/testing stage and only ever use it right at the very end when I am doing my checks and balances on how much capital I should and shouldn’t be using in my systems for both minimums and maximums.

A precaution on these MOC systems I have experienced with the upper limit…

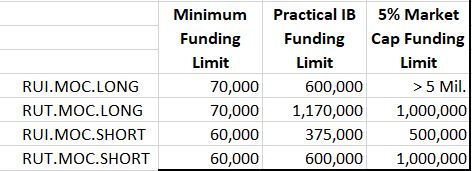

Even though you go through the process of knowing where your upper limits of capital may sit, I have found it is the practicalities of Interactive Brokers being able to hit your fill prices in short amounts of time that are the ultimate limiting factor on large order sizes. In my experience once you starting needing to place orders with LMT orders at say, 3, 4, 5,000 units or more you are going to start running into problems with rapid execution of the entire order. As orders can be executed by multiple venues in the US, orders are almost always split and you will get filled in lots of whatever is available to trade at the time you need to trade it. So if you have a 5,000 unit order it is likely to be split into odd lots of 56, 1,200, 650, 480, 150, 996, and whatever else odd lots until the full 5,000 unit order is filled. This takes time. It could take a good 10 seconds to fill such an order. It is often the case Limit prices traded in the day may only hit your price for a matter of seconds, or less than a second. So the smaller your orders, the more likely you are to be filled instantly or fully. The larger your orders the more likely you will be only partially filled. In the case of no or partial fills because your order is so large, this then introduces the problem that Amibroker cannot see this problem. It believes your Limit price was hit for the day and will assume the full volume of your order is filled.In my experience I try not to play with orders on this system any larger than 5,000 units. Even better is that I try to not use any more than 1,000 unit orders. The easy way to work out the absolute maximum capital you should be allocating to your system to combat this problem can be calculated from this target. For example:

1,000 unit traded max X $10 minimum = $10,000 per position.

You have a 40 position system, so 40 x $10,000 = $400,000.

You wish to use 4x Leverage so 400,000 / 4 = $100,000.

So by this trade size limitation method you would probably not want to allocate any more than about $100,000 to this system. Sure, you can allocate 200,000 because your earlier tests told you that 1.1M capital was the maximum, however that maximum is now irrelevant if you are placing a 2,000 unit order and cannot get instantly filled. I am not saying that 2,000 should be the limit. I am not saying 1,000 should be the limit either. I am just saying be aware that it is likely the rapid order execution limitation that will be experienced before you run into any “Account is too large” limits.Keep in mind that more positions in your system helps combat this problem, because your total capital gets to be less per position, and therefore less units would need to be ordered per position. A higher minimum price like 20 or $30 would also help. However, remember there is always a tradeoff between number of positions and profits (the temptation is to use less positions so as to attain more profits, albeit with higher volatility) and the more you increase your minimum volume and minimum price the less signals you will get. I use the following number of positions on my four MOC systems. This is where I have found comfort/balance:

RUI Long 80

RUT Long 160

RUI Short 50

RUT Short 80FYI I keep a small corner of my daily sizing spreadsheet to just act as a simple reminder of my cash limits.

Perhaps these methods helps you in your case, because you might find that through all of this actually you need to trade a larger amount of initial capital, but less leverage. Or maybe the opposite is proven true. You have been trading 200,000 USD capital on the strategy at 4x leverage and now after 11th June results you are thinking you should dial down your leverage, whereas in actual fact you might find that you can keep your 4x leverage but just drop your capital allocated to this strategy down to 70k instead, which still achieves your idea of “lower exposure” and the stats/workings of the system will still function properly. The obvious danger here is if through this method at 4x leverage your minimum limits of a stable system are 70K and you say to yourself “well I’ll just knock initial capital down to 30k for a while until I’m more comfortable”. This would obviously be an error because the system is not going to function properly and produce results that don’t reflect backtests.

Sorry I write long. That’s my style.

June 15, 2020 at 12:01 pm #111647ParticipantThanks Matt. Interesting approach.

My MOC has backtested CAR 48% and max DD 19.4% with 4x leverage. It is the psychology that is the issue. I am currently trading with a small account 50k but was planning to ramp up to 500k if it worked well. Problem is a 60k loss in one day is past my uncle point. Thinking about ramping up the account with no leverage which would leave me with a good income producer and acceptable drawdowns.June 15, 2020 at 2:38 pm #111648InactiveQuote:Sorry I write long. That’s my style.You don’t say…

June 16, 2020 at 5:35 am #111649InactiveSo to make sure I have this right, you were using 50k cash, at 4x leverage, on this system that produces CAR 48 and DD 19.8 and in a single day you lost 60k?

That is a 120% DD, not a 19.4 DD that the system should be producing.

I can already smell that at 48 CAR and 19.4 DD that at 4x leverage your number of positions is too low, thus creating a massive opportunity for account ruin. It would even seem that after this 60k loss day you have already achieved ruin.

Therefore did you run a long term backtest, I’m talking 15 years, to at least include the 07/08 debacle with minimum 5 to 10,000 trades? For example, starting at 2005 through to today, and then once complete what did the Monte Carlo plot show you in the last page of the backtest report? Did the lower/red line hit the bottom of the report and stay flat until the end of the test? Did the table at the top for 1% percentile hit 100% DD? And the 5% percentile also hit 100%? I’m guessing at least the first three or four lines of this report will be showing it hit ruin (100%) draw down, which is very bad.

Over a 15 year test, a good 5 to 10,000 trades, not one single line in this sheet of the report should be showing ruin. The red lower line should not be hitting 0 and staying flat. All three lines, upper green, middle black 50% probability and lower red line should all be making it to the top right of the chart. If red hits ruin the easy fix is raising the number of positions. Raise to 50 and try again, still hitting ruin on some? Raise to 60 positions and try again.

Yes, sure, I know it sucks thinking your 48 car may have to now be 25 after this change with more positions as generally on these systems more positions equals less profit, however that is not necessarily a bad thing as DD will also improve and you’ll be more confident to throw more money at the system.

Also the other thing you can do to instantly add more positions and reduce this problem is to split the strategy into two separate systems. Are you trading the R1000 only? Why not use 25k capital on a 40 position R1000 version and 25k capital on a 40 position R2000 version at the same time? You’ll get more signals, more fills, and have instantly halved the risk because you technically have 80 positions now spread over the same 50k capital. Of course I still think it sounds like 40 positions is too little given your example of already achieving ruin and very high CAR figures, so I still think you need to consider more than 40 positions in this type of system.

I don’t think leverage is the enemy or problem here. In fact leverage is what makes these systems work well. It seems to me that you should consider your risk management instead (number of positions) and also ensure you are not trading a system that has a long term chance of 100% ruin.

I am very anal in respecting the Monte Carlo report with ruin. If even the 1% result gets to say 60% I won’t trade the system. Especially if the 5% percentile is above 50% DD then I know I’m being too risky and will increase my position count by 5 or 10 and run my 15 year test again to ensure I’m safe.

If you do as you suggest and reduce leverage but increase capital you are achieving nothing. 50k x 4 = 200k exposure across 40 positions, thus 5k per position being placed. 200k x 1 = 200k exposure across 40 positions, thus 5k per position being placed. So you’ll still potentially lose 60k and to make matters worse you’ll be kicking yourself for using up 200k of your own money when you could have used just 50k,gotten the same result of 60k loss and not had the chance to use the 150k elsewhere in other systems/investments today

I’d start with number of positions as the focus, still with 50k capital and 4x leverage. Do long term backtest that include some horrible periods like 07/08 and at least 5000 trades. If the Monte Carlo page is showing ruin in ANY of the percentiles, that is a warning sign.

Of course still try the method of testing I explained earlier to find out if 50k capital really is workable. You might find the sweet spot is starting at more like 80k, which means you are never going to get consistent results that match backtest over the long term if you try to only use 50k.

June 16, 2020 at 6:28 am #111650TrentRothall

ParticipantI think he’s saying if he upped his balance a 500k account that’s when the -60k day could occur.

June 16, 2020 at 7:01 am #111651ParticipantHow do you set up your Monte Carlos Matthew? What parameters do you use I mean? Simulate using trade risk or equity changes?

-

AuthorPosts

- You must be logged in to reply to this topic.