Home › Forums › Trading System Mentor Course Community › Progress Journal › Trents Weekly Journal

- This topic is empty.

-

AuthorPosts

-

February 1, 2016 at 7:14 am #101416

TrentRothall

ParticipantI finished the theory parts of the course a week or so ago, I feel as though I have gained knowledge that otherwise I definitely wouldn’t have now and maybe not in the future either. I have now moved on to the systems development part of the course

I have been testing different entry techniques to find the winning percentage, after a few days of testing different things I soon disproved one or two of my theories which cannot be a bad thing.

The last few days I’ve been testing using the ROC indicator as part of my entry, which so far is looking alright.

Had a friend’s birthday on the weekend, had a barbecue at their house

February 1, 2016 at 9:08 pm #102628Nick Radge

KeymasterThanks Trent.

Disproving a theory is quite possibly more important because in many instances our theories are a function of our internal biases. As is always stated with running simulations, the computer has no bias!

It’s also a good thing to always try and punch holes in your theory. The harder you look for something that works the more you tend to miss it’s flaws.

February 8, 2016 at 3:37 am #102629Participantearly on in the week I finished coding my momentum system which uses the ROC indicator as part of the entry. The results from this entry technique seemed to be the best that I have been testing so far.

After going through a lot of the charts and checking the code over, and observation that I picked up was that a lot of the daily chop was causing an exit in the position before it had a chance to move upward. I played around with the stoploss using different parameters, also coded up and ATR stop neither of which really helped with the results in fact all they did was increase the drawdown.

I then tested the system on a weekly timeframe to try and alleviate some of the exits caused by the daily chop, trends on a weekly timeframe seem to be smoother.

When first testing on the weekly timeframe I didn’t put enough thought into adjusting the volume and turnover filters and I thought that I had found the ultimate system although I was suspicious. After a quick post to the Forum I soon realised that I didn’t have the filter set right. Once I started testing system properly the results are still showing it is a good start.

Had a Skype call with Nick this morning to go over my backtest settings to make sure that my results were correct.

Next thing is to go over the signals in the Explorer window to ensure that my back tests are picking up the signal ranking properly. Then I’ll stress test the parameters to work out if the system is robust enough.

February 8, 2016 at 7:45 am #102808ParticipantQuote:Next thing is to go over the signals in the Explorer window to ensure that my back tests are picking up the signal ranking properly. Then I’ll stress test the parameters to work out if the system is robust enough.found an error in my backtest ranking code i was using PositionScore = 1000+RankROC; but it was using the ROC on the entry bar and not the setup bar. Changed it to PositionScore = 1000+Ref(RankROC,-1);

it diluted results again but haven’t done a MCS as yet to find out more info… It pays to check!

February 15, 2016 at 12:21 am #102630ParticipantThe last week has been spent basically running MCS and various stress tests on my system. Have been sending the code through to Craig and Nick a few times to ensure everything is on track and no mistakes hidden in there.

I think i need to make some sort of checklist to work through while testing systems, i seem to sway off track and certain tasks take longer than they should…Haven’t been doing much trading of late everything is a bit volatile at the moment.

February 22, 2016 at 7:31 am #102631ParticipantSince last week i have done a bit of a swift U-turn i have gone from a weekly system to a MR system, while the results from my weekly system were not bad Nick pointed out that it might be hard to trade at times with the consistency of returns. This got me thinking about what I actually set out to achieve and originally I was after a short term system with a more consistent profit potential.

I trawled through different Internet forums and blogs around the place to get some ideas, then I added a few things that I had seen and liked out of other mean reversion systems. i ended up with system that at the moment is looking pretty good, I didn’t want something that has a overly high trade frequency because I want to run it on the ASX and didn’t want commissions dragging me back to much.

Started doing some stress tests and Monte Carlo simulations, so I will let you know how I go.

February 29, 2016 at 4:22 am #102632ParticipantAll week has been spent running stress tests and MCS on my Mean Reversion system and i am happy with how things have turned out. It is amazing how adding a few small tweaks and adding you own ideas to a simple concept can turn an ordinary system into something that looks good and SHOULD be easier to trade.

A bonus of the system I think is that it doesn’t need to use an index filter to keep the drawdowns low in fact adding an index filter drastically hurts both the CAR and MDD. Another positive from the test results is that the past few years the system has had good returns, I think it helps me mentally knowing that the system does not rely strong bull market to make decent returns, it also has a fairly high when rate around the 68% mark so hopefully this should help the consistency.

Now that I’m happy with the system and that all the test results seem to be good I will start to paper trade the system in my Sim account. I’ll post a bit more regularly now and let you know how it’s going.

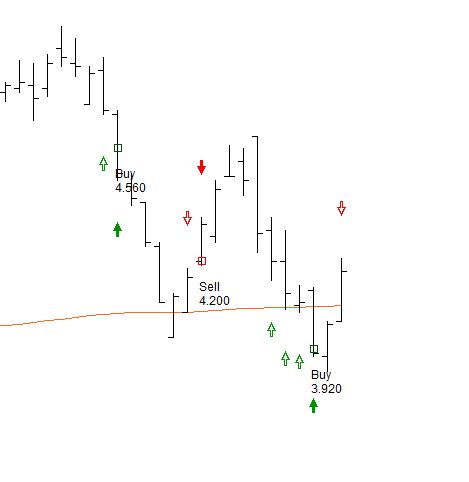

February 29, 2016 at 6:07 am #102633ParticipantHere are a couple of trades in MTR over the last few weeks – one exit tomorrow

March 1, 2016 at 6:21 am #102634Participant

March 1, 2016 at 6:21 am #102634ParticipantTrades for today were 1 exit , no new entries

1 Exit tomorrow – IPH had a nice bounce today to trigger an exit

2 open positions

3 Pending orders for tomorrowNot the ideal setup at the moment – currently waiting for IB to approve my margin account, so trading the system in my sim IB cash account. It doesn’t have API capability so if i get my full portfolio i will have to manually close trades. But it should still allow me to make sure the trades are executing properly and the explorer is not losing trades.

March 1, 2016 at 9:19 am #102875ScottMcNab

ParticipantHi Trent…any websites/forums that you would recommend regarding MR systems ?

Thanks

ScottMarch 1, 2016 at 10:07 am #102635ParticipantHi Scott

i just literally googled short term strategies and read a few of the articles and pages in the Articles depository thread in this forum – thats where i got my my main idea. Also read up some systems by Larry Conners i think some of them are not very robust and are questionable but still have good ideas in them.

March 2, 2016 at 6:00 am #102636ParticipantToday –

1 entry

1 exit in IPH3 open positions

1 pending order for tomorrowWith the ASX having a good day, not many signals

Working on coding up some other systems also just to see how they preform.

March 2, 2016 at 10:48 am #102895ParticipantThanks Trent…thats been my approach to date too.

Cheers

ScottMarch 3, 2016 at 5:59 am #102637Participant3.3.16

No entries

No exits2 pending exits

No pending entriesWill be 1 open position

Everything seems to be operating correctly so far – early days

March 4, 2016 at 7:39 am #102638ParticipantFriday 4.3.16

2 exits

0 entries1 exit signal

3 pending entriesSystem Weekly wrap –

4 Closed trades

3 Winners

1 Loss1 Open position

Entering my trades in the Chartist Trade Tracker Software, will be good to have all the stats there in a organised simple system. Once i have a decent size set of trades the charts will be a good visual reference too.

-

AuthorPosts

- You must be logged in to reply to this topic.