Home › Forums › Trading System Mentor Course Community › Running Your Trading Business › Leverage and System Allocation

- This topic is empty.

-

AuthorPosts

-

October 3, 2017 at 3:14 am #101694

JulianCohen

ParticipantI am looking at the overall balance of my portfolio and trying to work out the way that I would like to allocate my funds. I am looking to allocate them in a way that best uses the available funds and that allows me to make those funds work hardest without increasing my overall risk to dangerous levels, which I think I may be doing at the moment as I have been quite unmathematical in my approach to this so far.

I have one account with all funds in that account.

I have two MR systems and 5 Trend Following/Momentum systems.

The MR systems have the following Exposure from 2000 to 2017

Mean reversion 27.9% to 0.5% with mean average of 10%

MOC 31% to 8.7% with mean average of 15.3%The trend following systems all range from 68% to 80% exposure

At present I have my funds split the following way:

All trend Following systems: 92% of funds in account

MR system: 58% of account

MOC system: 58% of accountI am using full leverage on the MR (200%) and MOC (400%)

So my thinking is that the MR and MOC systems are both working on leverage and both are running at low exposure rates. Over the last 10 years the exposure rates have been very steady at around 8% for the MR and 12% for the MOC. In fact it is really only 2000-2001 that has the very high exposure rates, it drops off after that considerably. However I think that I have over leveraged myself and should I have a big day for positions I could be in trouble.

To put that into perspective the MOC has 50 days with 100% exposure in the last ten years and the MR has had 11 days with 100% exposure.

My trend following systems allocation has crept up in the last couple of months as I have added a couple of systems recently without increasing my account size. A couple of months ago it stood at 60%

So my questions are:

Should I reduce the trend following allocation back to around 60%? My feeling is yes I should.

Is 60% each for the MR and the MOC too much?

Should the MR be half the MOC because of the difference in leverage? I’m really undecided about this and this really is the main crux of the matter. If we are running systems at full leverage what percentage of overall account should we be allocating, bearing in mind the exposure of each system, and the potential exposure for each system. Of course the potential exposure could be 100% but I think we have to work in the bounds of the backtesting model as risk is always there, it is just how we account for it and manage it that is the main thing.Hopefully this will give us all a good point of discussion

October 3, 2017 at 3:40 am #107773ScottMcNab

ParticipantI have been looking at portfolio balance too but from a slightly different way… I feel that the 400% leverage is risky so want to reduce it as much as possible…my goal is 20% cagr for portfolio

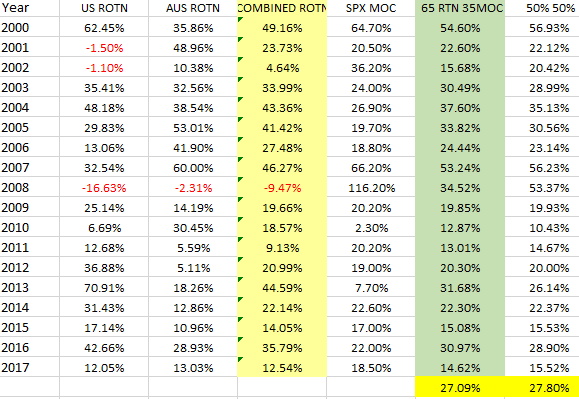

so start with non-leveraged AUS momo and US momo in cash account (can see from table of annual returns not 100% correlated)…once combine AUS and US momo things looking ok (column D)….add MOC (column E)(only SPX in this table but should add in XKO MOC if weren’t being lazy) and looks better (column F and G)..so the balance issue becomes how much can I reduce the highly leveraged MOC and still have it hedge the years when momo go poorly…seems ok 65% momo and 35% moc…(col F)….may even go 75/25

Specifics are not issue…just throwing forward another approach to look at topic

October 3, 2017 at 3:40 am #107781Participant October 3, 2017 at 7:40 am #107774

October 3, 2017 at 7:40 am #107774RobGiles

MemberGood discussion topic thanks Julian. Couple of clarifying questions:

1) What do you mean by

“All trend Following systems: 92% of funds in account

MR system: 58% of account

MOC system: 58% of account”2) When you say ” the MOC has 50 days with 100% exposure in the last ten years and the MR has had 11 days with 100% exposure” do you mean maximum number of positions allowed by the system has been hit that amount of times (which would mean that you would have been exposed 400% exposure on 50 occasions over the past 10 years)?

October 3, 2017 at 9:40 am #107787ParticipantRob Giles wrote:“All trend Following systems: 92% of funds in account

MR system: 58% of account

MOC system: 58% of account”These are the % size I use to position size the account.

If the account was 100,000 then 92,000 is used in all the trend following systems, mostly holding stocks at present, and 58,000 is the total size used to calculate positions for the MOC and 58,000 is used to calculate positions for the MR

Rob Giles wrote:2) When you say ” the MOC has 50 days with 100% exposure in the last ten years and the MR has had 11 days with 100% exposure” do you mean maximum number of positions allowed by the system has been hit that amount of times (which would mean that you would have been exposed 400% exposure on 50 occasions over the past 10 years)?Yes

October 3, 2017 at 10:57 am #107775ParticipantJulian Cohen wrote:So my questions are:Should I reduce the trend following allocation back to around 60%? My feeling is yes I should.

Is 60% each for the MR and the MOC too much?

Should the MR be half the MOC because of the difference in leverage? I’m really undecided about this and this really is the main crux of the matter. If we are running systems at full leverage what percentage of overall account should we be allocating, bearing in mind the exposure of each system, and the potential exposure for each system. Of course the potential exposure could be 100% but I think we have to work in the bounds of the backtesting model as risk is always there, it is just how we account for it and manage it that is the main thing.Hopefully this will give us all a good point of discussion

I am not sure how to objectively make the decision….. if the same equity is shared between several systems then there will naturally be times when the equity is trying to be in multiple places at once…in other words, the backtests are no longer an accurate representation (maybe out by just a little..maybe a lot eg if TF systems miss a few winners at the start of a trend….who knows?)

How do you decide how much to allocate..normal metrics such as maxDD or the timing of maxDD for each system etc would have changed (by an unknown amount)

Is the 60% based on exposure rather than walk forward or correlation of timing of maxDD between systems ?..cant quite work out where the 60 comes from but exposure seems to be common in the post

As a starting point, if (when) another 20% loss like 1987 occurs, at 4x leverage I think I would like my MOC system to be max of 1/3 of portfolio …but 1/4 sounds even better now I write it down…12 months ago it was 100% (but was only 2X leverage back then)….who knows what I will think in another 12 months

October 3, 2017 at 7:09 pm #107776LEONARDZIR

ParticipantJulian,

Are you talking about allocation just to your trading funds or allocation to all your stock and bond assets.

The trading portion of all my stock and bond assets is 13%October 3, 2017 at 8:41 pm #107791ParticipantLen Zir wrote:Julian,

Are you talking about allocation just to your trading funds or allocation to all your stock and bond assets.

The trading portion of all my stock and bond assets is 13%Hi Len

I’m talking about allocation to systems in my trading funds only

October 3, 2017 at 8:44 pm #107794ParticipantThe 60% is entirely made up. It just feels right. That’s my problem really. Nothing too mathematical about my allocation across my trading account, just gut feel. My gut feel says I’m over exposed.

October 3, 2017 at 9:53 pm #107788MemberOK so I’m assuming that you mean there’s 3 separate accounts of $100k for illustrative purposes (I’m basing this on $92k + %58k + $58k doesn’t = $100k)? If so, what’s the reasoning (even if gut feel, not mathematical) you get these allocation %’s? For e.g. let’s say I’m allocating $x’000 to the MOC system. I’m doing this because I want it to be a small % of my overall financial markets investment capital. If I get all signals filled I will be 100% (or 400% because of leverage) exposed for that 1 session. I wouldn’t allocate 58% of my $x’000 to the maximum position size, it would be the full amount. I control the overall risk by the amount I allocate to the strategy. As I write this I get the feeling that we’re not talking about the same thing?

October 3, 2017 at 9:55 pm #107792MemberLen Zir wrote:Julian,

Are you talking about allocation just to your trading funds or allocation to all your stock and bond assets.

The trading portion of all my stock and bond assets is 13%Hi Len, Just out of interest, how are you managing the other 87% of your stock and bond assets if they are not managed under some kind of system?

October 3, 2017 at 11:08 pm #107796ParticipantRob Giles wrote:OK so I’m assuming that you mean there’s 3 separate accounts of $100k for illustrative purposes (I’m basing this on $92k + %58k + $58k doesn’t = $100k)? If so, what’s the reasoning (even if gut feel, not mathematical) you get these allocation %’s? For e.g. let’s say I’m allocating $x’000 to the MOC system. I’m doing this because I want it to be a small % of my overall financial markets investment capital. If I get all signals filled I will be 100% (or 400% because of leverage) exposed for that 1 session. I wouldn’t allocate 58% of my $x’000 to the maximum position size, it would be the full amount. I control the overall risk by the amount I allocate to the strategy. As I write this I get the feeling that we’re not talking about the same thing?Hi Rob I think we are talking about the same thing but in different ways.

I am using 58% for both MR and MOC systems because I am using leverage.

I have 8% of my trading funds sitting unused at the moment in my account. I am leveraging up the 8% to use in the MR and MOC systems.

Now it’s not really 8% because I am effectively leveraging against the whole account as the shares in it count towards my trading size.

Does that make sense? It’s not 92% + 58% +58% not equaling 100%

October 3, 2017 at 11:30 pm #107797ParticipantRob,

The “nontrading” part of my portfolio consists of essentially four positions. Vanguard total stock market index, Vanguard total international stock market index,Vanguard total bond market index and Vanguard total internationbal bond market index. Before I joined the mentoring program I passively allocated 60% stocks and 40% bonds based on my age ,size of portfolio and risk assessment..

Since joining the mentoring program I will use a filter to decide what to do with stock “nontrading ” portions of my portfolio. If the monthly close is <10month MA I will sell otherwise I hold stocks.

Needless to say we have been in a massive 9 year bull market in the US. Therefore not many switches needed since 2009.. Although I only have 13% of assets in my MOC and rotational SPY, and NASDAQ systems the bull market has made my trading assets quite large.October 3, 2017 at 11:53 pm #107795LeeDanello

Participant[instagram][/instagram]

Julian Cohen wrote:My gut feel says I’m over exposed.Maybe you need to lose some weight

October 4, 2017 at 3:39 am #107799MemberLen Zir wrote:Rob,

The “nontrading” part of my portfolio consists of essentially four positions. Vanguard total stock market index, Vanguard total international stock market index,Vanguard total bond market index and Vanguard total internationbal bond market index. Before I joined the mentoring program I passively allocated 60% stocks and 40% bonds based on my age ,size of portfolio and risk assessment..

Since joining the mentoring program I will use a filter to decide what to do with stock “nontrading ” portions of my portfolio. If the monthly close is <10month MA I will sell otherwise I hold stocks.

Needless to say we have been in a massive 9 year bull market in the US. Therefore not many switches needed since 2009.. Although I only have 13% of assets in my MOC and rotational SPY, and NASDAQ systems the bull market has made my trading assets quite large.Hi Len,

Many thanks for providing that context. I’m in a similar situation at present with only 26% of my investable funds allocated to ‘trading’. The balance is essentially buy & hold with stops trailing approx. 15 – 20% below. I am intending to transfer the longer term buy & hold allocation to a mixture of stock and ETF momentum systems, to wrap a bit more discipline / risk management around that part of my capital. Are you thinking of doing the same or does the 10month MA filter do it for you?

-

AuthorPosts

- You must be logged in to reply to this topic.